Giving a Little Credit to High Yield

Ben Inker

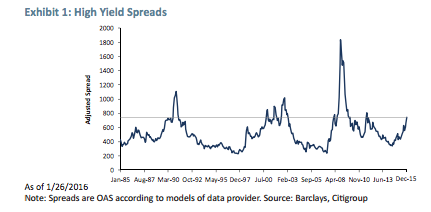

The year 2015 was not a banner year for financial assets around the world. Emerging market stocks had a particularly rough time of it, as did value stocks practically everywhere. But we at GMO spend a lot of time talking about emerging market and value stocks, so I’m going to shake things up a bit by talking about another asset class that had a notably bad year, U.S. high yield corporate bonds. The Barclays U.S. Corporate High Yield index fell 4.5% for the year, which doesn’t sound that horrible, but when you consider that it did have a coupon of about 6% and has a duration of less than 5 years, that loss corresponds to a pretty big drop in price for the average high yield bond and about 200 basis points of spread widening. I say “about 200 basis points” because one of the interesting features of the high yield market is that no two index providers agree on all that much about the market. The Bank of America Merrill Lynch (BoA) version of high yield, while it had similar performance for the year to the Barclays index, shows significantly wider spread and more widening during the year. Part of this is due to BoA including defaulted bonds in its universe and part to a different calculation of option adjusted spreads (OAS)1 for high yielding bonds, which actually has a pretty material effect on the averages. This means, unfortunately, that there is no simple answer to the question “What is the spread on high yield today?” or even “What is the yield on high yield today?” But what all of the answers to that question agree on today is that spreads as of the end of 2015 (and even more so as of the latter part of January 2016) are significantly wider than their long-term averages, as we can see in Exhibit 1.

This raises the important question: Is high yield debt cheap today? There is no particularly easy answer to this question given the nature of high yield, but the short answer is “probably” with a strong suspicion that it is not worse than fair value. In an environment where very few assets around the world are even particularly close to fair value,2 that statement seems like a pretty strong endorsement. And over the course of 2015 we were steady buyers of selected high yield names in our Benchmark-Free Allocation Strategy (BFAS). We did so cautiously, believing that default rates were likely to rise over the next few years. Our careful approach was rewarded, as our portfolios of high yield and distressed assets in BFAS made decent money in a down year for the asset class, and our holdings of structured debt also made money on the year. We are continuing to increase our holdings of high yield and distressed assets and expect to keep buying over the next several months as long as spreads stay near current levels or continue to widen. We are not yet leaping into high yield with both feet, however, for a couple of reasons. First, our suspicion is that we are likely entering a new “default cycle” where default rates on high yield bonds rise above long-term averages. And second, there are a number of features of the high yield market that indicate it is particularly likely to overshoot fair value as defaults rise.

The default cycle

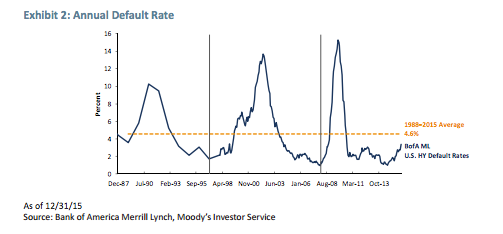

Coming up with a fair value estimate for high yield bonds is impossible without calculating expected losses due to defaults. While it might be tempting to simply use long-term average default rates and call it a day, the trouble is that defaults are far from constant over time, as can be seen in Exhibit 2.

The long-term average default rate may be 4.6% since 1988, but on an annual basis we have seen figures above 15% and below 1%. A yield spread over treasuries that would give wonderful returns at a 1% default rate would leave you crying over your brokerage statements if we saw 15% instead. Looking at the chart it seems there are two different regimes for high yield defaults. In the calm times, default rates are generally around 2-2.5%. But there have been three periods of much higher default rates – 1989-1993, 1998-2003, and 2008-2009. Each of these saw default rates rise several-fold over the calm time levels. Each default cycle saw a very significant excess of defaults, ranging from around 14% extra defaults in the 2008-2009 event to about 26% extra in the 1998-2003 event. As recently as last summer, the Wall Street consensus seemed to be that we were not in for cycle four in the near future, although my colleague Ara Lovitt pointed out at the time that some of the arguments that strategists were using to make that claim did not hold up well when one looked at the data.3

While some are still arguing that default rates will remain subdued for the next few years, we are not among them. It is our belief that we are probably entering into default cycle four, and investors should be prepared for defaults to rise, and not just in the energy and mining sectors being pummelled by falling commodity prices. The question is how bad will cycle four be?

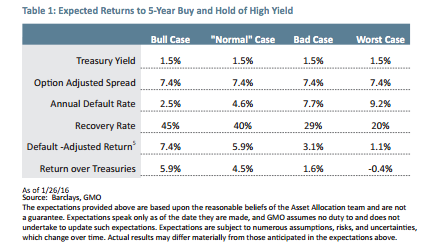

Unfortunately, we don’t know. The energy and mining sectors are clearly in for a very rough time of it, and the early defaults from this wave in 2015 saw some shockingly low recovery rates on the bonds – single-digit or zero recoveries in several cases against long-term average recoveries for senior unsecured debt of a little over 40%.4 How bad it will be for the rest of the high yield universe is hard to gauge. It is tempting to say that the answer depends on the economy – should we avoid recession, defaults will be low; in a deep recession, defaults would be much worse. But the pattern we’ve seen over the past 30 years suggests it isn’t that easy. Far and away the worst recession over the period was the Global Financial Crisis of 2008-2009. But it was the least bad default cycle, as unprecedently large fiscal and monetary stimulus combined with regulatory forebearance on the financial sector caused many borrowers pushed close to the brink to be able to recover without declaring bankruptcy. The worst default cycle, by contrast, was the 1998-2003 TMT cycle, and it included the mildest recession in U.S. history. In fact, given GDP revisions since then, the recession never even occurred according to the common recession definition of two quarters in a row of negative growth. These two events tell us a couple of things. First, default rates do not have to be particularly closely coupled to economic growth. And second, while the TMT cycle was the worst default cycle we have seen since the birth of the modern high yield market, it is almost certainly not a true “worst case scenario.” Since a worst case scenario is a very helpful thing to have in mind when making an investment case, we will have to make one up. The results are found in Table 1.

As we can see, at current yields, high yield is a real bargain if we actually experienced “calm time” defaults over the next five years, and is still quite cheap if we see default rates that track the long-term average.6 A repeat of the TMT cycle would see a buy and hold return of about 1.6% over treasuries, which seems at the very bottom end of acceptable for a risky asset of this nature. The worst case scenario shows a return about half a percent worse than that of treasuries, which would clearly be a grave disappointment. The magnitude of the losses in the worst case were not picked out of thin air, but rather correspond to the worst five-year average default rate during the U.S. Great Depression, according to Moody’s. The recovery rates were admittedly more of a guess, but seem to us to be reasonable in the context of a truly disastrous economic outcome.

Will high yield overshoot?

So the bad news is that high yield is not guaranteed to have a good outcome from here, but the likely results over the next five years range from just about acceptable to wonderful in anything but the most dire default scenario. So, why not be all-in now? If high yield seems to be cheap or at least okay under all but the worst circumstances, isn’t that a good deal better than anything else we have on offer? Yes and no. First, default losses are not the equivalent of an equity drawdown, but a permanent impairment of equity value. It certainly doesn’t say anything about how bad things might get in the interim. The equivalent would be to say that the permanent impairment of capital for European stocks from the Global Financial Crisis looks to have been around 8%.7 The peak to trough loss for European equities, by contrast, was approximately -59%.8 And second, given the illiquidity of high yield bonds and the particular dynamics of the asset class, there are pretty good reasons to believe that this is a market that has a hard time stopping at fair value on the downside.

Part of the problem is the nature of how high yield bonds come about. Today, the vast majority of the high yield bonds in existence were issued with ratings of BB or lower. But there is another way to create high yield bonds, which is to have investment grade bonds get downgraded to junk status. To some degree this happens throughout the cycle – in an average year about 5% of BBB bonds will get downgraded to junk. But during a default cycle, the downgrade frequencies can double or more. Given that the BBB cohort of U.S. corporate debt, at $2.1 trillion, is significantly larger than the entire $1.2 trillion U.S. high yield market, downgraded investment grade bonds can increase the size of the high yield market materially just at the time of the cycle where there is little appetite from investors to absorb more of them.

But perhaps more important is the interesting divide between the holders of high yield debt when it is issued and the potential buyers in the circumstance that those original holders want to sell. High yield debt is not homogenous, even when it is the debt of a single issuer. While this point has been raised countless times before, it’s worth going over again the implications of the idiosyncratic nature of individual bonds in the event of trouble. Under normal circumstances, borrowers come to the market at times when it is calm and investor sentiment toward the borrower is good. Buyers of the debt are thinking more in terms of the yield on offer and usually less about the individual features of the indenture they are buying. But even insofar as they do care about the details of the covenants, collateral, and position of the debt within the borrower’s capital structure, there is incentive for bond dealers to give investors some time to fully analyze the potential issue before they have to place bids on it. 9

This dynamic changes when the original holders are in a position to have to sell. Whether that is because a formerly investment grade bond is downgraded to junk or a mutual fund manager is facing client redemptions or an insurance company needs to reduce risk in its portfolio, the seller does not have the luxury of letting potential buyers analyze the bond for a week before they ask for bids. The potential buyers, however, still need time to analyze the bond. In fact, given that the issuer is more likely to be in danger of defaulting than was the case at issuance, the details of the issuer and the indenture probably matter more to them than the original par buyer. And given the nature of corporate capital structures, analyzing bonds is far more complicated than stocks. Kinder Morgan has only a single issue of stock. There may be 2.2 billion outstanding shares, but they are all exactly the same from a legal standpoint. The debt is another matter. As near as we can tell, Kinder Morgan has at least 55 different debt instruments outstanding across what seem to be 29 different entities and subsidiaries that warrant their own abbreviations in their 2014 10-K.10 So, even if a potential buyer already owns an issue of the company, he needs to do significant additional work to truly understand any other one that comes up for sale.11 The different issues may well have very different recovery values in the event that the company does default. As an example, at the time of the TXU default (which was quite well-telegraphed to the market), the trading price of its various bond issues ranged from 119 to 8.8. Knowing Kinder Morgan as a company is an essential first step to understanding what each of its debt issues are worth, but it is far from the only step. The potential buyers who are probably in the best position to do the analysis quickly are the big bond mutual fund firms who have a large team of credit analysts covering the bond market. But during a sell-off, their high yield funds are probably facing redemptions themselves, and so are not really in a position to be buyers. The distressed debt hedge funds and more opportunistic investors who are not large investors in high yield when spreads are tighter are unlikely to have done sufficient analysis ahead of time given that they have smaller teams and/or a wider array of securities to cover around the world. To protect themselves against the potential adverse selection of the seller knowing more about the bond than they do, they need to build a margin of safety into their bids for the bonds.

In the past, this is where the bond dealers might have stepped in. The original underwriters of the bond would likely have kept up with the issuer and, hence, knew the issue well. They could step in and buy the bond and warehouse it for a time while potential buyers did the work to understand how much they thought the bond was worth. The dealers did not do this as charity, of course, but given their knowledge of the issue and their relationships with the pool of potential buyers, they generally would have been able to buy the bond at a smaller price concession and make money on the transaction anyway. Given the regulatory changes that have forced the dealers to slash their bond inventories as well as their experienced fixed income traders, they can no longer provide this service to any meaningful extent. In extreme market moves, such as occurred in the fall of 2008, admittedly the dealers have always hesitated to put too much of their capital on the line, but they did step in on occasion in the past and will not for the foreseeable future.

A final driver of overshoot is the different cost of capital for the potential buyers of high yield when traditional holders are forced to sell. If you are a distressed debt hedge fund charging your clients 2 and 20, you are really only interested in buying bonds that have expected returns in the double digits, whereas normal high yield buyers are generally willing to accept lower returns of 2% to 3% above comparable treasuries after expected defaults. That is a pretty wide gap to have to jump over, and requires a pretty big price drop.

Conclusion

At current spreads, high yield seems to be no worse than fair value and probably better than that, even if we assume (as we do) that we are entering a fourth default cycle. In today’s environment, that makes it one of the best available risk assets for investors. But the nature of the high yield market suggests it is a good candidate for overshooting fair value to the downside whenever defaults begin to rise in earnest. Our response for BFAS at current levels is to continue to search for credit securities offering a superior combination of expected returns and downside protection while augmenting this at the margin with more index-like credit exposure. This has been a slow process, but we have been able to steadily add to our credit exposure over the last 12 months or so and we expect to continue to build our holdings over the coming months.

It would be lovely to claim we will be able to time the bottom for credit precisely. We will not, and unlike with equities, even if we did know the timing perfectly, getting material exposure to the asset class quickly would be extremely difficult. This leaves us with the hunch we are probably getting in a little early, the fear that we might not get all the exposure we would like before spreads move to less attractive levels, and the sure knowledge we won’t get the bragging rights of having called the turn. In other words, it seems to be an utterly classic value investing opportunity.

1 The option adjusted spread is a spread of a fixed income security or derivative over the equivalent risk-free rate accounting for the value of any embedded options in that security. The figure will vary depending on the model used to value the embedded options.

2 As of the middle of January 2016, emerging market equities look to be within a few points of fair value on our models and emerging market value stocks are probably a bit below fair value, but otherwise we have trouble finding any equity or bond markets close to their historical valuation norms.

3 Ara Lovitt, “What Do High-Yield Maturities Tell Us About Timing the Credit Cycle? Another Take on the Wall,” July, 2015. This white paper is available at www.gmo.com.

4 Source: Moody’s Analytics data from 1998-2015 for U.S. corporate high yield.

5 This return estimate makes the assumption that defaults happen on average halfway through the year, costing half of the year’s yield in addition to the losses in default. It also assumes that the index has exactly five years to maturity.

6 If a fair return for equities is around 3- 3.5% above treasury notes, high yield bonds need to return somewhat less as they are less risky than equities, although they have some equity-like characteristics and are far less liquid than treasury bonds. A number 2- 2.5% above treasuries probably qualifies as a fair return.

7 See July 2012 GMO Quarterly Letter, “When Bad Things Happen To Cheap Assets.”

8 MSCI Europe ex UK, 2007-2009 worst drawdown on monthly U.S. dollar returns.

9 This is not to say that underwriters never act to bury some information until after the fact. But the goal of the underwriting process is to get the bonds placed at an acceptable price, and if that requires giving potential buyers some time to analyze the issue, they will certainly do that.

10 Specifically, Kinder Morgan has 55 debt issues that are included in the Barclays U.S. Aggregate Bond Index. It may well have others that are not eligible, but I didn’t have the heart to ask someone to dig out a more exhaustive list.

11 As of January 2016, Kinder Morgan is rated Baa3, the lowest investment grade rating, by Moody’s Analytics, so it isn’t high yield today.

Disclaimer: The views expressed are the views of Ben Inker through the period ending February 2016, and are subject to change at any time based on market and other conditions. This is not an offer or solicitation for the purchase or sale of any security and should not be construed as such. References to specific securities and issuers are for illustrative purposes only and are not intended to be, and should not be interpreted as, recommendations to purchase or sell such securities.

Copyright © 2016 by GMO LLC. All rights reserved

*****

Part I: The Real American Exceptionalism Jeremy Grantham

Introduction

If you listen to most red-blooded Republican candidates for President, you will often hear lists of U.S. virtues that are claimed to be superior to all others. There is never any attempt to prove the assertions – they are articles of faith. And, as we saw in last quarter's letter, the claims are mostly inaccurate and by a wide margin. Indeed, in this one respect Mr. Trump is far more accurate when he suggests that the U.S. has fallen off the pace in recent decades and has done much better in the past and could perhaps do much better again.

But this quarter I would like to examine two areas where the U.S. really does have documentable advantages. They are both incredibly important, one especially for good times with thriving capitalism and the other as a protection against possible bad times in the future that I for one fear.

1. Animal spirits and venture capital

In a world in which most things continue to work well, or at least well enough, the U.S. has the advantage of simply being more entrepreneurial. More of us risk starting new enterprises than do others in developed countries. Keynes famously made the point that almost no one, looking at the 10% survival rate of new enterprises, would take the risk in cold blood.1 He argued that the recklessness brought by a surge of animal spirits was necessary to lead entrepreneurs to believe that they would be the exceptions. And Americans apparently have more animal spirits than most. In the U.S., much more than in Europe and elsewhere, it is also okay to have failed. Some visible scars are taken as proof that you have played the game hard. Our culture is more forgiving. You can even be associated with several bankruptcies and still be a strong-running candidate for President! How unlikely that would be anywhere else. And if three times more of us charge at the Internet, medical research, or social enterprises than in other countries, then we do not have to be better. The laws of averages will guarantee, given even average competence, that when the smoke of battle clears we will have more of the Amazons, Facebooks, and Coca-Colas, for that matter, than they do. And we might indeed be a little better. Over half of the world’s top 100 brands are American, even though we are only 20% of the world’s GDP, and that ratio has been looking strong in the last 20 years as new great brands appear. Seven of the strongest seventeen global brands2 have their U.S. founders still living, without including Apple, the number one brand, as a sad near miss. What a remarkable testimonial to the recent vigor of American entrepreneurial spirit this is. Last quarter I talked about the downside of overconfidence and accepting only good news. Well, this is the upside to what can often seem like excessive optimism: We undertake far more than our fair share of substantial start-ups and we dominate the formation of great new global brands.

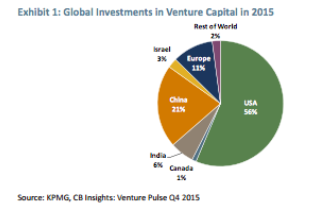

Not surprisingly, perhaps given our inclination for risk-taking, we have also ended up with by far the biggest and, I suspect, the best venture capital industry. In this we represent almost half the dollar value of all global venture capital invested in a year (see Exhibit 1). This industry in turn has the unfair advantage of feeding off the world’s great research universities. In this regard it is, like most areas of life these days, a winner-take-all environment. Among universities, Harvard and Stanford are not associated with twice the money raised for start-ups than the twentieth largest money-raiser, but 10 times more.3 Last quarter, I talked about the relatively average quality of the typical U.S. student. That fact does not take away from the nearly complete dominance by the U.S. of the top-rated academic universities globally. In the 3 rankings that I checked, the U.S. had 15 or 16 entries out of 20 in all 3 (the U.K. had 3).4

This is not meant to ignore the importance of governmental R&D, which has declined as a percentage of government spending over recent decades. Increases in R&D would feed into the strengths we already have in the three areas of natural risk-taking, venture capital dominance, and the great research universities. It would also come at a time when we are faced by greater non-military threats than ever before: climate change and the need for alternative energy technology.

Our strong position in new enterprise has, I think, important investment implications for today. I believe the returns to cash and bonds are certain: They are certain to be low or negative. Global equity markets in the developed world are overpriced, particularly in the U.S. In the developed world, real estate and even farms and forestry all yield 2% or so below their long-term averages. I believe that these miserable potential returns have been brought to us courtesy of the Greenspan-Bernanke-Yellen Fed regime and their belief in interfering in markets, manipulating if you will, and their moral hazard asymmetry. This is a long and old story and I will just resist going into it one more time.

In stark contrast to dismal returns in investable public markets is the continued high return on equity available to corporate investing, the mean-reverting series that refuses to mean revert, where competition no longer serves, apparently, to bring returns back to the old averages. We can argue about the reasons for this. I lean to the Andrew Smithers line that it is caused by the “stock option culture” in which stock is bought back – this last year a record $800 billion – and deals are made, also at record levels, rather than capacity expansion, which has run at mediocre levels. But whatever the reasons and despite a modest decline in margins in 2015, caused mainly by oil and mining wipeouts, abnormally high returns at the corporate level are a fact. This persistent discrepancy – that in theory is arbitrageable but in practice apparently is not – between low returns to private investors and high returns to corporate investments suggests an investment strategy: Get as close to corporate investing as you can. The closest is to start your own company. Failing that, the next nearest is early-stage venture capital where the investor gets some of the benefits, small or large depending on the circumstances, of the entrepreneurs. Another way of looking at this is that reduced capital spending by established public corporations leaves more opportunities for new start-ups (and for private companies).

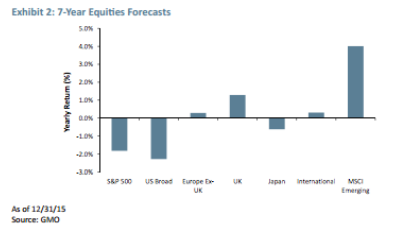

GMO’s 7-year forecasts, which are based on margins and P/Es returning to a longer-term average, suggest that returns on public investments will range from negative to about 3% (with the interesting and risky-looking exception of emerging market equities, which now offer a more normal 4% return as shown in Exhibit 2). Even if U.S. corporations did not regress in either margins or P/E, the current modest yield and modest growth would offer less than 4% a year on our forecasting methodology. In contrast, corporate return on equity, after adjustments for some wonky accounting that has gotten steadily more suspicious over the last 25 years, appears to be considerably higher than its old 7% real, perhaps as high as 8% to 10% real. You can see what a handsome gap there is. A gap that has existed now for almost 20 years, although on average smaller than it is currently. Its lengthy stay, in defiance of theory, owes a lot to the Fed and a lot to the new corporate fixation on short- and intermediate-term profits. While it lasts, diversified venture capital offers, I believe, the best investment opportunities. Adding to the case for venture capital is that over the long run it has had a higher return than have public equities, a rare case where theory coincides with reality, for venture capital is perceived as the higher risk asset and should in theory have a higher return.5 In the interest of full disclosure, the Grantham Foundation is aiming at over 30% in venture capital, putting its money where its mouth is (or, more accurately, where my pen is). At this point it is appropriate to point out the illiquidity and risk of venture capital. Why can’t we just have a free lunch? Investing in venture capital obviously requires experience, skill, and extreme diversification and should not be attempted at home.

Finally, on this issue, venture capital represents one of the best opportunities for “mission-driven” or “impact” investments. By investing in alternative energy projects and agricultural research and improvements the Grantham Foundation is offered at least the hope of handsome returns together with the certainty that we are helping our two most critical global needs. So, from these several perspectives it is good to be based in the U.S. and particularly in Boston, a city that, along with the San Francisco Bay area, best represents this greatest relative strength of the U.S. in global capitalism.

2. Fortress Canamerica

The problem of feeding 10 billion humans is likely, I believe, to create increasing problems. Soil erosion, desertification, and other land degradation deprive us of over 30 million acres a year. Urbanization costs us some more. It has been calculated that after over 12,000 years of farming, done sometimes very badly and sometimes merely suboptimally, 5 billion of our original 16 billion acres of useful arable land has become unusable. And now destabilized weather, especially extreme droughts and floods, cost us increasing percentages of our soil through erosion and increased crop losses, which have risen from a 5% average annual loss 30 years ago to 15% today6 in the developed world. This and other reasons have caused our net gains in productivity to drop from over 3% a year in the Green Revolution of the 1950s and 1960s to just over 1% now and the trend profile is for further declines in productivity gains.7

These difficulties, though, are very unevenly distributed. Africa and the Middle East drew the short straws. The Americas drew the long straws, and everyone else, as a broad generalization, is in the middle. As you know from my previous quarterlies, I am extremely worried about Africa, which is estimated to have all of the world’s future population growth, coupled with a long list of agricultural problems: the worst soils on average and the greatest soil degradation; the worst availability of surface water distribution; poor access to energy and fertilizer; the worst food distribution system, a terrible infrastructure, and, on average, the poorest governance. It seems likely to me that they will receive insufficient effective assistance to meet their challenges. Their neighboring Middle Eastern countries share many of the same problems. The odds favor the continued increase in these two areas in the number of failed states, a process that has been going on for the last several years. That in turn threatens, indeed almost guarantees, an increasing wave of immigrants or refugees into Europe that will inevitably stress some of the component countries into severe economic or political problems. Unless we are extremely lucky, these destabilizing forces – climate and food problems together with refugees and other immigrants – will unsettle global politics and create repeated crises, which will be made worse by terrorism. Not a pretty picture and one that increasingly concerns the minds of various military and intelligence groups including our own.

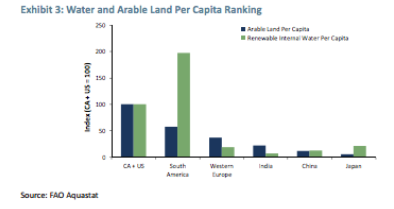

In this rather nightmarish potential it is clear who has the best hand to play: the U.S. and Canada (and, to a lesser degree, South America). The list of our advantages in Canamerica, as we could call it, is a very long one. First, we are uniquely defensible and difficult to attack. We are well-armed and well-organized. Less obviously, perhaps, we are more than self-sufficient in food production, energy, and mineable resources. Exhibit 3 shows how we rank in water and arable land per capita. We have six or seven times more of these critical resources per capita than China or India. We have two and a half times the available ratios for the rest of the world.8 To rub in our advantages in arable land, we are much over-represented in the highest-quality loess soils – those that come only from accumulations of wind-blown soils over millennia and are found in quantity only in California and the Midwest, Argentina, Eastern Europe, and Northern China. These soils are often tens of feet thick and so productive that you can get a reasonable harvest after your top soil has blown away, when less fortunate populations would starve. We have enough reserves of fossil fuels that if we put our best foot forward we can convert successfully to renewables. Even given the wasteful “big ag” we have today we are only deficient in phosphorus looking out beyond 50 years and we have sufficient reserves of fertilizers to buy us time to change our agriculture to more sustainable practices. (On phosphorus, we have to make sure that after the next decade or two we stay friendly with Morocco, which controls ±75% of the world’s high-grade phosphorus reserves, as regular readers know.) We have a sufficiency of basic metals and most of the more exotic ones. We could, if necessary, finesse those few we lack.

These are not small advantages. No other area of the world comes close to having our assets. I have extreme doubts that densely populated countries even in the developed world could feed themselves in a highly stressed global world. But even in such a world, Canamerica, almost uniquely, could probably sustain up to twice its current population – although strongly not advocated! This, together with the first point on animal spirits, is the true American advantage, not the ridiculous and provably wrong ones we hear on television. On most of those alleged virtues we are merely average among developed countries and on most of them we have been slipping. On some, like income inequality, health, and social cohesion, we are at or close to the bottom of the list.9 But on the two aspects featured here, both extremely important and one certainly the most important factor of all, we are truly fortunate and, yes, exceptional.

1 Modern data shows just over 70% failure rate at 10 years. By deduction, that’s about 90% in 25 years.

2 Interbrand, “The Best 100 Brands,” 2015.

3 PitchBook, “Universities Report,” 2015-2016 edition.

4 15/20 “Times Higher Education World University Rankings” 2014-2015; 16/20 U.S. World and News Report, “Best Global Universities”; 16/20 “2015 Academic Ranking of World Universities,” Shanghai University

5 Cambridge Associates LLC US Venture Capital Benchmark®

6 Navin Remankutty, et al., Nature, January 2016.

7 Grassini, et al., Nature Communications, December 17, 2013.

8 David Montgomery, University of Washington, 2012.

9 Richard G. Wilkinson and Kate Pickett, The Spirit Level: Why More Equal Societies Almost Always Do Better, Allen Lane, 2009

Disclaimer: The views expressed are the views of Jeremy Grantham through the period ending February 2016, and are subject to change at any time based on market and other conditions. This is not an offer or solicitation for the purchase or sale of any security and should not be construed as such. References to specific securities and issuers are for illustrative purposes only and are not intended to be, and should not be interpreted as, recommendations to purchase or sell such securities.

Copyright © 2016 by GMO LLC. All rights reserved.

Part II: 2015 and 2016, U.S. Equity Bubble Update, and Yet More on Oil

Jeremy Grantham

Summary

■ The positive effects of low resource prices are underestimated. The U.S. and global economies are likely to do significantly better this year than recent opinions predict. The U.S. has plenty of spare capacity to grow above its longer-term limits. The biggest risk would be China’s GDP becoming much more disappointing.

■ The U.S. and global markets do not look like they are in bubble territory. They can always suffer a regular bear market (and are almost in one now). But I still believe we will have to wait longer for the BIG ONE and that global equity markets will regroup once more.

■ Currently ultra-low resource prices are not sustainable, particularly those of grains and oil. Oil producers need $65/barrel and rising to finance new oil exploration. Resource prices will inevitably rise and as they do they will reduce once again the growth rates of the global economy.

A quick look at 2015 and 2016

2015

Looking back to last year we could simplify it by saying that the big positive was, as usual, support from the Fed and its allies, as they continued to maintain lower than market rates. You know my view: These lower rates have surprisingly little effect on the economy but a big effect on pushing up asset prices. Historically – well for 25 years anyway – the lack of reasonable values has often not impeded the Fed’s ability to push equity prices higher. Indeed, by any traditional measure we have spent over 80% of the last 25 years overpriced. The big negative in 2015, of course, was China slowing down, especially in areas requiring raw materials. This helped to broadly lower global GDP growth. Loosely speaking, the closer investments were to China – say, miners, countries supplying raw materials, and emerging markets with heavy Chinese trade – then the relatively worse they did. And the closer to the Fed, as the U.S. is, the less badly they did.

The global bear market bias of 2015 was also helped along everywhere by the plunging oil price, which caused layoffs, reductions in capital spending, and, probably more importantly for equities, increased global uncertainties both at the company financial level and the country political level.

Right behind that as a negative, particularly in the U.S., was a decline in profit margins. Finally! But the drop was from levels so far above the old trend that even after recent declines they remain handsome.

Looking at the U.S. equity market I think we might agree on how powerful the Fed is in the market equation. It approximately offset these three very large negatives: China, oil, and declining margins, which together caused disappointing global growth. But in addition, it had to neutralize the justifiable nervousness caused by increased terrorism, immigrant problems, Russia’s sharp elbows, and an apparently disheveled Europe. Not bad!

2016

Looking to 2016, we can agree that uncertainties are above average. But I think the global economy and the U.S. in particular will do better than the bears believe it will because they appear to underestimate the slow-burning but huge positive of much-reduced resource prices in the U.S. and the availability of capacity both in labor and machinery. So even though I believe our trend line growth capability is only 1.5%, our spare capacity and lower input prices make 2.5% quite attainable for this year. And growth at this level would make a major market break unlikely. As discussed elsewhere, this situation feels at worst like an ordinary bear market lasting a few months and not like a major collapse. That, I think, will come later after the final ingredients of a major bubble fall into place.

As always, though, prudent investors should ignore historical niceties like these and invest according to GMO’s rather depressing 7-year forecast. The U.S. equity market, although not in bubble territory, is very overpriced (+50% to 60%) and the outlook for fixed income is dismal. At current asset prices no pension fund requirements can be met. Thus, we should welcome a major market break that will leave us with more reasonable investment growth potential for the longer term, but I suspect that we will have to wait patiently for such a major decline. The ability of the market to hurt eager bears some more is probably not exhausted. I still believe that, with the help of the Fed and its allies, the U.S. market will rally once again to become a fully-fledged bubble before it breaks. That is, after all, the logical outcome of a Fed policy that stimulates and overestimates some more until, finally, some strut in the complicated economic structure snaps. Good luck in 2016.

U.S. equity bubble update

On the evaluation front, the market is not quite expensive enough to deserve the bubble title. We at GMO have defined a bubble as a 2-standard-deviation event (2-sigma). We believe that all great investment bubbles reached that level and market events that fell short of 2-sigma did not feel like the real thing. (In our view, 2008 was preceded by an unprecedented U.S. housing bubble – a 3-sigma event.)

Today a 2-sigma U.S. equity market would be at or around 2300 on the S&P, requiring a rally of over 20%; even from the previous record daily high it would have required an 8% rally. The impressive bubble peaks of 1929 and 2008 also featured broad international overpricing of equities, measured at over 1-sigma, and this, too, was completely lacking this time. Emerging market equities were just ordinarily overpriced last year and full of investor concerns totally unlike normal bubble conditions. Europe and other developed markets were more overpriced but nowhere near bubble levels, and were also characterized by extreme nervousness.

On the more touchy-feely level of psychological and technical measures, the U.S. market came closer to bubble status but, still, I think, no cigar. I had pointed out two years ago1 that nearly all major bubbles are immediately preceded by a period when the safer blue chips outperform the riskier, higher-beta stocks on the upside. At other times this would be considered very unusual. Two years ago there was not a hint of that, but last year was a classically narrow market – i.e., led by a handful of the very largest and, on average, higher-quality companies. So the bears can claim this one, although I think with an asterisk because the market was not really going up last year and outperformance of bigger stocks in a flat market is not particularly remarkable. Also mitigating the bear argument is that this market effect was not caused by defensive buying of blue chips but, I would say, offensive buying into the spectacularly superior earnings of this small group. So, not convincing. I had also written that I did not see much chance that this market would end before records would be set for corporate deals done, encouraged by the extremely low rates and reluctance to invest in new plants and equipment. This test, I must admit, was passed with flying colors, for all deal records were broken in the second half of last year. Much more convincing.

A third less elegant but historically effective test further improves the odds of a bear market this year: the infamous January rule. Applied GMO-style, it goes that the first five trading days predict the balance of the year, especially if the average number is negative. (As does the whole month with about the same – and quite significant – statistical weight.) When the two signals oppose each other, on the other hand, we have had very normal years. Needless to say, the first five days and January were both record-ugly this year. Since 1925, a down five-day and down January have more than doubled the probability of a down market for the remaining 11 months.

So I must admit to feeling nervous for this year’s equity outlook in the U.S. But I am not entirely convinced. Sure, we can have a regular bear market. That is always the case. But the BIG ONE? I doubt it. And here is my admittedly reduced case.

The most important missing ingredient is a fully-fledged blow-off. This should come complete with crazy speculative anecdotes for your grandchildren, massive enthusiasm from individual investors, an overwrought, overcapacity economy, and, at minimum, a 2-sigma S&P 500 at 2300. Lacking all of this, I still believe it is “likely” that we will reach Election Day more or less intact. I will, though, admit to my definition of “likely” being beaten down by the negative factors listed earlier to something just over 50%. The wild card, as usual these days, is China. The market is discounting lower growth. (I believe 4% a year for the next 10 years would be a reasonable target.) But a deep entry into negative GDP numbers might ruin my relatively positive case for global growth.

To rub in how ordinary our present market negatives are compared to the impending doom bubble of 2007 when a crash seemed inevitable – like “watching a slow motion train wreck”2 – let’s compare today with 2007.

Back then the banks looked very vulnerable. Indeed, I predicted in July 2007, “at least one major bank… will fail.” This time oil debt may hurt, but our moderately strengthened banks will surely withstand this much smaller hit easily. In 2007, resource prices, historically a terrible drag on economies, were at cosmic highs – oil alone was over $150/barrel. Today they are at cosmic and unsustainable lows. So a major, major negative is this time a major positive. The U.S. housing market back then was at a 3-sigma high (never before approached) and represented a potential and realized $6 trillion writedown of perceived wealth. This time the U.S. housing market is merely moderately overpriced. Last time the economy was cranking out 1.25 million extra houses and the whole economy was running flat out. This time we are building at least 300,000 houses below normal levels and there is spare capacity in the broad economy. Clearly, this current situation has no material similarity to that which impressed us as so irresistibly negative in 2007. In short, the economic outlook for the immediate future is less bad than recent commentaries would have you believe. Especially in the U.S.

Yet more on oil

So, this is the situation: The world’s most important resource, oil, which we need for practically everything but especially to drive our cars, is getting really cheap. And this is helping to drag other commodities down with it. Everything is getting cheap. It is like a tax cut for individuals that is being financed by the profits of oil companies and Saudi Arabia. Now, what’s not to like about that? Yet this is a big part of what is spreading terror in the markets. Why?

I have described before the situation that although in the long run there is an apparent balance between winners and losers, the problem is that oil companies and their suppliers take their hits up front as they reduce their exploration and development efforts projecting deep into the future. Oil-dominated countries do the same, in addition to cutting their national budgets and their foreign buying. Under this shock, economic expectations can take a hit.

The shock, I suppose, is how completely Saudi Arabia and OPEC were willing to give up any and all attempts to control price. Through 90% of oil history, if oil producers wanted to outproduce demand they could have. And it would always have buried oil prices. But mostly they restrained their competitive market share instincts in the interest of a more stable price. And very sensibly so. To summarize my previous case,3 I consider that Saudi Arabia, if it has been driven by commercial as opposed to political reasons, has made perhaps the biggest economic error in the history of oil. If their main motive is political, on the other hand, it better be an extremely important one for they themselves are quite likely to pay a very high political as well as financial price. An oil price change of this magnitude and speed is very destabilizing to economies, politics, and social cohesion. It makes for dangerous times and the market does not like it. The psychological response is understandable.

But excluding some major political upheaval, what are the likely economic consequences from here? The largest hits from the major oil company responses are behind us, although at $30/barrel (and maybe less) there will be some further retrenchment. And now comes the matching response from us, the consumers. Everything we buy has cheaper input costs. The major item of gasoline purchases is a steady jolt of encouragement. Heating bills are also much lower. Could there be a better financial input than this to the group that has been hurting for 30 years – the median wage earner? Not easily. Some of us argued that the impact of high resource prices in 2008 had an underappreciated major negative impact on the economy, and there certainly is a strong statistical relationship between previous upward jots in oil prices and ensuing recessions. (Actually, the number is 100%. Every major previous increase in the price of oil was followed by an economic setback. And why would this not be the case?) We argued that mainstream economists were so obsessed with bank and credit problems that they had no time to worry about resource prices. Typically they almost never do. Market opinion now, though, impressed with the early negatives that it should have expected4 and because the offsetting stimulus effect is delayed and weakened initially by some understandable increases in savings, is doing the opposite. It is underrating what will very likely become an important economic tailwind for the next several quarters. Reflecting current opinion (January 25), Luke Kawa, a writer for Bloomberg reviewing the oil situation claims, “One of the biggest surprises in economics has been how the world responded to a period of lower energy prices.” Well, the economic world is easily surprised.

A lot of people who worry about resources had felt that several years of much higher resource prices (from 2006 to 2014) were acting to weaken our global economy, slowly but surely, and I was one of them. I feel that this period now is a reprieve, if only temporary, from that pressure. It gives an opportunity for the global economy to regroup and start to grow a bit faster again, at least for a while.

The U.S. economy in particular, with its available labor, tucked away in the current ultra-low labor participation rate, and a moderately low industrial capacity ratio (76.5% – 3.5 points below its 1972- 2014 average), appears to be well-positioned to benefit. And, we are still an important wheel in the global machinery.

1 “Looking for Bubbles,” 1Q 2014 GMO Quarterly Letter.

2 See our Quarterly Letters during 2007.

3 See “Why Were We So Surprised? The Oil Glut, Saudi Decisions, and the Uniqueness of U.S. Fracking,” 4Q 2014 GMO Quarterly Letter.

4 For example, see the section under the subheading “Probability of a Net Drag on GDP” from the 4Q 2014 GMO Quarterly Letter.

Disclaimer: The views expressed are the views of Jeremy Grantham through the period ending February 2016, and are subject to change at any time based on market and other conditions. This is not an offer or solicitation for the purchase or sale of any security and should not be construed as such. References to specific securities and issuers are for illustrative purposes only and are not intended to be, and should not be interpreted as, recommendations to purchase or sell such securities.

Copyright © 2016 by GMO LLC. All rights reserved.

© GMO