Four Reasons Why the Bond Market Is Not Headed Toward a Liquidity Crisis

Liquidity in fixed income markets has become a major focus of concern inside and outside of the investing community. While the consensus view suggests that US bond markets have become more susceptible to serious shocks, Invesco Fixed Income believes there are four main factors that will help the US avoid a liquidity-induced systemic crisis.

Liquidity concerns are growing

Investors, asset managers, bank regulators and policymakers are worried that changes in the bond markets, post-financial crisis, have led to greatly reduced levels of bond market liquidity — meaning it may now be more difficult to transact smoothly in bond markets without price disruptions.

Concerns are growing that we may be entering a “perfect storm” where fears of rising interest rates cause bond investors to simultaneously rush for the exits just when US brokerage firms, constrained by new regulations, are less able to act as potential buyers. The consensus view suggests that because US bond markets have grown dramatically and no longer enjoy the support of broker/dealers, they are much more susceptible to shocks. Herd behavior, it is feared, could lead to bond market turmoil with negative repercussions beyond financial markets to the real economy.

Gauging the problem

Aggressive monetary easing has fueled the enormous growth in demand for risk assets — especially among retail investors — as investors have sought yield. On the supply side, companies have issued record amounts of debt to take advantage of attractive financing.

The growth in the sheer volume of US holdings of fixed income assets and the decline in bond market intermediation may indeed lead to conditions where investment losses are exacerbated in a bond market sell-off. However, we believe it is important to distinguish between the potential for investment losses due to shifts in supply and demand and a systemic breakdown. While volatility may rise as markets anticipate a tighter Fed (or other global developments), we believe several mitigating factors suggest that a systemic crisis caused by a lack of bond market liquidity is not in the making.

Dire predictions appear unwarranted

Reduced bond market liquidity means that sudden outflows from bond mutual funds are a growing source of risk. However, we believe four factors challenge the more dire predictions of a systemic crisis:

1. Fixed income growth in line with equities: Both US fixed income and equity mutual fund holdings have grown, leaving their relative composition largely unchanged. Bond exchange-traded funds (ETFs), which can be traded more frequently and are therefore viewed as potentially more destabilizing, have also grown, but remain a small fraction of total US bond fund holdings.

2. Broker/dealer support overestimated: It is a misconception that US broker/dealers have been a source of support in times of market stress. Rather, broker/dealers have often themselves been sellers. History shows that, even when broker/dealers’ capacity to take on risk was elevated, they were heavy sellers of inventory during market downturns, as shown in the graph below. That said, because leverage among key US financial players, such as broker/dealers and hedge funds, is widely acknowledged to be sharply lower than pre-financial crisis, we believe there is less risk of “forced” selling today, which bodes well for improved bond market functioning in times of stress.

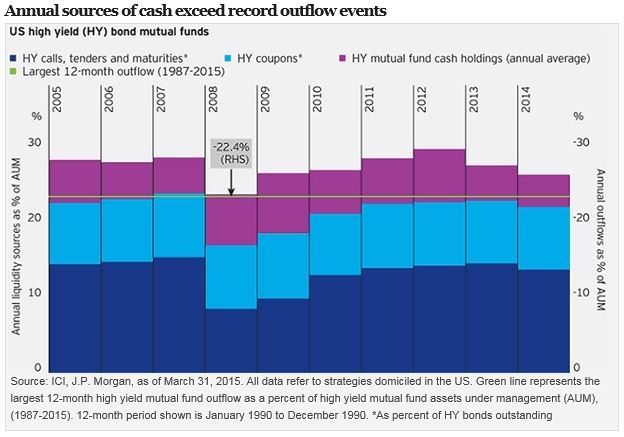

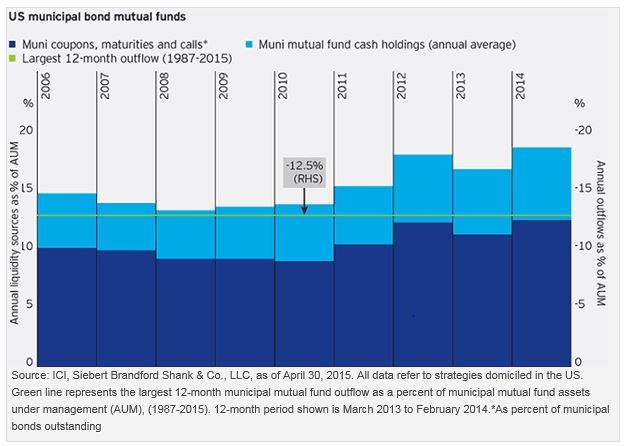

3. Fixed income generates cash flows: Bond mutual funds generate liquidity naturally from maturities, coupons, calls and tenders — without trading. Combined with portfolio cash holdings, this level of “intrinsic liquidity” in US mutual funds has historically been sufficient to cover the worst redemptions, as seen in the charts below.

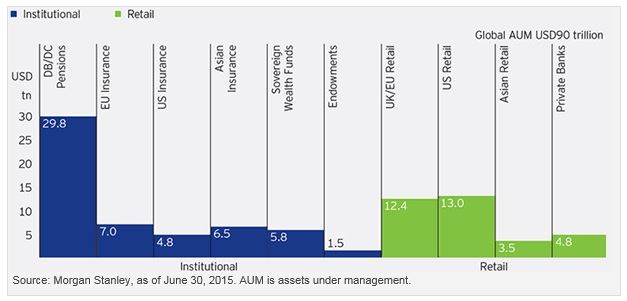

4. Structural support: The global fixed income asset class benefits from the structural support of long-term investors. Institutional holders dominate the fixed income investor base, led by pension funds, which tend to favor longer-duration assets. On the retail side, investors are likely to continue to seek income, capital preservation and lower volatility, which points to continued demand for fixed income products. For these reasons, we believe the global bond investor base tends to have strong hands, which would likely be further strengthened in a higher yield environment. In any case, a sell-off in bonds would drive yields higher, likely attracting additional buyers seeking yield.

Implications for bond investors

As the Fed transitions toward “normal” monetary policy, we certainly do expect to see greater bond market volatility. We believe such volatility argues for active management and presents opportunities for prepared asset managers with careful processes in place to manage portfolio liquidity and take advantage of market fluctuations.

The way forward: policy prescriptions

In general, there appears to be little consensus about how to resolve issues around liquidity at the market level. Regulators face a number of competing goals: limiting the interdependence of banks, ensuring adequate levels of liquidity among asset managers and preserving the flexibility of issuers to issue debt opportunistically. The current focus appears to be centered on asset managers, as the US Securities and Exchange Commission is currently exploring several new liquidity risk management rules for some mutual funds and ETFs.

We believe two additional solutions could be constructive:

- Creation of electronic and open trading venues, allowing direct client-to-client transactions versus client-to-dealer only.

- Standardization of bond issuance to reduce fragmentation in the bond market by creating fewer unique securities.

Such approaches would require significant changes in the way investors and issuers currently think about and operate in bond markets. Moreover, these changes would not necessarily resolve the fundamental issue of preventing market shocks. However, in our view, they could significantly improve prevailing liquidity conditions in stable markets.

Read more about our views on bond market liquidity.

Read Tony Wong’s What is the credit cycle telling us about 2016?

Important information

Liquidity refers to how quickly and cheaply an asset can be converted into cash.

Monetary easing refers to action(s) by a central bank to reduce interest rates and boost money supply as a means to stimulate economic activity.

Yield is the income return on an investment.

Volatility measures the standard deviation from a mean of historical prices of a security or portfolio over time.

Intrinsic value represents the inherent business value of portfolio holdings during a two- to three-year investment horizon, based on their estimates of future cash flow.

All fixed income securities are subject to two types of risk: credit risk and interest rate risk. Credit risk refers to the possibility that the issuer of a security will be unable to make interest payments and/or repay the principal on its debt. Interest rate risk refers to fluctuations in the value of a fixed income security resulting from changes in the general level of interest rates. Non-investment grade securities (junk bonds) have greater risk than investment grade securities, including the possibility of default. Economic and regulatory factors may affect a municipal security’s value, interest payments and repayment of principal.

The information provided is for educational purposes only and does not constitute a recommendation of the suitability of any investment strategy for a particular investor. Invesco does not provide tax advice. The tax information contained herein is general and is not exhaustive by nature. Federal and state tax laws are complex and constantly changing. Investors should always consult their own legal or tax professional for information concerning their individual situation. The opinions expressed are those of the authors, are based on current market conditions and are subject to change without notice. These opinions may differ from those of other Invesco investment professionals.

All data provided by Invesco unless otherwise noted.

Invesco Distributors, Inc. is the US distributor for Invesco Ltd.’s retail products and collective trust funds. Invesco Advisers, Inc. and other affiliated investment advisers mentioned provide investment advisory services and do not sell securities. Invesco Unit Investment Trusts are distributed by the sponsor, Invesco Capital Markets, Inc., and broker-dealers including Invesco Distributors, Inc. PowerShares® is a registered trademark of Invesco PowerShares Capital Management LLC (Invesco PowerShares). Each entity is an indirect, wholly owned subsidiary of Invesco Ltd.

©2016 Invesco Ltd. All rights reserved.

Four reasons why the bond market is not headed toward a liquidity crisis by Invesco Blog