KEY TAKEAWAYS

· Our Five Forecasters indicators are sending mid-cycle signals, although stock valuations, the ISM Manufacturing Index, and market breadth have flashed some warning signs.

· Although volatility may remain high, we expect the latest stock market correction will not turn into a bear market.

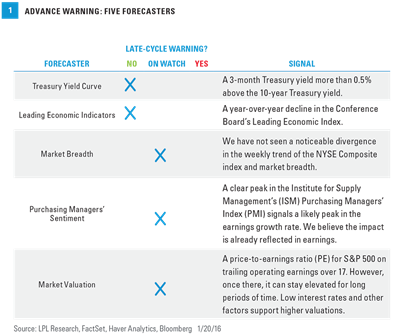

The Five Forecasters still favor the continuation of the current bull market and no recession. The Five Forecasters, which we first introduced in 2014, are five indicators that, collectively, have historically signaled the increasing fragility of the U.S. economy and a transition to the late stage of the economic cycle and an oncoming recession.

Currently, these indicators are generally sending mid-cycle signals (similar to our cycle clock from Outlook 2016). Three of the five indicators are flashing a warning signal and suggest the cycle may have moved past the midpoint, while two of them are still benign [Figure 1]. Here we review these five indicators, which still signal that this bull market may continue and that the latest S&P 500 correction may stop short of a 20% decline.

Bear market declines of 20% or more for stocks are not always accompanied by a recession, although more often than not, that is the case. Accordingly, we believe these indicators can be used to give some advance warning of an impending bear market. The average S&P 500 decline in a bear market historically is about 33%, compared to the 12% peak-to-trough decline from the all-time high on May 21, 2015, through January 20, 2016.

LEADING ECONOMIC INDICATORS: NO WARNING

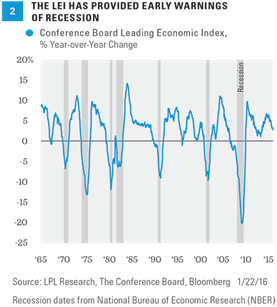

Among the Five Forecasters, the Conference Board’s Leading Economic Index (LEI) provides the best snapshot of the overall health of the economy. The LEI is an aggregate of 10 diverse economic indicators that have historically tended to lead changes in the level of economic activity. The index includes data on employment, manufacturing, housing, bond yields, the stock market, consumer expectations, and housing permits. Taken together, these indicators have a strong history of forecasting the path of the economy with a lead time of 6–12 months. The year-over-year change in the LEI has also provided an effective warning signal that the economy might be nearing a recession. When the year-over-year change has turned from positive to negative, on a year-over-year basis, a recession has followed in anywhere from 0–14 months with an average lead time of 6 months.

The year-over-year change in the LEI as of December 2015 was +2.7% [Figure 2]. Since 1960, when the LEI has been 2.7% or higher, the economy has been in recession for only one isolated month over its 672-month history, or 0.1% of the time, and the economy has entered recession in the next 12 months only 5% of the time. Even when the year-over-year change has been 2–4%, the economy has entered recession over the next 12 months less than 10% of the time. While the economy right now is showing a mix of early, mid, and late cycle signals, we agree, on balance, with the statistical evidence that the likelihood of a recession in the next year remains low.

TREASURY YIELD CURVE: NO WARNING

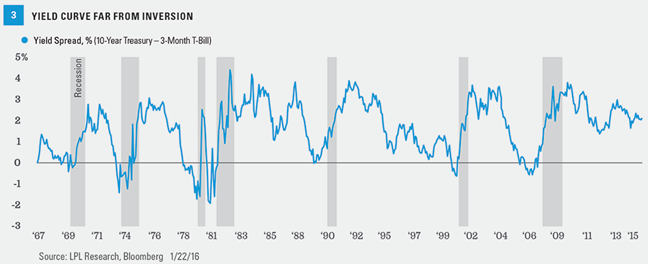

Now that the Federal Reserve (Fed) has initiated the process of normalizing interest rates, some fear a recession may not be far behind. However, history shows that the start of rate hikes does not matter much to stocks after an initial dip and quick recovery. Instead, bull markets have historically ended (and bear markets have begun) when the Fed pushes short-term rates above long-term rates. This is referred to as “inverting the yield curve.” For example, the S&P 500 Index peaked in 2000 and 2007 when the 3-month to 10-year Treasury yield curve was inverted by about 0.5% (3-month Treasury yields were about 0.5% above the yield on the 10-year Treasury note).

Why does an inverted yield curve signal a major peak for the stock market? Because every recession over the past 50 years was preceded by the Fed hiking rates enough to invert the yield curve. That is 7 out of 7 times—a perfect forecasting track record. The yield curve inversion usually takes place about 12 months before the start of the recession, but the lead time has ranged from about 5–16 months. The peak in the stock market comes around the time of the yield curve inversion, ahead of the recession and accompanying downturn in corporate profits.

With the 3-month Treasury and 10-year Treasury currently yielding 0.28% and 2.05%, respectively, the Fed must push up short-term rates by nearly 2.30% to invert the yield curve by 0.5%. Based on the latest internal Fed survey, the Fed does not expect to raise the fed funds rate above 3% until sometime in 2017, at the earliest. The facts suggest that one of the best indicators for the start of a bear market may still be a long way from signaling a cause for concern [Figure 3].

ISM SURVEY: ON WATCH

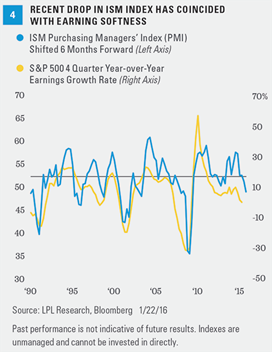

The Institute for Supply Management (ISM) Manufacturing Index has historically been a good earnings indicator. Earnings are the most fundamental driver of the stock market, and therefore, should be a part of any recession or bear market watch checklist. The ISM is an association of purchasing and supply management professionals who are surveyed each month to assess their future plans; the results of the survey are then used to create an index. Because purchasing managers are on the front line when it comes to the manufacturing supply chain, they can provide signals ahead of economic turning points. With about two-thirds of S&P 500 profits tied to manufacturing, manufactured goods demand has still been a timely barometer of all types of economic activity in recent decades.

The ISM has a solid track record of forecasting earnings growth over the next 6 months [Figure 4]. A peak in the ISM, as occurred in late 2014, did indicate an ensuing slowdown in profits. Pulled down by energy sector weakness and a strong U.S. dollar, this indicator continues to signal an earnings lull and is one to watch closely. We believe the index may stabilize in early 2016 and that this period of earnings weakness will end up resembling the mid-cycle dips experienced in the mid-1980s, mid-1990s, and 2012, periods when the ISM dipped below 50 that were not followed by recession.

MARKET BREADTH: ON WATCH

Analyzing market breadth has been a useful tool to help provide some advance warning of recessions and bear markets. We track market breadth by looking at the number of stocks that are advancing minus those that are declining. By tracking how many stocks are participating in a rally, or sell-off, we can get a sense of how broad and durable a rally may be. A market that is rising on the strength of fewer and fewer stocks is more vulnerable to a decline. If market breadth begins to decline and diverges from the rise in the NYSE Composite Index, and is followed by a decline in the index as it begins to succumb to the dwindling number of stocks in the index that are still rising, the likelihood of a major market downturn and recession increases (we use the NYSE Composite because of its many constituents).

Over the past 6 months, we have not seen a noticeable divergence in the weekly trends of the NYSE Composite Index and market breadth [Figure 5]; both patterns are moving in the same direction, downward. This indicates that both NYSE Composite Index prices and a large number of its constituents (breadth) have been moving lower during this time frame. We interpret the absence of a meaningful divergence between price and breadth prior to the current correction to mean that the stock market’s ascent in 2015 had a stronger foundation than it did ahead of prior recessions.

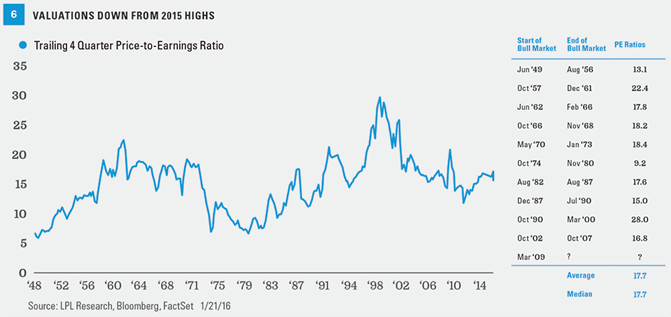

STOCK VALUATIONS: ON WATCH

Stock market valuation is a poor market-timing indicator. There is no statistical relationship between what investors are willing to pay today for earnings over the past year, as measured by the price-to-earnings ratio (PE), and how stocks perform over the following year. However, the PE is a good indicator of long-term stock returns and can help tell us when the market has become fully valued and may be more vulnerable to deterioration in the economic cycle, which is why we have included it as one of our Five Forecasters. A higher PE implies a more optimistic earnings outlook, which introduces more risk of disappointment if that growth outlook does not materialize.

The stock market’s recent decline has brought the S&P 500 trailing price-to-earnings ratio (PE) down to 16. But the 2015 highs near 18, reached in May and sustained through much of the summer, were in the range where stocks have traded historically when bull markets have ended [Figure 6]. The good news is we are now below the post-1980 average of 16.4, and nowhere even remotely close to the record highs at the peak of the internet bubble in 2000, providing some potential for PE expansion should the growth outlook improve from here. But we are still above the longer-term average of 15.3 going back to 1950. At this point we would characterize valuations as flashing a warning signal because of the PE levels reached in 2015, and, assuming no recession or bear market in 2016, would look for a return to the previous range before this signal becomes more worrisome.

CONCLUSION

The Five Forecasters continue to signal economic growth and the continuation of the bull market, not a recession or bear market. The yield curve and Index of Leading Economic Indicators are sending clear positive signals. Meanwhile, the signals from the indicators that have flashed some warning signs, i.e., stock valuations, the ISM Manufacturing Index, and market breadth, are more mixed and consistent with a mid-cycle correction rather than recession. So although volatility may remain high, we expect the latest stock market correction may stop short of a bear market. We continue to watch these and other indicators to inform our tactical asset allocation views.

IMPORTANT DISCLOSURES

The opinions voiced in this material are for general information only and are not intended to provide specific advice or recommendations for any individual. To determine which investment(s) may be appropriate for you, consult your financial advisor prior to investing. All performance referenced is historical and is no guarantee of future results.

The economic forecasts set forth in the presentation may not develop as predicted and there can be no guarantee that strategies promoted will be successful.

Investing in stock includes numerous specific risks including: the fluctuation of dividend, loss of principal, and potential liquidity of the investment in a falling market.

All investing involves risk including loss of principal.

The PE ratio (price-to-earnings ratio) is a measure of the price paid for a share relative to the annual net income or profit earned by the firm per share. It is a financial ratio used for valuation: a higher PE ratio means that investors are paying more for each unit of net income, so the stock is more expensive compared to one with lower PE ratio.

Because of its narrow focus, investing in a single sector, such as energy or manufacturing, will be subject to greater volatility than investing more broadly across many sectors and companies.

INDEX DESCRIPTIONS

The Standard & Poor’s 500 Index is a capitalization-weighted index of 500 stocks designed to measure performance of the broad domestic economy through changes in the aggregate market value of 500 stocks representing all major industries.

The Institute for Supply Management (ISM) Index is based on surveys of more than 300 manufacturing firms by the Institute for Supply Management. The ISM Manufacturing Index monitors employment, production inventories, new orders, and supplier deliveries. A composite diffusion index is created that monitors conditions in national manufacturing based on the data from these surveys.

The NYSE Composite Index measures the performance of all stocks listed on the New York Stock Exchange. The index includes more than 1,900 stocks, of which over 1,500 are U.S. companies. Its breadth therefore makes it a much better indicator of market performance than narrow indexes that have far fewer components.