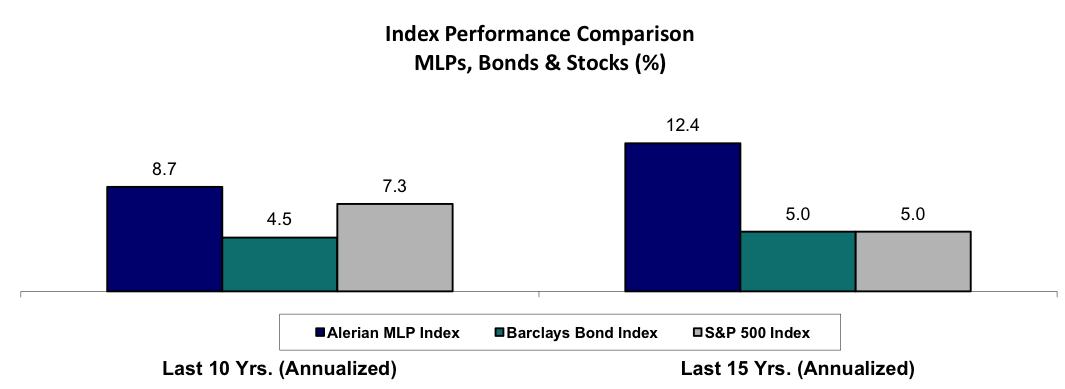

The year 2015 will go down as one of the most disappointing, frustrating, and in the end humbling years for MLPs we expect to experience. Certainly returns for MLPs were disappointing, with the fourth quarter of 2015 posting a -2.8% total return, a suitable end for a year where the index returned -32.6%, the worst one-year return on record except for 2008. What made the returns for MLPs sting especially was that unlike 2008 when all risk assets, credit and equity, posted horrible returns, in 2015 MLPs stood out in their particular horribleness. The S&P 500 Index rallied 7.1% in the fourth quarter bringing its return for the year to 1.4% and fixed income returns were basically flat for the quarter and year. This recent performance has dented the longer term outperformance of MLPs versus bonds and stocks. However, for longer periods MLPs have still outperformed other asset classes, with the 15-year annual return for MLPs more than 7.0% per year above the annual return for U.S. stocks and bonds.

Source: Alerian, Bloomberg. *The inception of the Alerian MLP Index was June 1, 2006, however, Alerian publishes hypothetical index data beginning January 1, 1996. Past performance is not indicative of future results. The referenced indices are shown for general market comparisons and are not meant to represent the Fund. Investors cannot directly invest in an index and unmanaged index returns do not reflect any fees, expenses or sales charges. The Alerian MLP Index does not represent the Eagle MLP Strategy Fund.

There are many reasons that have been pointed to for the poor returns: declining energy prices; the belief we are in a “lower for longer” commodity price regime; the ensuing uncertainty over oil and gas volumes that will be produced in North America in the coming years as a result; and potentially higher interest rates arising from the Federal Reserve’s first increase in policy interest rates since 2006. As a result, the downward trend in equity values that began in the second half of 2014 continued through 2015, effectively closing the equity markets for many MLPs as yields trended up to levels not seen since the financial crisis in 2008. Debt markets subsequently tightened for many MLPs resulting in cash cost of capital becoming prohibitively expensive, if it was even available at all. As a result, many MLPs that needed to access capital markets to fund growth capital spending faced the difficult decision of canceling or postponing growth projects, looking for alternative sources of capital, or reducing current distributions. While most companies choose the first two options, group bell-weather Kinder Morgan opted for a dividend reduction, further adding uncertainty to an already volatile market.

The most frustrating aspect of this market has been that portfolio company 2015 cash flows have mainly come in as we had forecast. Midstream energy infrastructure has largely shown its resilience to weak commodity prices, as expected, since cash flows are based on fees for service and volume commitments. Unlike the oil service industry, MLPs have not offered price discounts to producers. We think this confirmed the quasi-monopolistic character of most midstream infrastructure that underlies stable pricing in the industry. These cash flows have continued to support growing distributions in the aggregate albeit at a slower pace than in the past. This past quarter MLPs in the Alerian MLP Index saw on average an increase in their distribution of 6.4% over the prior year period.

Weighted Average MLP Distribution Increase (YoY)

Source: Alerian. Past performance is not indicative of future results.

Source: Alerian. Past performance is not indicative of future results.

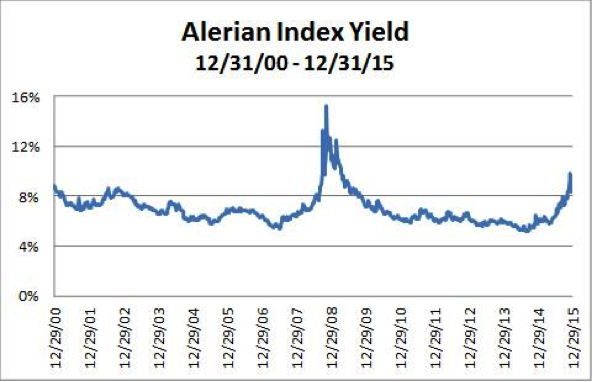

The yield of the Alerian MLP Index was unchanged over the quarter from the beginning yield at 8.3%. In contrast, many other interest rates fell in the quarter, leading to historically high yield spreads of MLPs versus alternative yielding asset classes.

Finally this has been a humbling year to us as investors in the space. Despite the accuracy of our cash flow forecasts and the resilience of the companies to lower energy prices, we did not fully appreciate the impact of macro headwinds on valuations, especially in the area of capital market access. While the industry dealt with unfriendly capital markets very well in 2008 and 2009, it was not in the midst of a capital spending cycle as it is now. Morgan Stanley estimates that MLPs invested nearly $50 billion in new midstream infrastructure in 2015 and has plans for over $40 billion of new investment in 2016. However, since MLPs distribute most of their free cash flow and finance new investment by raising debt and equity in the capital markets, they are especially vulnerable to the whims of investors. Whether prompted by real or imaginary worries, lower MLP equity prices created their own reality, and sparked a vicious circle.

Lower prices meant higher cash cost-of-equity to MLPs; higher cost of equity meant less accretive returns on new investments; lower accretion meant lower potential future growth rates of MLPs distributions, justifying lower MLP equity prices. Rinse, wash, and repeat.

At a time like this, we think it is important to refocus on fundamentals and revisit our most basic thesis. We know that the MLP structure provides a tax-advantaged vehicle for investors that is superior to other modes of corporate organization — the deferred tax on distributions incentivizes MLPs to pay out cash flow to investors while accessing the capital markets for growth instead of retaining cash to fund growth. However, we recognize that going forward this benefit will have to be weighed against the risk of having to go to the capital markets at inopportune times. As a result, some MLPs may rationally choose to retain more of their free cash flow going forward to self-fund growth capital spending, but as long as these projects are well founded and value creating it should not matter greatly to the valuation of the enterprise. Even as commodity and capital market headwinds persist, we have noted a meaningful increase in the number of companies where insider buying is occurring as the year has progressed. In the fourth quarter, we counted insider buying at 19 different MLPs, doubling the amount of companies with insider buying in the first quarter. Despite current low energy prices, the need for energy infrastructure remains; in fact, it is still increasing as we expect North American oil and gas to be in greater demand in the years ahead. While 2015 has been an Annus Horibilis for MLP investors, we think patient investors will be greatly rewarded for staying the course in years to come.

History gives reason for optimism for MLP returns going forward

In every dark cloud there is a silver lining. We looked at past sell-offs of MLPs and found that historically the sector has rebounded over the next 3 years. The worse the sell-off, the stronger the rebound.

|

Alerian MLP Index |

|

|

Drawdown |

Next 3 Year Average Return |

|

10% to 15% |

21.0% |

|

15% to 30% |

25.9% |

|

30% to 45% |

34.9% |

There were five instances since 1995 when the Alerian MLP Index fell from 30% to 45% from peak to trough, and the average annual return after these drops for the index was 34.9% for the subsequent three years.

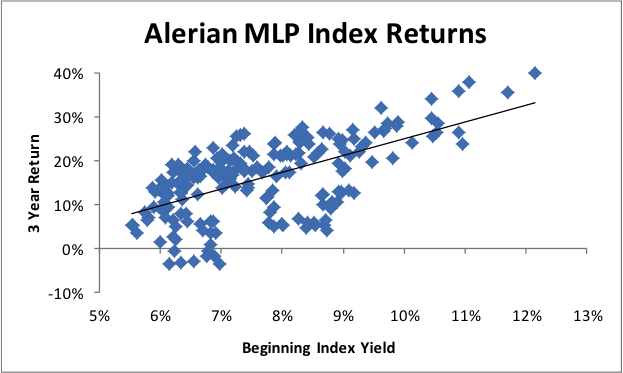

Additionally, future returns of the Alerian MLP Index are higher when the current yield of the index is high (see graph above). At year end, the yield on the index was about 8.3%, which according to the graph above, is historically associated with a subsequent 18% annual, 3-year return for the index.

Underlying these potential returns are compelling valuations which we have not seen since the financial crisis almost six years ago. In fact, this level is higher than it has been outside of the financial crisis period for the last 15 years.

Source: Alerian. Past performance is not indicative of future results. The referenced indices are shown for general market comparisons and are not meant to represent the Fund. Investors cannot directly invest in an index and unmanaged index returns do not reflect any fees, expenses or sales charges. The Alerian MLP Index does not represent the Eagle MLP Strategy Fund.

Yield spreads of MLPs versus other income producing publicly traded assets are at historic highs. MLP yield spread versus corporate bonds (rated Baa) and high yield bonds (rated Ba) are near their highs of the last 20 years (which is the extent of our history); compared with REITs, MLP yields are near their highest spreads experienced in the last 20 years, and versus the 10-year Treasury, are at their highest spread except for the financial crisis period.

Morgan Stanley estimates that the MLP sector is trading at an Enterprise Value-to-EBITDA multiple nearly as low as during the financial crisis (see below).

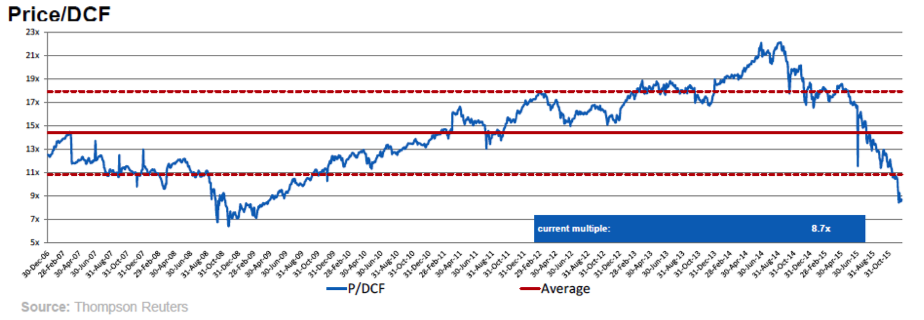

Furthermore, looking at MLPs Price-to-Distributable Cash Flow ratio, as estimated by Morgan Stanley, it is near the lows achieved in the financial crisis.

Capital Market Conditions

The key challenge to the MLP sector in the second half of 2015 was access to the capital markets to fund growth capital spending. As we noted above, we estimate that MLPs spent over $50 billion on new projects in 2015 and given their policy to distribute the bulk of free cash flow, most of that had to be raised in the equity and fixed income markets. After raising about $10 billion of equity in the first half of the year, equity issuance fell dramatically in the second half (to about $3.3 billion, a large part of which was private placements) as equity prices continued to fall. Many MLPs turned to fixed income issuance to bridge the gap, but rising debt-to-equity and debt-to-cash flow measures also limited that avenue of finance.

MLPs have responded in different ways to this challenge. Some MLPs like Enterprise Products and Magellan Midstream, which have pre-funded their capital spending or retain significant cash flow, will likely maintain their plans for growth capital spending and distribution growth. Other MLPs like Plains All American, Oneok, and Targa Resources have announced plans to reduce their capital spending resulting in a materially lower external financing requirement, allowing them to maintain or increase distributions. Others have turned to non-traditional financing sources like convertible preferred equity, private placements, or joint ventures with private equity providers. However, Kinder Morgan elected to cut its distribution by 75% rather than issue equity, lose its investment grade credit rating by issuing more debt, or reducing its capital spending program. We expect that most MLPs will be able to navigate through the current environment by either reducing capital spending (in some cases dramatically) or finding alternative funding measures but recognize that distribution reduction remains a possibility for some. We also expect that a number of mergers or acquisitions may be prompted by this “capital crunch” in the year ahead.

As companies have turned to the bond markets in lieu of the equity markets, credit conditions have become more important. For companies with investment grade ratings, money has become marginally more expensive, but not to levels that discourage issuance. For those companies that rely on the non-investment grade (high yield) bond market, financing has generally become materially more expensive, or in some cases become unavailable. This is partly due to macro issues buffeting the debt markets: a general fourth quarter sell-off in high yield bonds, reversing a multi-year rally; an uptick in defaults from very low levels; and finally concerns about the change in Federal Reserve interest rate policy. But some of the higher rates faced by MLPs reflect specific industry concerns stemming from the rising cost of equity, an overhang of debt funding requirements, and potential counterparty risk from exploration and production customers.

We believe part of the problem in financing capital growth projects comes from the outsized part that retail investors still play in the MLP sector. The average institutional holding of MLPs is about 50% of the float as compared with about 80% for large capitalization stocks in the U.S. We think this is partly the reason for the rise in the correlation of MLP returns with the price of oil and oil producer equities, even for companies that have little to do with the logistics of oil handling. Individual investors are notorious trend followers and fund flows primarily from retail mutual funds, ETFs and ETNs turned sharply negative in the second half of 2015 following negative returns in the first half. We expect that there may be continued volatility in the MLP sector until greater clarity on the capital funding issue is achieved.

The need for new midstream infrastructure continues

Low energy prices are currently discouraging new drilling in North American and have raised questions about the prospects for supply growth and the need for associated new infrastructure. While we expect U.S. oil and gas production to decline in 2016, we remain bullish on the intermediate and long-term prospects. We expect demand for U.S. natural gas to increase about 25% over the next 5 years and 40% over the next 10 years. Globally economies are turning to natural gas as a cheap, clean source of energy, particularly in electricity generation where gas is displacing coal as a fuel source. This trend underpins exports of natural gas to Mexico and overseas by LNG (Liquefied Natural Gas), which we expect to amount to about 10% of current U.S. gas production in 5 years. Also prompted by cheap natural gas and its by products is a boom in the construction of new chemical and industrial plants. The broad-based global trend to natural gas has been termed a “natural gas megatrend” and we believe that the U.S. will continue to need new natural gas infrastructure for years to come to satisfy this demand growth.

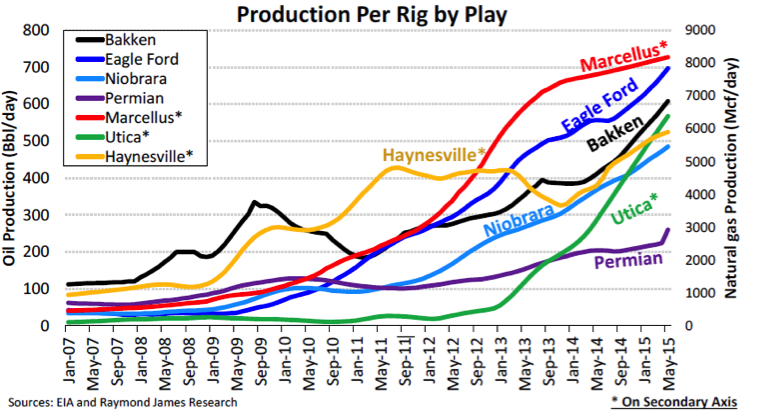

The case for U.S. oil is founded on continued technological advance in drilling and production methods in the shale formations. Recently Raymond James noted the incredible increases in drilling productivity that has already been achieved in the various shale basins where the production per well increased markedly in recent years in response to new technology:

We believe that the current global oversupply of oil has led to an environment where prices have overshot to the downside. Very few basins in the world are able to profitably produce oil at a current price in the low $30 per barrel. As global supply adjusts downward, and demand increases in response to the low price environment, we expect that oil supply / demand will become more balanced towards the end of 2016. In conjunction, prices should stabilize at levels higher than today. U.S. oil production has rolled over and should be down about 5% in 2016. Looking out further, we believe that U.S. shale oil production, aided by great increases in productivity, will become globally cost competitive and will be a major part of meeting the world’s energy needs. Another factor to note is that in comparison to the 1980s when there was great excess capacity in OPEC countries, all OPEC nations are producing near full capacity at the current time and any disruption in supply could quickly lead to markedly different conditions in the oil markets.

Individual company developments

Quarterly earnings reports in the fourth quarter continued to be fundamentally sound for the portfolio with the exception of a few outliers. Kinder Morgan was no exception in terms of reporting relatively good quarterly numbers; however, after announcing a small acquisition for $136 million, the capital markets turned on Kinder Morgan in response to a threat from rating agency Moody to potentially downgrade its debt to below investment grade. With a fully levered balance sheet, a strong desire to keep their investment grade rating, and the desire to maintain its five-year, $20 billion project backlog, the company chose to cut its dividend payout by 75%. Some weeks later, the Teekay family of shipping MLPs found themselves in a similar situation. Weak equity prices and sharply higher yields in the non-investment grade bond market coupled with an unwillingness to defer capital projects led management to make a similar decision and cut the distributions sharply. As we look across the landscape of the rest of the space, we continue to believe that this course of action will be the exception and not the rule.

The year 2015 will be remembered for a number of major mergers and the fourth quarter continued that trend. Targa Resources announced it will acquire its MLP Targa Resource Partners in an all-stock transaction. Similar to the Kinder Morgan consolidation deal announced in 2014, management believes that a simplified structure with no IDR burden and potentially better access to capital is more suitable for this environment. The company is guiding to 10% dividend growth rate in 2016 and modest growth thereafter in its “low case”. Also, similar to Kinder the company expects to be a non-cash tax payer for at least the next 5 years. MarkWest Energy Partners and MPLX completed their merger with Marathon Petroleum Corp (the parent of MPLX) eventually revising its bid higher and offering a greater cash component to ensure a favorable vote from MarkWest shareholders. Energy Transfer Equity continues to push forward with its merger proposal for Williams, and the deal is expected to close in the first half of 2016.

MLPs were also active on the acquisition front. Spectra Energy acquired interests in NGL pipelines from Spectra Energy Partners in exchange for cancelling outstanding common units and general partner units. Spectra Energy subsequently contributed the assets to the private entity DCP, LLC. Along with a cash infusion from the other joint venture partner Phillips 66, this helped to shore up the credit metrics for the private sponsor of DCP Midstream. This serves as another good example where the sponsor relationship gives MLPs an advantage to creatively solve funding and balance sheet hurdles. Rice Midstream did a $200 million private issue to fund a drop-down of water logistics assets from its sponsor. As expected, Tesoro Logistics Partners was able to execute a drop-down for refining logistics assets from its sponsor Tesoro Corp. who also helped finance the deal by taking back units. Shell Midstream Partners continued its torrid pace of drop-down acquisitions from its sponsor Royal Dutch Shell with a $390 million acquisition of midstream assets in November putting the company close to $1.2 billion of acquisitions for the year. Energy Transfer Partners was able to sell $2.2 billion of fuel wholesale and retail assets to a member of the Energy Transfer family, Sunoco LP; the transaction improved ETP’s balance sheet and reduces its need for external financing. Finally, Enlink Midstream Partners bought a large package of midstream assets mainly supporting production in the STACK and Woodford formations in Oklahoma for $1.6 billion from private equity backed Tall Oak Midstream. Likewise, Devon, who owns most of the general partner of Enlink, purchased the production and underlying acreage behind the system from private company Felix Energy for $1.9 billion.

Congress Authorizes Crude Oil Exports

On the last day of 2015, Nustar Energy loaded the first U.S. crude oil export shipment in nearly 40 years. The 400,000 barrel cargo left Nustar’s terminal in the Port of Corpus Christi heading for Europe. Enterprise Product Partners will be close behind as they will be loading a similar cargo for Europe from their terminal in the Houston Ship Channel. These historic events are taking place since Congress passed a $1.1 trillion spending bill which included, among other things, extensions of renewable energy tax credits for another 5 years and the lifting of the crude oil export ban. Unfortunately, the current Brent / WTI spread is now trading near parity (versus a high of almost $15 earlier this year) making significant exports from the U.S. less economic although the spread will likely increase in the future. The lifting of the ban will create an opportunity for MLPs to increase dock capacity and storage at coastal facilities. Many already have existing assets at the Houston Ship Channel, the Port of the Corpus Christi, and the Louisiana Offshore Oil Port (LOOP), a few locations where we see value and the potential need for increased infrastructure. While the new legislation represents a substantial investment opportunity for the midstream, this will occur overtime with the pace directed by the evolving economics of onshore WTI crude oil versus global crude oil. Another notable change on the regulatory front relates to the FERC pipeline index, which governs the maximum annual tariff increases for FERC regulated pipelines owners and is reviewed every five years. The previous index allowed a maximum tariff increase of PPI+2.65%; the new five-year index will be set at PPI+1.23% beginning with the adjustment in July 2016.

Long-Term Prospects for MLPs are Potentially Very Attractive

Despite the returns seen recently for MLPs generally, we are very optimistic about the outlook for MLPs in the long-run. Bottom line, we see the demand for midstream services to continue to expand. While we expect the volumes of oil will decline in the coming quarters, we expect the volumes of gas to be produced will still increase. And while oil is in oversupply for the current time, strong demand growth is being spurred by lower prices. Goldman Sachs recently noted that global oil product demand grew by approximately 1.7 million barrels per day (bpd) in 2015 and they forecast another 1.3 million bpd growth in 2016. This growth is primarily being driven by increases in the demand for gasoline in the U.S., China, and India, to such a point that Goldman Sachs opines that gasoline could be in a “structural shortage” in that global demand for gasoline may exceed global refining capacity. Demand growth of this degree will certainly eat into the excess supply of oil in the coming quarters and years.

David Chiaro

David Chiaro is Co-Head of MLP Strategy for Eagle Global Advisors, LLC

Co-Advisor of the Eagle MLP Strategy Fund

Disclosures:

Investors should carefully consider the investment objectives, risks, charges and expenses of the Eagle MLP Strategy Fund. This and other important information about the Fund is contained in the prospectus, which can be obtained by calling 1-888-868-9501 or visiting www.eaglemlpfund.com. The prospectus should be read carefully before investing. The Eagle MLP Strategy Fund is distributed by Northern Lights Distributors, LLC member FINRA/SIPC. This is an actively managed dynamic portfolio. There is no guarantee that any investment (or this investment) will achieve its objectives, goals, generate positive returns, or avoid losses. The information provided should not be considered tax advice. Please consult your tax advisor for further information. Eagle Global Advisors, Princeton Fund Advisors, LLC and Northern Lights Distributors, LLC are not affiliated.

A master limited partnership (MLP) is a limited partnership that is publicly traded on a securities exchange. It combines the tax benefits of a limited partnership with the liquidity of publicly traded securities. To qualify for MLP status, a partnership must generate at least 90 percent of its income from what the Internal Revenue Service (IRS) deems "qualifying" sources, generally relating to the production, processing or transportation of natural resources, such as oil and natural gas.

The Alerian MLP Index is a composite of the 50 most prominent energy master limited partnerships calculated by Standard & Poor's using a float-adjusted market capitalization methodology.

The S&P 500 Index is a capitalization-weighted index that measures the performance of 500 U.S. large-capitalization domestic stocks representing all major industries.

The Barclays Capital U.S. Aggregate Index provides a measure of the performance of the U.S. investment grades bonds market.

Enterprise Value-to-EBITDA is a multiple used to determine the value of a company. It shows the value of a company based on a multiple of earnings before interest, taxes, depreciation and amortization (EBITDA).

Price-to-Distributable Cash Flow is a valuation ratio calculated by dividing a company’s current stock price by its distributable cash flow per share.

Risk Factors:

Credit Risk: There is a risk that note issuers will not make payments on securities held by the Fund, resulting in losses to the Fund. In addition, the credit quality of securities held by the Fund may be lowered if an issuer’s financial condition changes.

Distribution Policy Risk: The Fund’s distribution policy is not designed to guarantee distributions that equal a fixed percentage of the Fund’s current net asset value per share. Shareholders receiving periodic payments from the Fund may be under the impression that they are receiving net profits. However, all or a portion of a distribution may consist of a return of capital (i.e. from your original investment). Shareholders should not assume that the source of a distribution from the Fund is net profit. Shareholders should note that return of capital will reduce the tax basis of their shares and potentially increase the taxable gain, if any, upon disposition of their shares.

ETN Risk: ETNs are subject to administrative and other expenses, which will be indirectly paid by the Fund. Each ETN is subject to specific risks, depending on the nature of the ETN. ETNs are subject to default risks. Foreign Investment Risk: Investing in notes of foreign issuers involves risks not typically associated with U.S. investments, including adverse political, social and economic developments, less liquidity, greater volatility, less developed or less efficient trading markets, political instability and differing auditing and legal standards.

Interest Rate Risk: Typically, a rise in interest rates can cause a decline in the value of notes and MLPs owned by the Fund.

Liquidity Risk: Liquidity risk exists when particular investments of the Fund would be difficult to purchase or sell, possibly preventing the Fund from selling such illiquid securities at an advantageous time or price, or possibly requiring the Fund to dispose of other investments at unfavorable times or prices in order to satisfy its obligations.

Management Risk: Eagle’s judgments about the attractiveness, value and potential appreciation of particular asset classes and securities in which the Fund invests may prove to be incorrect and may not produce the desired results. Additionally, Princeton’s judgments about the potential performance of the Fund’s investment portfolio, within the Fund’s investment policies and risk parameters, may prove incorrect and may not produce the desired results.

Market Risk: Overall securities market risks may affect the value of individual instruments in which the Fund invests. Factors such as domestic and foreign economic growth and market conditions, interest rate levels, and political events affect the securities markets.

MLP Risk: Investments in MLPs involve risks different from those of investing in common stock including risks related to limited control and limited rights to vote on matters affecting the MLP, risks related to potential conflicts of interest between the MLP and the MLP’s general partner, cash flow risks, dilution risks and risks related to the general partner’s limited call right. MLPs are generally considered interest-rate sensitive investments. During periods of interest rate volatility, these investments may not provide attractive returns. Depending on the state of interest rates in general, the use of MLPs could enhance or harm the overall performance of the Fund.

MLP Tax Risk: MLPs, typically, do not pay U.S. federal income tax at the partnership level. Instead, each partner is allocated a share of the partnership’s income, gains, losses, deductions and expenses. A change in current tax law or in the underlying business mix of a given MLP could result in an MLP being treated as a corporation for U.S. federal income tax purposes, which would result in such MLP being required to pay U.S. federal income tax on its taxable income. The classification of an MLP as a corporation for U.S. federal income tax purposes would have the effect of reducing the amount of cash available for distribution by the MLP. Thus, if any of the MLPs owned by the Fund were treated as corporations for U.S. federal income tax purposes, it could result in a reduction of the value of your investment in the Fund and lower income, as compared to an MLP that is not taxed as a corporation.

Energy Related Risk: The Fund focuses its investments in the energy infrastructure sector, through MLP securities. Because of its focus in this sector, the performance of the Fund is tied closely to and affected by developments in the energy sector, such as the possibility that government regulation will negatively impact companies in this sector. Energy infrastructure entities are subject to the risks specific to the industry they serve including, but not limited to, the following: Fluctuations in commodity prices; Reduced volumes of natural gas or other energy commodities available for transporting, processing, storing or distributing; New construction risk and acquisition risk which can limit potential growth; A sustained reduced demand for crude oil, natural gas and refined petroleum products resulting from a recession or an increase in market price or higher taxes; Depletion of the natural gas reserves or other commodities if not replaced; Changes in the regulatory environment; Extreme weather; Rising interest rates which could result in a higher cost of capital and drive investors into other investment opportunities; and Threats of attack by terrorists.

Non-Diversification Risk: As a non-diversified fund, the Fund may invest more than 5% of its total assets in the securities of one or more issuers. Small and Medium Capitalization Company Risk: The value of a small or medium capitalization company securities may be subject to more abrupt or erratic market movements than those of larger, more established companies or the market averages in general. Structured Note Risk: MLP–related structured notes involve tracking risk, issuer default risk and may involve leverage risk. Mutual Funds involve risk including possible loss of principal.

6063-NLD-1/20/2016