Oh, market volatility — your foul stench is particularly rancid in the dark of winter, when the taxman begins his rounds and rebalancing fills investors' minds.

But, as goes January, so goes the year? Not so fast.

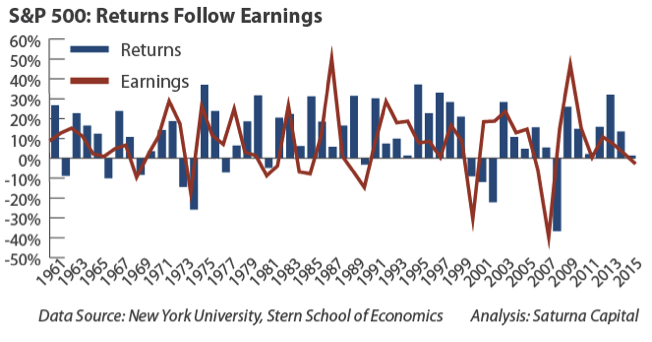

It is not unusual to have a down January. Since 1961, about a third of the years have seen a January with negative equity market returns: 19 of 55, to be exact.

Of these 19, only six had years where earnings declined, the rest saw increases in earnings. On average, the S&P 500 Index returned 3.56% in these 19 years. However, when earnings increased for those years when January was negative, the return increased to 6.51%.

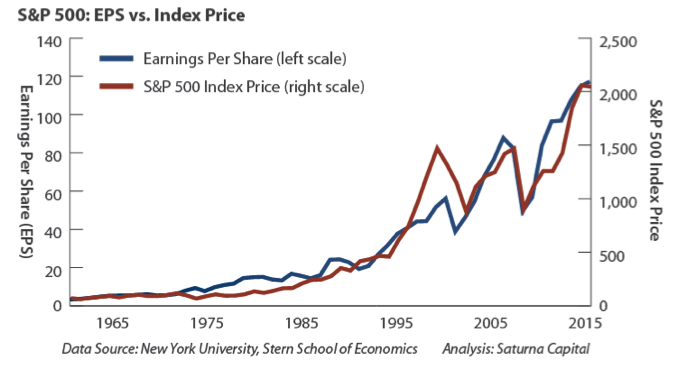

Admittedly, earnings growth has slowed, but it remains positive. Ultimately, market prices tend to follow earnings.

In Saturna's view, low earnings growth leads to higher market volatility. For bonds, the lower the yield, the higher the volatility. Similarly for equities, the lower the earnings yield, the higher the volatility in the face of even small declines in earnings estimates.

There have been six occasions where there were two down January years in a row. 2015 – 2016 looks to be another. However, there's only been one occasion where January was lower THREE years in a row. Also, the year of the second down January tends to produce exceptional returns (23% on average).

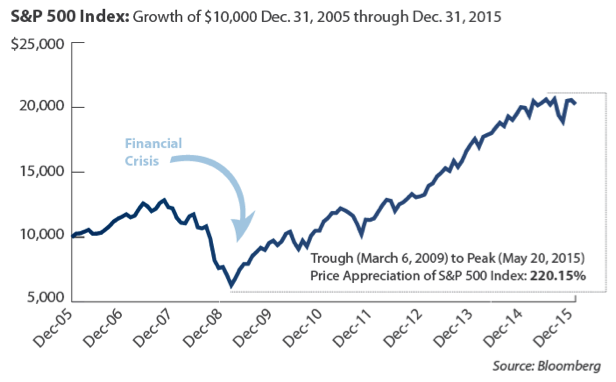

Anxiety often follows high volatility and the likelihood of acting on "gut instinct" increases. Gut Instinct can easily lead one astray. If your investment horizon is longer than a couple of years, we remind you of the financial crisis of 2007 – 2009. As painful as the "Great Recession" was, if you sold at the bottom, you missed out on the 220.15% equity bull market, trough to peak.

While jarring, occasional market gyrations are not your greatest risk. Your greatest risk is not being invested, while attempting to time markets only benefits those collecting commissions.

Copyright 2016 Saturna Capital Corporation and/or its affiliates. All rights reserved. Vol. 10 · No. 1

Important Disclaimers and Disclosures

Performance data quoted represents past performance which is no guarantee of future results.

This publication should not be considered investment, legal, accounting, or tax advice or a representation that any investment or strategy is suitable or appropriate to a particular investor's circumstances or otherwise constitutes a personal recommendation to any investor. This material does not form an adequate basis for any investment decision by any reader and Saturna may not have taken any steps to ensure that the securities referred to in this publication are suitable for any particular investor. Saturna will not treat recipients as its customers by virtue of their reading or receiving the publication.

The information in this publication was obtained from sources Saturna believes to be reliable and accurate at the time of publication.

All material presented in this publication, unless specifically indicated otherwise, is under copyright to Saturna. No part of this publication may be altered in any way, copied, or distributed without the prior express written permission of Saturna.