Not too much further we think. As we’ve seen over the first few weeks of 2016, WTI (West Texas Intermediate) crude has been down as much as 25% from last year end 2015.1 Prices per barrel also closed below $30 for the first time since 2003.2

According to our investment manager research, the same bearish factors that surfaced in 2015 continue to persist: a market that is estimated to be oversupplied to the tune of 1 million to 2 million barrels a day (MBD), posturing by Saudi Arabia and other OPEC (Organization of Petroleum Exporting Countries) members as they defend market share over price, U.S. shale production that remains resilient in spite of significant declines in rig activity3, a strong US dollar (USD), and consistently bearish sentiment by investors.

We believe that many of these forces should begin to shift, and the decline into (and below) $30 a barrel may expedite the adjustments necessary to push crude oil prices back into a higher equilibrium range. Why do we think this?

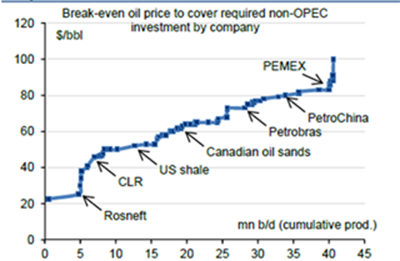

First, there is significant financial pressure on non-OPEC suppliers. The majority of non-OPEC oil production requires prices well in excess of $30 a barrel to operate profitably. As noted in the chart below, Bank of America Merrill Lynch (BofA Merrill Lynch) estimates the long-term breakeven price to be closer to $80 per barrel for non-OPEC suppliers.4

Source: BofA Merrill Lynch Global Research. December 22, 2015.

Secondly, global production figures have yet to respond to significant cuts in producer capital expenditure and rig activity.U.S. shale, in particular, has held relatively firm at 9.2MBD for the last three months (through December 2015) after falling from a record high 9.7MBD last summer.5 Efficiency gains, financing lifelines and hedging activity have been credited for the resilience of U.S. shale producers, but we believe their tolerance for low prices will be tested in the coming months. Cash costs, or the absolute minimum price required to keep operations afloat, have come down in recent months, but our research still estimates the $20 to $30 range to be the most efficient for shale producers.

Additionally, according to our internal research and discussions with external investment managers, Saudi Arabia has elected to draw from its foreign reserves (to the tune of $10-$12 billion per month in 2015) instead of defending prices as oil revenues have fallen dramatically. Iraq continues to produce at their estimated capacity and Iran is expected to add another 300,000 to 500,000 barrels a day to global markets as sanctions are lifted.

However, we see signs of a shift in 2016. In our conversations with external investment managers on January 22, we learned that a number of significant global producers have recently reigned in guidance for 2016.

While U.S. producers continue to emphasize cost reductions and growth, we believe that their time may be running short at these price levels and the market is beginning to reflect that:

- Moody’s recently placed 120 oil and gas companies on review for a ratings downgrade. This includes 69 U.S.-based exploration as well as production and services firms.6

- High-yield bond spreads for exploration and production companies are close to the all-time levels reached in 2008 and are implying a cumulative loss of 86% for the sector.7

- Stresses on the energy lending bank sector are coming under focus. Our research has found estimates that U.S. equity markets are pricing in losses of 12.5% for the space, which would exceed losses seen during the downturn during the 1980’s.

- Forward curves (which are the current price for a commodity in a specific location on a specified date in the future)8 have fallen to levels that prohibit shale producers from hedging production. The WTI curve is below $40 all the way out to 2018, below most producers breakeven costs and well below the $50 estimated to incentivize production growth.9

So what does all this mean? We believe oil has reached price levels that are low enough to create a significant strain on producers, and that strain will inevitably lead to the fundamental changes in production in the oil supplier market to shift prices to higher. We expect that this transition will play out over the first half of 2016, and perhaps longer, before oil moves into a meaningfully higher trading range.

Given these circumstances, while we are still underweight commodities in many of our strategies, that underweight has diminished in recent weeks. From a portfolio perspective, we believe now may be a beneficial time to consider removing underweights to energy or explore opportunities to add energy exposures in 2016.

For more about how low oil prices may impact the European economy this year, see our 2016 Eurozone Outlook.

1 FactSet WTI Price search as of January 20, 2016.

2 FactSet WTI Crude Index search as of January 15, 2016.

3 Rig activity and shale production searches on Bloomberg as of January 22, 2016.

4 Source: BofA Merrill Lynch Global Research, Global Energy Weekly, Relative Value in Oil. December 22, 2015.

5 Search for MBD figures on Bloomberg as of January 22, 2016.

6 Search for oil and gas companies ratings on Thomson Reuters. January 22, 2016.

7 Russell Investments manager research. January 2016.

8 Future Curve also called Forward Price Curve is the current price for a commodity in a specific location on a specified date in the future. A Future Curve consists of a series of forwarded prices plotted together, reflecting a range of today’s tradable values for specified dates in the future.

9 FactSet, Tudor Pickering Holt search for WTI Crude Index and WTI Crude pricing. As of September 28, 2015.

Disclosures

Nothing contained in this material is intended to constitute legal, tax, securities or investment advice, nor an opinion regarding the appropriateness of any investment, nor a solicitation of any type.

These views are subject to change at any time based upon market or other conditions and are current as of the date at the top of the page. The information, analysis, and opinions expressed herein are for general information only and are not intended to provide specific advice or recommendations for any individual or entity.

Investing involves risk and principal loss is possible.

Forecasting is inherently uncertain and may be incorrect. It is not representative of a projection of the stock market, or of any specific investment.

Commodity futures and forward contract prices are highly volatile. Trading is conducted with low margin deposits which creates the potential for high leverage. Commodity strategies contain certain risks that prospective investors should evaluate and understand prior to making a decision to invest. Investments in commodities may be affected by overall market movements, and other factors such as weather, exchange rates, and international economic and political developments. Other risks may include, but are not limited to; interest rate risk, counter party risk, liquidity risk and leverage risk. Potential investors should have a thorough understanding of these risks prior to making a decision to invest in these strategies.

The general information contained in this publication should not be acted upon without obtaining specific legal, tax and investment advice from a licensed professional. The information, analysis and opinions expressed herein are for general information only and are not intended to provide specific advice or recommendations for any individual entity.

Russell Investments is a trade name and registered trademark of Frank Russell Company, a Washington USA corporation, which operates through subsidiaries worldwide and is a subsidiary of London Stock Exchange Group.

Copyright © Russell Investments 2016. All rights reserved.

This material is proprietary and may not be reproduced, transferred, or distributed in any form without prior written permission from Russell Investments. It is delivered on an “as is” basis without warranty.

UNI – 10731