Municipal bonds continue to defy market volatility, offering an oasis of tranquility for investors. Here’s why.

With stock markets grabbing the headlines in January, municipal bonds’ steady performance has received little notice. But for investors seeking a calm port in a storm, munis are looking attractive. As Table 1 shows, a broad index of the municipal-bond market is outperforming equities as well as some fixed-income categories so far in 2016, as it did in all of 2015.

Table 1. Municipal Bonds Have Held Their Own During a Volatile Time

Total return for indicated asset classes for calendar year to date (as of January 21, 2016) and one-year periods ended December 31, 2015

Source: Morningstar and Credit Suisse. “Barclays Aggregate” refers to the Barclays U.S. Aggregate Bond Index. High-yield bonds are represented by the Credit Suisse High Yield Index. “S&P 500” refers to the S&P 500® Index. “MSCI EAFE” refers to the MSCI EAFE (Europe, Australasia, Far East) Index. Emerging-market bonds are represented by the J.P. Morgan Government Bond Index-Emerging Markets (GBI-EM) Global Diversified. Indexes are unmanaged, do not reflect the deduction of fees and expenses, and are not available for direct investment.

Past performance is no guarantee of future results. The historical data are for illustrative purposes only and are not intended to predict or depict future results. Performance during other time periods may differ. Due to market volatility, the market may not perform in a similar manner in the future.

Of course, past performance does not guarantee future results. But there are factors behind municipal bonds’ performance that are distinct from those currently affecting equity and some bond markets, and which suggest that the calm in municipal markets may continue.

This is because, unlike other markets that are being whipsawed by fast-moving global developments—including collapsing oil and commodity prices, slowing growth in China, and currency declines in emerging markets—municipal bonds are influenced largely by three fundamental factors that are U.S.-focused. These are the state of the U.S. economy, bond-issuer supply, and individual investor demand for munis—each of which continues to provide support for the asset class.

- U.S. economy—Most data indicate that the U.S. economy is showing steady, though not overly strong, growth, along with low inflation. As the broader economy grows, state tax revenues are increasing, strengthening municipal budgets.

- Supply—Given the moderate growth of the U.S. economy, we expect the Federal Reserve Board to increase interest rates at a slow and measured pace in 2016. This means that interest rates will remain at attractively low levels, increasing the likelihood of another large volume of refunding in 2016, as occurred in 2015. But new issues continue to be few as municipalities delay infrastructure spending. So, net supply is expected to be flat—and therefore, not overwhelming demand.

- Demand—The lower volatility and positive price performance of the municipal bond market in 2015 is attracting investors to the asset class and increasing fund flows. Year to date (through January 20, 2016), net inflows to tax-free funds totaled $4.4 billion, according to Lipper. We expect demand to remain relatively strong, supporting market stability in 2016.

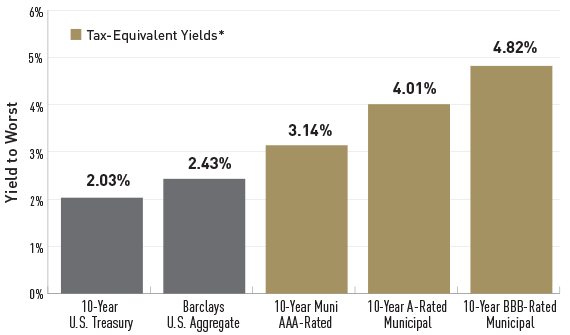

Adding to demand is the fact that, even after their recent outperformance, munis still present attractive relative value versus their taxable counterparts. While muni yields are not elevated, compared with historical standards, Chart 1 shows that they are still high, on a taxable-equivalent basis, relative to similar-risk alternatives, such as the yields on 10-year U.S. Treasury bonds and the broader bond market (as represented by the Barclays Aggregate U.S. Bond Index, as of January 22, 2016).

Chart 1. Tax-Equivalent Yields on Munis Remain Attractive

Yield to worst, January 22, 2016

Source: Barclays and Bloomberg.

Government bonds are represented by the Bloomberg World Bond Government Bond listings. “Barclays Aggregate” refers to the Barclays U.S. Aggregate Bond Index. All the rest are represented by the Bloomberg Fair Value Yield Curve. *At the 28% tax bracket, the tax-equivalent yield would be 2.47%, 3.15%, and 3.79% for the ‘AAA’ rated, ‘A’ rated, and the ‘BBB’ rated segment of the Bloomberg Fair Value Yield Curve, respectively. Tax-equivalent yield calculation for the municipal indexes above assumes the top marginal tax bracket of 43.4% on investment income, which includes the 39.6% income tax rate and the 3.8% in Medicare tax. This tax rate does not factor in the effect of AMT (alternative minimum tax) or taxes in your individual state. Tax-equivalent yield will vary based on an investor’s tax bracket.

Past performance is no guarantee of future results. For illustrative purposes only and does not reflect any Lord Abbett mutual fund or any particular investment. Lower-rated bonds may carry greater risks than higher-rated bonds. Income from municipal bonds may be subject to the alternative minimum tax. Federal, state, and local taxes may apply.

Ten-year Treasury yields have remained low (2.03% as of January 22, 2016) in the recent flight to quality, but it’s worth noting that investors are getting almost the same yield tax-free (1.78%, or 88% of the 10-year U.S.Treasury) on a similar-duration ‘AAA’ municipal bond. For investors looking to make an allocation to high-quality intermediate muni bonds, the taxable-equivalent yield on that sector is an attractive alternative to high-quality intermediate taxable bonds, such as the Barclays Aggregate Bond Index which offers a yield of 2.43%.

According to Stephen Hillebrecht, Lord Abbett Fixed-Income Product Strategist, there is an even more interesting opportunity by dipping down a notch in credit quality to the lower end of the investment-grade sector. According to Bloomberg, the average yield on 10-year ‘A’ rated municipal bonds was at 2.27% (as of January 22, 2016), while 10-year ‘BBB’ rated municipals offered an average yield of 2.73%. On a taxable-equivalent basis, these yields are 4.01% and 4.82%, respectively, as calculated from the highest tax-bracket of 43.4%, and 3.15% and 3.79%, respectively, as calculated from the 28% tax-bracket, making them much more attractive than the yields offered by the 10-year U.S. Treasury or the Barclays U.S. Aggregate Bond Index.

Does this increased yield come with greatly increased risk? Not necessarily. In 2015, the financial media focused on the few trouble spots of the muni market, such as Illinois and Puerto Rico. But historically, defaults are infrequent in the muni market. As we discussed in our August 17, 2015 Market View, default rates have been extremely low in investment grade municipal bonds.

Additionally, in 2015 the major credit rating agencies released more upgrades than downgrades of municipal bond issuers. We think this trend is likely to continue in 2016, given the outlook for an improving U.S. economy and the increase in tax revenues that would accompany more economic activity, adding to the stability of the municipal market.

We would be remiss in not reminding investors that, over the long term, equities offer the opportunity to generate higher total return than municipal bonds. Moreover, recent volatility may present opportunities and more attractive valuations not only in equities but in other asset classes that have suffered, such as high-yield bonds.

But, for those investors who are losing sleep at night because of the current volatility in the stock market, municipal bonds are an asset class that may offer the relative tranquility they seek, with the additional opportunity to realize an attractive total return.

A Note about Risk: The value of investments in debt securities will fluctuate in response to market movements. Lower-rated bonds carry greater risks than higher-rated bonds. Investments in high-yield securities (sometimes called junk bonds) carry increased risks of price volatility, illiquidity, and the possibility of default in the timely payment of interest and principal. When interest rates rise, the prices of debt securities are likely to decline, and when interest rates fall, the prices of debt securities tend to rise. A portion of the income derived from a municipal bond may be subject to the alternative minimum tax. Any capital gains realized may be subject to taxation. Federal, state, and local taxes may apply. There is a risk that a bond issued as tax-exempt may be reclassified by the IRS as taxable, creating taxable rather than tax-exempt income. Bonds may also be subject to other types of risk, such as call, credit, liquidity, interest-rate, and general market risks. Investments in Puerto Rico and other U.S. territories, commonwealths, and possessions may be affected by local, state, and regional factors. These may include, for example, economic or political developments, erosion of the tax base, and the possibility of credit problems. No investing strategy can overcome all market volatility or guarantee future results.

Tax-equivalent yield is the yield that a taxable bond would have to pay to be equal to the yield of a tax-free municipal bond. The tax-equivalent yield varies, depending on the investor’s income tax bracket.

Yield is the annual interest received from a bond and is typically expressed as a percentage of the bond's market price.

Yield to worst is the lowest yield that can be paid on a bond, assuming the issuer does not default. The calculation takes into consideration worst-case scenarios in which the bond would be paid prior to maturity. It is assumed the bond will be prepaid if current interest rates are lower than the current coupon rate.

The Barclays U.S. Aggregate Bond Index represents securities that are SEC-registered, taxable, and dollar denominated. The index covers the U.S. investment grade fixed rate bond market, with index components for government and corporate securities, mortgage pass-through securities, and asset-backed securities. Total return comprises price appreciation/depreciation and income as a percentage of the original investment.

The Barclays Municipal Bond Index is a rules-based, market-value-weighted index engineered for the long-term tax-exempt bond market. The index is a broad measure of the municipal bond market with maturities of at least one year. To be included in the index, bonds must be rated investment-grade (Baa3/BBB- or higher) by at least two of the following ratings agencies: Moody's, Standard & Poor's, Fitch. If only two of the three agencies rate the security, the lower rating is used to determine index eligibility. If only one of the three agencies rates a security, the rating must be investment-grade. Bonds must have an outstanding par value of at least $7 million and be issued as part of a transaction of at least $75 million. The bonds must be fixed rate, have a dated-date after December 31, 1990, and must be at least one year from their maturity date.

The Credit Suisse High Yield Index is an unmanaged, trader-priced index constructed to mirror the characteristics of the high-yield market. The index includes issues rated ‘BB’ and below by S&P or Moody’s, with par amounts greater than $75 million.

The J.P. Morgan Government Bond Index-Emerging Markets (GBI-EM) Global Diversified is a comprehensive global emerging markets index that consists of regularly traded, liquid fixed-rate and domestic currency government bonds.

The MSCI EAFE Index (Europe, Australasia, Far East) is a free float-adjusted market capitalization index that is designed to measure the equity market performance of developed markets, excluding the US & Canada. The MSCI EAFE Index consists of the following 21 developed market country indexes: Australia, Austria, Belgium, Denmark, Finland, France, Germany, Hong Kong, Ireland, Israel, Italy, Japan, the Netherlands, New Zealand, Norway, Portugal, Singapore, Spain, Sweden, Switzerland, and the United Kingdom. MSCI makes no express or implied warranties or representations and shall have no liability whatsoever with respect to any MSCI data contained herein. The MSCI data may not be further redistributed or used as a basis for other indices or any securities or financial products. This report is not approved, reviewed or produced by MSCI.

The S&P 500® Index is widely regarded as the standard for measuring large cap U.S. stock market performance and includes a representative sample of leading companies in leading industries.

Indexes are unmanaged, do not reflect the deduction of fees or expenses, and are not available for direct investment.

The credit quality ratings of the securities in a portfolio are assigned by a nationally recognized statistical rating organization (NRSRO), such as Standard & Poor's, Moody's, or Fitch, as an indication of an issuer's creditworthiness. Ratings range from 'AAA' (highest) to 'D' (lowest). Bonds rated 'BBB' or above are considered investment grade. Credit ratings 'BB' and below are lower-rated securities (junk bonds). High-yielding, non-investment-grade bonds (junk bonds) involve higher risks than investment-grade bonds. Adverse conditions may affect the issuer's ability to pay interest and principal on these securities.

The opinions in Market View are as of the date of publication, are subject to change based on subsequent developments, and may not reflect the views of the firm as a whole. The material is not intended to be relied upon as a forecast, research, or investment advice, is not a recommendation or offer to buy or sell any securities or to adopt any investment strategy, and is not intended to predict or depict the performance of any investment. Readers should not assume that investments in companies, securities, sectors, and/or markets described were or will be profitable. Investing involves risk, including possible loss of principal. This document is prepared based on the information Lord Abbett deems reliable; however, Lord Abbett does not warrant the accuracy and completeness of the information. Investors should consult with a financial advisor prior to making an investment decision.