Executive Summary

In the context of the role that debts and deficits play in overall economic policy, in this paper I focus on the philosophy known as “sound finance,” which includes adherents who believe that governments should seek to balance their budgets. I, however, take a different view, and believe that the role of government when dealing with budget deficits should be one of “functional finance,” which ensures that the policies implemented help to reach the overarching goals of macroeconomic policy (generally held to be full employment and price stability).

This paper attempts to show why the proponents of sound finance are mistaken by defining and unpacking a series of “myths” that are foundational to, or at least helpful to, convincing us that sound finance requires that governments run a balanced budget. Though not a complete list, following are the “myths” presented:

Myth 1: Governments are like households

Myth 2: Printing money to finance budget deficits is inflationary

Myth 3: Budget deficits/high debt lead to high interest rates

Myth 4: Budget deficits are unsustainable

Myth 5: Debt is a burden on future generations

To conclude, I offer some thoughts on the actual impact of monetary policy on the real economy, which I believe to be quite small. These thoughts include a brief discussion about how fiscal policy, once the nature of government debts and deficits is fully understood, can be a viable alternative to monetary policy.

Introduction

What do the following people all have in common: Warren Buffet, Seth Klarman, Bob Rodriguez, Rob Arnott (at this point you may be looking at the list and thinking, hmm, all value investors), Paul Singer, Angela Merkel, George Osborne, and Barack Obama?

The answer is that they all seem to believe in an economic philosophy known as “sound finance,” as witnessed by the quotations below. As Walker (1939) noted, “Sound finance is sometimes worshipped as an end in itself…sound finance means the observance of certain arrangements which have become sanctified by habit and tradition…its intrinsic value [is] taken as self-evident.” Effectively this group of people (some of whom are actually my friends) believe that governments should seek to balance their budgets.

In the last fiscal year, we were far away from this fiscal balance… All of America is waiting for Congress to offer a realistic and concrete plan for getting back to this fiscally sound path. Nothing less is acceptable. — Warren Buffet, 2012

We are talking about the underlying structural issues of the federal budget deficit…the longterm insolvency of the country due to the government having made (and continuing to make) massively unpayable promises for the future. — Paul Singer, 2013

Governments that run huge deficits, promise entitlements that will be next to impossible to deliver, and depend on the beneficence of foreigners to stay afloat inevitably must collapse. — Seth Klarman, 2010

I don’t see how financial markets do well longer term if you continue to erode the fiscal integrity of our financial system. — Bob Rodriguez, 2012

Our debt level will have to be brought down to a more reasonable level. — Rob Arnott

A Swabian Housewife [would say] you cannot live permanently beyond your means. — Angela Merkel, 2008

Without sound public finance, there is no economic security for working people… in normal times, governments…should run a budget surplus to bear down on debt. — George Osborne, 2015

Small businesses and families are tightening their belts. Their government should too. — Barack Obama, 2010

In contrast to this group I adhere to a school that takes a very different view of the role of government budget deficits. It is best summed up by the following quotation from a member of my coterie of long dead favourite economists, Abba Lerner.

The central idea is that government fiscal policy, its spending and taxing, its borrowing and repayment of loans, its issue of new money and its withdrawal of money, shall be undertaken with an eye only to the results of these actions on the economy and not to any established traditional doctrine about what is sound or unsound. This principle of judging only by effects has been applied in many other fields of human activity, where it is known as the method of science… The principle of judging fiscal measures by the way they work or function in the economy we may call Functional Finance. (1943)

In essence, Lerner is saying that government deficits should be judged only by the degree to which they help us reach the goals of macroeconomic policy (generally held to be full employment and price stability), rather than by some arbitrary measure such as not having deficits of more than X% of GDP. The latter is “sound finance;” the former is “functional finance.”

Of course, finding myself facing the luminaries listed at the outset leaves me feeling a little like Captain Redbeard Rum in Blackadder II,

Edmund: Look, there’s no need to panic. Someone in the crew will know how to steer this thing.

Rum: The crew, milord?

Edmund: Yes, the crew.

Rum: What crew?

Edmund: I was under the impression that it was common maritime practice for a ship to have a crew.

Rum: Opinion is divided on the subject.

Edmund: Oh, really?

Rum: Yahs. All the other captains say it is; I say it isn’t.

Edmund: Oh, God; mad as a brush.

So let me try to explain why I take a very different view of the role of debts and deficits, and hopefully convince you that I am not as “mad as a brush.” To do this I’m going to attempt to show why the proponents of “sound finance” are mistaken by laying out a series of “myths” (or, for the alliteratively minded, five fiscal fallacies).

Myth 1: Governments are like households

Perhaps the foundational myth of all believers in sound finance is that the government sector is just like a household. The intuition for this belief and its accompanying misunderstanding can be seen by examining the stalwart go-to of economists – a simple barter system.1

Let’s imagine that I own an awful lot of cows, and you are a particularly skilled maker of yurts.2 In return for some of my surplus milk and cheese, you agree to repair my yurt periodically and, should the need arise, build me a new one. All is fine with the world until I happen to attend a local village meeting where I uncover that you have made exactly the same deal with just about everyone else in the village (the butcher, the baker, and candlestick maker included). It occurs to us that even if you worked all of the hours available there is simply no way that you can ever hope to repair/build enough yurts for all of us. You have incurred an excess of private debt. This is clearly bad.

This simple parable tells us that the over-accumulation of private sector debt is a problem. I completely agree with this analysis. However, those in the sound finance camp then extrapolate this finding into realms that involve governments and their deficits. Sadly, they do so in an indiscriminate fashion, and therein lies the problem.

We need to distinguish between governments that are what we might describe as monetarily sovereign (by which we mean those that issue their own currencies, have floating exchange rates, and issue debt in their own currency) and those that lack such sovereign status. In the former category we find countries such as the United States, the United Kingdom, and Japan whilst the Eurozone is a prime example of the latter group. This distinction has a great bearing on how one should think about debt and deficits.

Those nations that enjoy monetary sovereign status can, in effect, borrow from themselves. They have the ability to create money and spend it – essentially ex nihilo. Thus they can’t ever be forced into insolvency. If this sounds a little like Rumpelstiltskin spinning straw into gold that is because it is. Such are the benefits that are potentially available to monetarily sovereign nations.

However, for both types of regimes public debt is still different from private debt. In fact, public debt is often the counterpart of private saving. To see this we need to do a little macroeconomic accounting. (Double jeopardy on the boredom stakes, I know, but try and stay with me here.)

Let’s start by stating that output can be thought of as consumption, plus investment, plus government spending, plus exports minus imports. This is known as the expenditure model of GDP.

Y = C + I + G + (X – M)

We could also take a different perspective (the income model of GDP) and say that all output is consumed, saved, or paid in taxes.

Y = C + S +T

Setting these two equations equal to each other gives:

C + S + T = C + I + G + (X – M)

Cancelling out terms and rearranging generates what is known as the sectoral balances:

(S – I) = (G – T) + (X – M)

This states that if the private sector wishes to save in excess of its investment, then there must be a government deficit and/or a current account surplus. If one were working with a closed economy (i.e., no foreign trade) then the government deficit would be the exact counterpart to any private sector savings surplus.

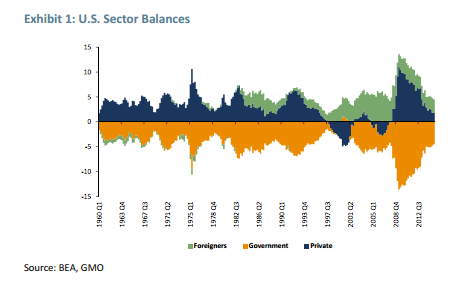

Now, one of the very many pleasing aspects about accounting identities is that they have to be true (by construction) and thus, unsurprisingly, when we look at the data we see exactly what we would expect. The private sector generally runs surpluses with the counterpart coming from the government’s fiscal deficits.

We can see that twice in the sample shown in Exhibit 1, wherein the private sector has run significant deficits with neither experience ending well. The first was the TMT bubble, when firms drove the private sector into deficit, and the second was the housing bubble with households driving the private sector into deficit. Both are examples of the dangers of debt accumulation by the private sector. However, the government sector has been accumulating debt over this whole period seemingly with impunity – contrary to the proclamations of the sound finance adherents.

Once one understands that the government deficits are the counterpart to private sector savings, then concepts such as the national debt take on a different hue. There used to be a clock that was located near Times Square that kept a real count of the U.S. national debt. I gather it stopped working when the $10 trillon mark was surpassed. The current U.S. national debt stands at $18.8 trillion (as of the time of writing in December 2015). This sounds mind-bogglingly large – can anyone imagine repaying $18.8 trillion? Of course, it won’t be repaid. In fact, given the counterpart nature of the government deficit, the national debt could (and perhaps should) easily be relabled as national saving. Suddenly that $18.8 trillion figure doesn’t seem anywhere near so scary!

Myth 2: Printing money to finance budget deficits is inflationary

Perhaps one of the most persistent myths surrounding budget deficits is the idea that they are inherently inflationary. This is usually expressed in terms of “printing money to finance budget deficits causes inflation.” This statement is related to another myth that I have explored before concerning hyperinflations.3 The root of this myth seems to stem from the quantity theory of money.

The quantity theory of money simply states that all of the money in the economy multiplied by the number of times it goes around must be equal to the prices paid times the volume of goods and services purchased (MV = PY). In other words it says that expenditure equals income, which is nothing more than an identity.

In order to turn this into a theory of inflation one has to make some rather unrealistic assumptions such as velocity being fixed and output being fixed. If one is willing to make such assumptions, then by construction the only two free variables are money and prices, ergo changes in money must cause changes in prices, according to the adherents of this view. The equation they believe defines the role of money in creating inflation is thus:

![]() Strangely enough, we know that PY can also be written as the sum of its parts: PY = C + I + G + (X – M). When written this way we see that there is nothing unique about G (government spending). Any of the compoments of GDP could potentially cause inflation, if it raises output above the full employment level. Let us be clear here. Yes, it is certainly possible that running government deficits can create inflation (if doing so pushes the economy beyond its limits), but so could any other element of GDP (e.g., consumption or investment). There is nothing unique about government deficits from an inflationary point of view.

Strangely enough, we know that PY can also be written as the sum of its parts: PY = C + I + G + (X – M). When written this way we see that there is nothing unique about G (government spending). Any of the compoments of GDP could potentially cause inflation, if it raises output above the full employment level. Let us be clear here. Yes, it is certainly possible that running government deficits can create inflation (if doing so pushes the economy beyond its limits), but so could any other element of GDP (e.g., consumption or investment). There is nothing unique about government deficits from an inflationary point of view.

Indeed, taking a functional approach to government deficits clearly recognises the possibility that a deficit could be inflationary. When asking whether a particular deficit/surplus position helps us achieve our macroeconomic objectives (full employment and price stability) we are explicitly thinking about the consequences of our actions.

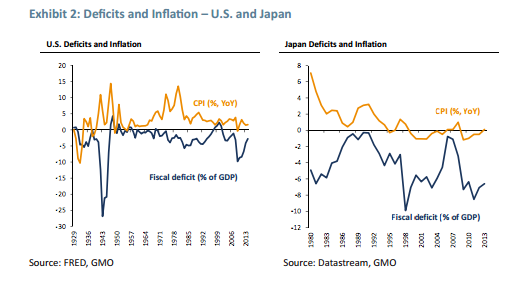

Ultimately, all economic theories should be checked against the data. So let’s cast a cursory eye over the empirical evidence by way of the U.S. and Japan. In neither case is there any evidence of a strong link between fiscal deficits and inflation. The only evidence of any linkage that I could find in the U.S. data was around the time of World War II, when the U.S. was running major deficits due to the war, and then seeing inflation as a result of the shutdown in trade and eventually the return to a peacetime economy with the unleashing of pent-up demand. Obviously this tells us more about the impact of war (and it is well known that wars have often been associated with inflation) rather than anything meaningful about the relationship between deficits and inflation.

We will return to the issue of “financing” the deficit in the course of our discussion of the next myth.

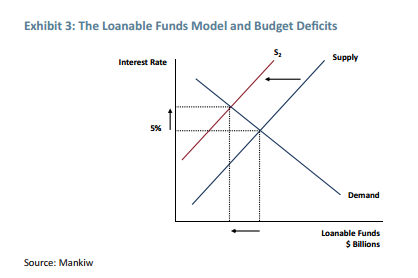

Myth 3: Budget deficits/high debt lead to high interest rates According to mainstream economic textbooks, budget deficits should lead to higher interest rates. The model used to back such claims is known as the loanable funds theory.4 According to this model, the natural rate of interest is determined by the interaction of the demand and supply for funds as per the diagram presented in Exhibit 3.

According to the textbooks, national saving is the source of loanable funds, and is comprised of the sum of private and public saving. An increasing budget deficit reduces public saving and thus overall savings, pushing the supply of loanable funds to the left (to the curve S2). According to this view of the world, the budget deficit doesn’t influence the demand for funds, leaving the demand curve unchanged. Thus the result is rising interest rates.

As we have detailed in the aforementioned papers, we don’t find the loanable funds model to be a useful way of thinking about the world. It is riddled with flaws that render it unusable. We won’t go over all of the issues again here, but suffice it to say, the biggest issue is that the model assumes that savings must precede investment. This is a reasonable assumption if you are living in a onecommodity, corn-based economy. If you want to invest in more corn, you must save some corn first. However, when we move to monetary-based economies this ordering is no longer true. Investment can (and does) precede savings in such a system. When you want to invest, you go to the bank and ask for a loan. The bank decides whether or not to grant such a loan, but it isn’t constrained by deposits or reserves. It will make the loan, and then worry about how to ensure regulatory compliance with reserve requirements, etc., afterward.

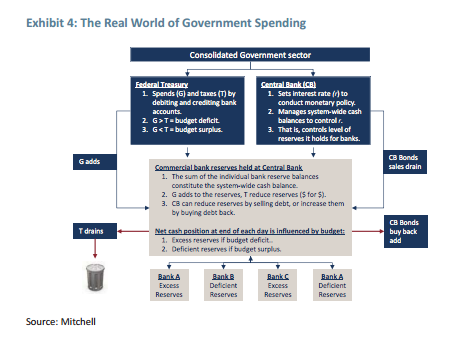

So, what would a realist (as opposed to an economist) say about interest rates and budget deficits? The diagram in Exhibit 4 is taken from Bill Mitchell – one of the few living economists whom I respect deeply.

The real world model is certainly a lot messier than the loanable funds model and, interestingly, it comes to a very different conclusion about the impact of deficits on interest rates. Let’s start by acknowledging that when a government spends it simply tells the central bank to credit the government’s account with funds (created by keystrokes).5 Similarly, when a government taxes, these funds eventually end up as a credit to the government in their account at the central bank.

The real world model is certainly a lot messier than the loanable funds model and, interestingly, it comes to a very different conclusion about the impact of deficits on interest rates. Let’s start by acknowledging that when a government spends it simply tells the central bank to credit the government’s account with funds (created by keystrokes).5 Similarly, when a government taxes, these funds eventually end up as a credit to the government in their account at the central bank.

So, when a government runs a fiscal deficit, it creates more money than it receives (by definition). This money is then used to purchase goods and services, so the central bank transfers money from the government’s account to the reserve account of the bank with whom the sellers of goods and services happen to hold their accounts. This creates excess reserves at the bank. No bank willingly sits on excess reserves, and so money is lent out in the interbank market. This has the effect of lowering the interest rates towards zero (or to the level that the central bank pays on reserves). So the prediction from the real world model is that interest rates get driven down by budget deficits, not up as per the loanable funds framework.

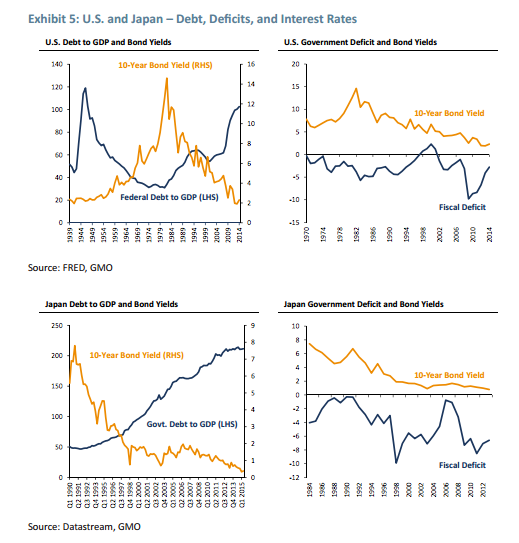

We can thus take the predictions to the data and see which is better supported. Exhibit 5 shows the charts for both the U.S. and Japan with respect to both the deficit and interest rates and the debt to GDP ratio and interest rates.

The evidence seems to come in strongly on the side of the real world model. Budget deficits and high debt levels don’t seem to be associated with higher interest rates at all. This probably shouldn’t be a surprise, given that weak economic growth is likely to cause both high deficits and low interest rates – entirely consistent with the real world model.

The evidence seems to come in strongly on the side of the real world model. Budget deficits and high debt levels don’t seem to be associated with higher interest rates at all. This probably shouldn’t be a surprise, given that weak economic growth is likely to cause both high deficits and low interest rates – entirely consistent with the real world model.

In the interest of full disclosure, I should point out that somewhere around the time that the bond yield and the debt to GDP ratio crossed in the chart for Japan, a much younger and even more foolish version of me uttered the phrase “Japanese bond yields can’t possibly go any lower.” Over the intervening 20 years, I have watched bond yields in Japan halve, halve, and halve again! It was at least in part due to that experience that I have spent much time thinking about debts and deficits, trying to learn from my mistakes.

Myth 4: Budget deficits are unsustainable

Sound finance adherents often speak of the “unsustainable” nature of budget deficits. But what do they mean by the term “unsustainable?” Bernanke6 provides us with a fairly standard answer: “a sustainable path that ensures that debt relative to national income is at least stable.” For now let’s accept Bernanke’s definition at face value (I’ll come back to critique it shortly).

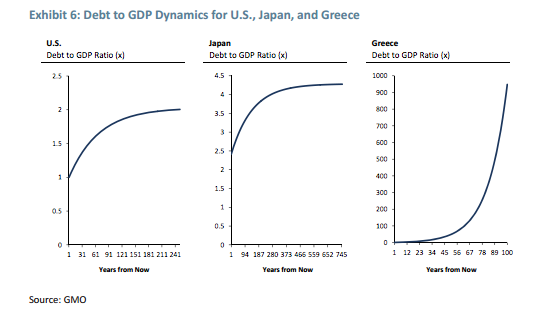

One can model the dynamics of debt7 to GDP over time and see if today’s values for the relevant variables lead to a stable path or not. In essence it comes down to whether the real interest rate (r) is higher or lower than the real growth rate (g). If r > g then any positon of primary deficit will be “unsustainable.” Plugging in today’s values for the U.S. and Japan reveals both have positions that are sustainable as per Exhibit 6. To give a flavour of what “unsustainable” looks like, I have included the picture for Greece circa 2009.

The biggest problem with this kind of analysis is that it assumes that nothing changes. Is it reasonable to assume that real rates and real growth will be the same for the next 750 years (as per the Japanese example)?

Randy Wray has drawn parallels with Morgan Spurlock’s film “Supersize Me,” in which Morgan decided to see what would happen if he ate food from McDonalds for breakfast, lunch, and dinner for a month. By pursuing this path, Spurlock was consuming around 5000 calories a day, and expending roughly 2500 calories a day. The net calories were enough to generate about a one-pound weight gain per day. An economist watching this would reason along the following lines: This clearly can’t go on forever, at some point Spurlock would be larger than his house, at some point he would be bigger than the earth, and at some point he would be bigger than the entire universe, at which point he would create a black hole and the universe would disappear into it. The problem with such logic is simple: Long before any of this happens he will either change his eating habits or die.

A second issue with the concept of sustainability (as defined by Bernanke) is that because the central bank sets the interest rate for the group of countries we are talking about (those that enjoy monetary sovereignty), they should pretty much always be able to ensure that the real interest rate is below the real growth rate. This ensures that the fiscal position is always “sustainable” as per the above criteria. The obvious issue for Greece (in the chart above) is that it isn’t monetarily sovereign, and also not fiscally sovereign…a decidedly unfortunate situation!

Myth 5: Debt is a burden on future generations

The final myth that I would like to tackle is the idea that debt is somehow a burden imposed by this generation on a future generation. In effect, is the old lady in Exhibit 7 imposing the bill for her hedonistic life style on the two innocents shown?

In the specific, the answer is no. These are in fact my two daughters pictured with their 95-year-old great grandmother. However, it isn’t true in general either. Here is one prediction that I am very nearly absolutely sure about: At some point in the future, everyone alive today will be dead. At that point in time the bonds that make up the government’s debt will be held entirely by our children and grandchildren. That debt will, of course, be an asset for those who own the bonds (just as it is today). There may well be distributional issues if all of those bonds are owned by, say, the grandchildren of Bill Gates, but these will be intragenerational issues, not intergenerational ones.

Thought of another way, let’s imagine that for some strange reason a future generation decides to repay the national debt. Who will they repay it to? Themselves, of course; once again showing that government debt simply can’t be an intergenerational issue.

Why does any of this matter?

It may be a little late in the day after you have just waded through X pages of the above to ask this question. However, from an economic standpoint, given that monetary policy seems to have remarkably little impact upon the economy8 (indeed I would go so far as to say monetary policy is largely impotent with regard to the real economy), fiscal policy offers a real alternative. However, it can be an alternative if, and only if, we understand the nature of government debts and deficits. As the term secular stagnation creeps into the common parlance, and potentially the pricing of assets,9 it is worth remembering that secular stagnation is a policy choice. It could always be ended by the use of fiscal policy.

Intriguingly, a greater reliance upon fiscal policy rather than monetary policy could also be good news for value investors. My colleague, Phil Pilkington, brought the following to my attention as we were discussing some of the issues contained in this paper. Phil found a wonderful quotation from Nicky Kaldor (another of my economic heroes) concerning the role of monetary policy and its interaction with capital markets:

Reliance on monetary policy as an effective stabilising device would involve…a high degree of instability …in the capital market…The capital market would become far more speculative… longer run considerations of … profitability would play a subordinate role. As Keynes said, when the capital investment of a country “becomes the by-product of the activities of a casino, the job is likely to be ill-done.” — Kaldor, 1958

This struck me as very prophetic. Indeed, I would suggest that the elevated valuation that the U.S. market has suffered since Greenspan took the helm at the Fed back in 1987 is a testament to the accuracy of Kaldor’s insight. Whilst monetary policy may not have much impact upon the real economy (except via the debt channel of encouraging households to gear up), it does seem to have influenced an investor’s risk appetite. A move away from the obsession with monetary policy potentially could help generate a return to a more normal world from a valuation perspective.

Kalecki’s insights

Kalecki’s insights

In some ways this brings us back full circle to the very start of this paper and that list of sound finance acolytes. Why do so many very smart people10 subscribe to the edicts of sound finance? In part I think it is because of the extension of the intuition built from the dangers of private debt that I outlined in Myth 1. Ultimately, however, the neglect of fiscal policy stems from political rather than economic foundations. Perhaps the most insightful analysis of the “political problems” with fiscal policy as a policy tool can be found in Kalecki’s excellent analysis from 1943, “Political Aspects of Full Employment.” In this short paper, Kalecki lays out three reasons why “business” doesn’t like the idea of fiscal policy.

“The reasons for the opposition of the “industrial leaders” to full employment achieved by government spending may be subdivided into three categories: (i) dislike of government interference in the problem of employment as such; (ii) dislike of the direction of government spending (public investment and subsidizing consumption); (iii) dislike of the social and political changes resulting from the maintenance of full employment.”

With regard to the “dislike of government interference,” “Every widening of state activity is looked upon by business with suspicion,” and this is especially true with respect to the creation of employment by government expenditure. Kalecki notes that in a system without significant active fiscal policy, business is in the driver’s seat, and their animal spirits may determine the state of the economy. “This gives the capitalists a powerful indirect control over government policy,” he writes. Effectively anything they don’t like will be said to dampen their confidence and thus endanger growth and employment. Because active fiscal policy should reveal that the state can create employment, it must be undermined from the business perspective.

On the “dislike of the direction of government spending,” Kalecki notes that industrial leaders hold a “moral principle of the highest importance” to be at stake. “The fundamentals of capitalist ethics require that ‘you shall earn your bread in sweat’ – unless you happen to have private means.”

Finally, businesses may not like the long-term consequences of the maintenance of full employment. “Under a regime of permanent full employment, the ‘sack’ would cease to play its role as a ‘disciplinary’ measure… ‘discipline in the factories’ and ‘political stability’ are more appreciated than profits11 by business leaders. Their class instinct tells them that lasting full employment is unsound…and that unemployment is an integral part of the ‘normal’ capitalist system.”

Given the evidence of the widespread dominance of the sound finance view across the political spectrum found by examining the list of its adherents that started this note, and Kalecki’s insights, much as I may hope that fiscal policy comes back on the policy agenda, I shan’t be holding my breath.

1 Why this is the workhorse of so many economists is a complete mystery to me. There is, as far as I can tell, no evidence that humans have ever lived in such a system, whereas money/credit/debt seems to appear in very early human societies.

2 The tents in which we all live in this make-believe world.

3 See “Hyperinflations, Hysteria, and False Memories” (February 2013), a white paper available at www.gmo.com.

4 We have attempted to highlight the flaws of this model in our previous papers. See Wicksell’s Red Surstromming in “The Purgatory of Low Returns” (GMO Quarterly Letter, July 2013) and “The Idolatry of Interest Rates, Part 1: Chasing Will ‘o the Wisp” (May 2015)

5 Most economists seem to think in terms of the “financing” of budget deficits as coming from four sources (for example, see Fischer and Easterly, “The Economics of the Government Budget Constraint, World Bank Research Observer” [1990]): budget deficit = money printing + (foreign reserve use + foreign borrowing) + domestic borrowing. In fact budget deficits aren’t “financed” at all; they are always financed by “printing money,” then debt is issued effectively to drain reserves and help the central bank hit its interest rate target. As Lerner noted long ago, “The almost instinctive revulsion that we have to the idea of printing money, and the tendency to identify it with inflation, can be overcome if we calm ourselves and take note that this printing does not affect the amount of money spent.”

6 Bernanke (2012), “The Economic Outlook and the Federal Budget Situation.”

7 ∆d=-s+d*[(r-g)/(1+g)] where s is the primary surplus (the budget position before interest payments), d is the initial level of debt to GDP, r is the real interest rate, and g is the real growth rate.

8 See “The Idolatry of Interest Rates, Part 1: Chasing Will ‘o the Wisp” (May 2015) for more details.

9 See, for example, “The Idolatry of Interest Rates, Part 2: Financial Heresy and Potential Utility in an ERP Framework” where we showed that both bond and equity markets were pricing in very low real rates pretty much forever. This white paper is available at www.gmo.com.

10 It should be noted that even if I am right about functional finance and the role of debts and deficits, a misunderstanding clearly hasn’t impacted a number of the sound finance believers when it comes to investment returns. However, I do worry a little about a halo effect occurring, in as much as we tend to regard the successful as being experts in all areas.

11 Under full employment, everyone would be working and thus spending, which, as per the Kalecki profits equation, would be good for corporate profits.

James Montier is a member of GMO’s Asset Allocation team. Prior to joining GMO in 2009, he was co-head of Global Strategy at Société Générale. Mr. Montier is the author of several books including “Behavioural Investing: A Practitioner’s Guide to Applying Behavioural Finance”; “Value Investing: Tools and Techniques for Intelligent Investment”; and “The Little Book of Behavioural Investing.” Mr. Montier is a visiting fellow at the University of Durham and a fellow of the Royal Society of Arts. He holds a B.A. in Economics from Portsmouth University and an M.Sc. in Economics from Warwick University.

Disclaimer: The views expressed are the views of James Montier through the period ending January 2016, and are subject to change at any time based on market and other conditions. This is not an offer or solicitation for the purchase or sale of any security and should not be construed as such. References to specific securities and issuers are for illustrative purposes only and are not intended to be, and should not be interpreted as, recommendations to purchase or sell such securities.

Copyright © 2016 by GMO LLC. All rights reserved

© GMO