Global Investment Insights: Longer lifespans paired with drop in birth rates create drag on global productivity growth — emerging markets buck trend

By Bruce Campbell of Pyrford International Ltd.

We are always surprised that so little attention is paid to the rapidly changing demographic situation throughout the world. It gets lip service by politicians but then they swiftly move on to issues they believe to be more important or, (more likely), bigger vote-winners.

The facts are simple — the birth rate is dropping everywhere, work-force growth is dramatically slowing (to negative in many countries), the median age is rising and people are living longer. The repercussions are immense. Pension and social security systems are inadequate, health care and retirement facilities ditto and government budgetary forecasts are not worth the paper they are written on due to slowing GDP growth.

Economic growth is made up of the expansion in output per employed person (productivity) and the rate of growth of employed people. If the latter is steadily in decline then the potential rate of economic growth declines. And that is the pickle in which the world finds itself.

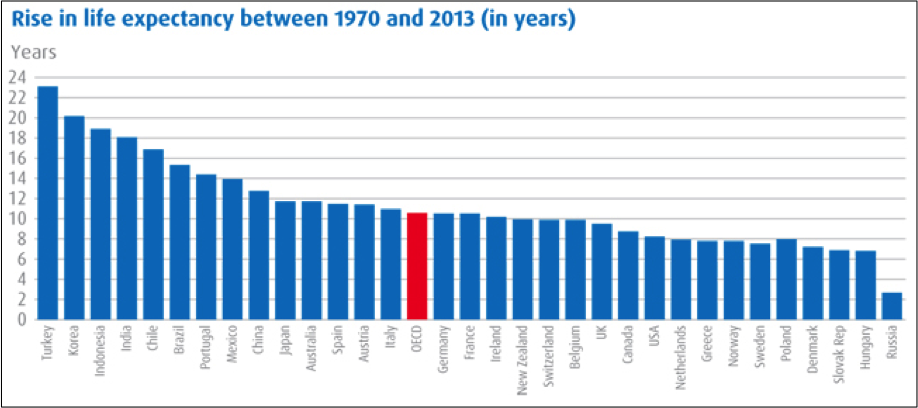

Pictures are better than words. Take a look at what has happened to average life expectancy in the relatively short period from 1970 to 2013.

It is remarkable that in many advanced economies, where life expectancy was already relatively high, it has increased by around 10 years over the period illustrated. In developing economies the increase tends to be higher. Whilst we should applaud the improvements in health care, diet and lifestyle that have permitted this trend to longevity we need to recognise that back in the 1970s this was not anticipated and not embraced in forward planning. Governments and others have been playing a game of catch-up ever since.

In 1950 the world’s average life expectancy was 46.8. Today, it is 70.5. The world’s median age was 23.5 in 1950, 22.5 in 1980 and 29.6 in 2015. In the advanced countries the median age has risen from 28.5 in 1950, to 31.9 in 1980 and 41.2 in 2015. Almost inevitably, Japan tops the median age list at 46.5, hotly followed by Germany at 46.2 and Italy at 45.9 (UN data).

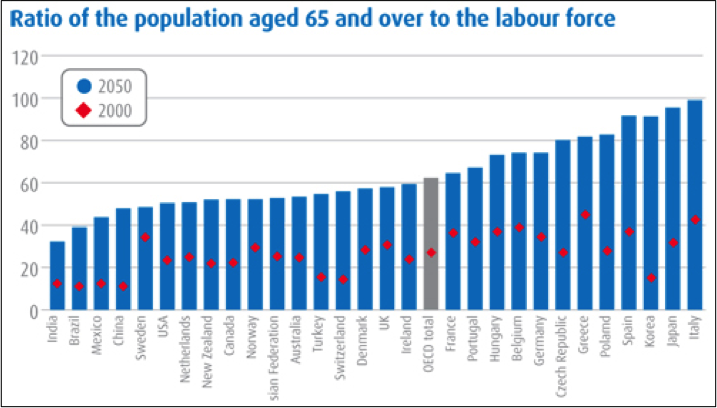

The aging profile is dramatically illustrated in the following chart:

The countries at the far right of the chart have a real problem — the “oldies” (over 65) will be almost as numerous as the workers by 2050. The red dot shows the situation in 2000 and highlights the rapid deterioration in all countries over the period.

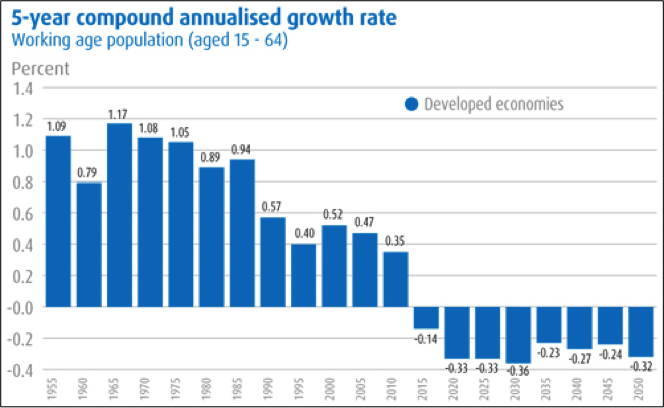

And the working-age population? This is defined by the UN as all people aged between 16 and 64. In the developed world this segment of the population, on average, is now starting to shrink. This will deduct around 0.3% annualised from GDP growth over the next 35 years. In the previous 35 years it added an average of 0.4% annualised to developed world GDP growth. The combination of the two means a comparative (negative) growth differential of 0.7% annualised in the next several decades.

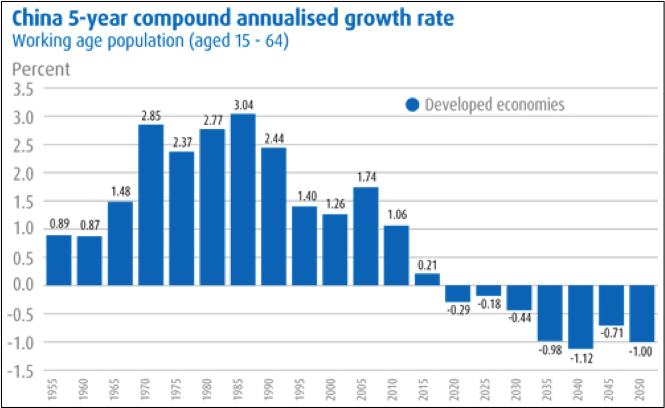

The boom country of the past twenty years, China, is about to experience a very dramatic change in fortunes due to its one-child per family policy — a policy that the government is only now getting around to amending — but it is very much a case of too little too late. Even if all the fetters are removed there is no indication that there will be a birth-boom in China. The potential working-age population starts to shrink about now providing a stark contrast to the growth of the past 50 years. A glance at the chart is sufficient to indicate that the comparative negative growth differential is going to be considerably more than 1% annualised.

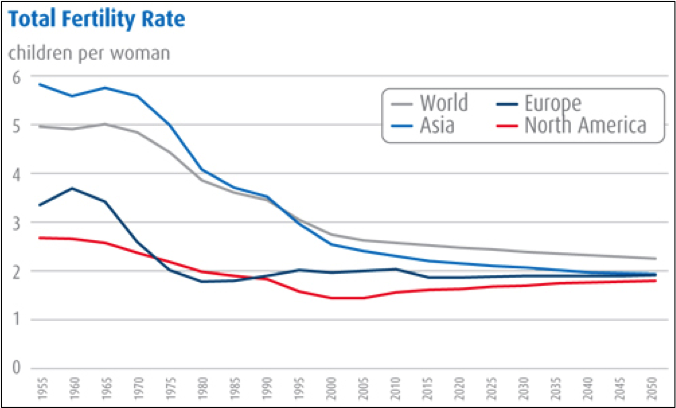

The fertility rate (children per woman) needs to be 2.1 for a population to maintain itself. Anything lower and shrinkage occurs. In all of the world’s regions the fall in the fertility rate has been nothing short of dramatic. Europe is in the most parlous position with the fertility rate now comfortably below replacement level.

So the picture that emerges is very clear — a rapidly ageing global population with steadily fewer workers (relative to the retirees) to maintain overall living standards. From an investment perspective behavioural economics now becomes a very important study. A legion of retirees behaves quite differently than an equivalent legion of younger workers. Retirees need income and security, spend a significant amount on healthcare, tend to be downsizing housing rather than upsizing, will not be seeking mortgages, are unlikely to be patronizing shops selling the latest fashions and will be liable to spend some of the kid’s inheritance on the odd cruise (the fastest growing holiday segment).

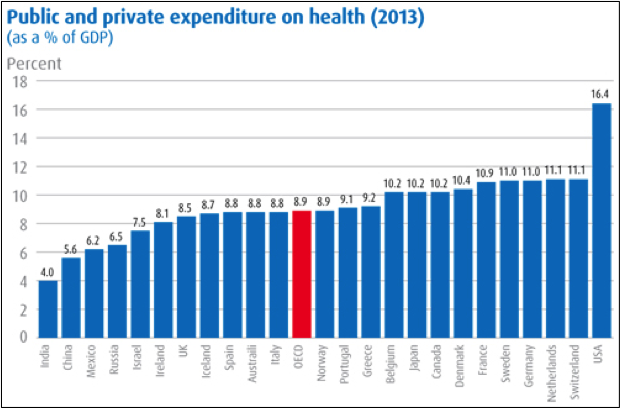

Healthcare is already a sizeable slab of the budget of most countries but it is about to get much bigger. No country rivals the “spend” of the U.S. (relative to GDP) but all will be rising up the scale over the next few decades. If more of the pie is spent on healthcare something else misses out. This is a substantial challenge for governments throughout the world — again, one that tends to be under-appreciated.

The impression may be gained from the preceding that there is no or at best little light at the end of the tunnel. Not so, as some countries are still experiencing booming population growth. We refer to countries such as India, Nigeria, Ethiopia, Pakistan, Tanzania and the Democratic Republic of the Congo which, between them, will total almost 3 billion people in 2050 according to the UN. The lion’s share of this is India which will expand from a current 1.3 billion to 1.7 billion, making it easily the most populous country in the world by 2050. China’s population is expected to fall by around 30 million over the same period but by a total of 370 million by the end of the century.

India’s working-age population will grow by 1.1% annualised over the next 20 years and an average of 0.8% annualised over the 35 years to 2050. The task is to make effective use of this growth-dividend.

The same comment applies to Africa, the continent where the bulk of the remaining growth occurs. We try not to be sceptics but we are only too aware that India and Africa have so often disappointed in the past. But the fact is that the world will need the people of working-age to be productively employed because elsewhere there will be a vast number of retirees sitting back hoping that someone is out there generating the wealth to fund their pension or social security benefit. Or perhaps it will be robots. Now there’s a topic for a future Global Investment Insights!

All investments involve risk, including the possible loss of principal.

Foreign investing involves special risks due to factors such as increased volatility, currency fluctuation and political uncertainties. High yield bond funds may have higher yields and are subject to greater credit, market and interest rate risk than higher-rated fixed-income securities. Keep in mind that as interest rates rise, prices for bonds with fixed interest rates may fall. This may have an adverse effect on a Fund’s portfolio.

Investments cannot be made in an index.

This presentation may contain targeted returns and forward-looking statements. “Forward-looking statements,” can be identified by the use of forward-looking terminology such as “may,” “should,” “expect,” “anticipate,” “outlook,” “project,” “estimate,” “intend,” “continue” or “believe” or the negatives thereof, or variations thereon, or other comparable terminology. Investors are cautioned not to place undue reliance on such returns and statements, as actual returns and results could differ materially due to various risks and uncertainties. This material does not constitute investment advice. It does not have regard to the specific investment objectives, financial situation and the particular needs of any specific person who may receive this report. Investors should seek advice regarding the appropriateness of investing in any securities or investment strategies discussed or recommended in this report and should understand that statements regarding future prospects may not be realized. Investment involves risk. Market conditions and trends will fluctuate. The value of an investment as well as income associated with investments may rise or fall. Accordingly, investors may receive back less than originally invested.

Pyrford International Ltd. (Pyrford) is a registered investment adviser and a wholly owned subsidiary of BMO Financial Corp. BMO Global Asset Management is the brand name for various affiliated entities of BMO Financial Group that provide investment management and trust and custody services. Certain of the products and services offered under the brand name BMO Global Asset Management are designed specifically for various categories of investors in a number of different countries and regions and may not be available to all investors. Products and services are only offered to such investors in those countries and regions in accordance with applicable laws and regulations. BMO Financial Group is a service mark of Bank of Montreal (BMO).

BMO Asset Management Corp. is the investment adviser to the BMO Funds. BMO Investment Distributors, LLC is the distributor. Member FINRA/SIPC.

BMO Asset Management Corp., BMO Investment Distributors, LLC, BMO Private Bank, BMO Harris Bank N.A. and BMO Harris Financial Advisors, Inc. are affiliated companies. BMO Private Bank is a brand name used in the United States by BMO Harris Bank N.A. BMO Harris Financial Advisors, Inc. is a member FINRA/SIPC, an SEC registered investment adviser and offers advisory services and insurance products. Not all products and services are available in every state and/or location.

Investment products are: NOT FDIC INSURED — NOT BANK GUARANTEED — MAY LOSE VALUE.

© 2016 BMO Financial Corp. (4110060)