Executive Summary

- Slowing growth and swelling corporate debt are expected to result in challenges in the coming quarters.

- A strong dollar is creating fears of deflation.

- Smaller companies may be well positioned to side step these headwinds.

Demographics, debt, and the fear of deflation are creating challenges for the economy and investors alike. However, we expect the impact of these headwinds will vary across different areas of the market with companies most insulated from these factors likely to outperform.

First, a closer look at how the “3 Ds” are making their presence felt.

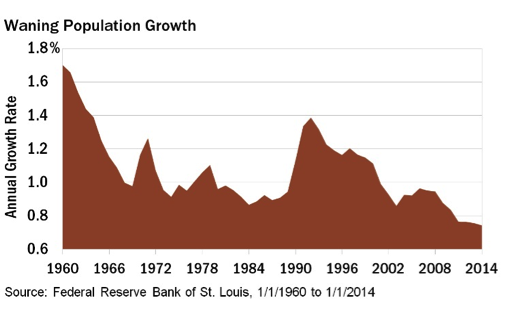

Demographics. Expansion of U.S. Gross Domestic Product (GDP) has been slower during the current recovery than in the past, and has softened in recent quarters. Increases in productivity and the number of people joining the workforce could produce a needed boost, but secular trends aren’t promising. After a near decade-long rise, worker output gains have been flattening, as shown. The population growth rate has also been on a steady decline domestically. With fewer workers entering the workforce, the addition of incremental output from new employees is limited.

Debt. Inexpensive credit has allowed CEOs to boost results without having to generate organic sales growth. For example, many companies have taken on debt to fund share buybacks. By doing so, even businesses with flat sales can show improvements by reducing the number of shares that have a claim on each dollar of revenue. While buying back equity can be shareholder friendly, we believe it should be funded by free cash flow and done only when the rate of return is higher than can be achieved by alternative capital expenditures.

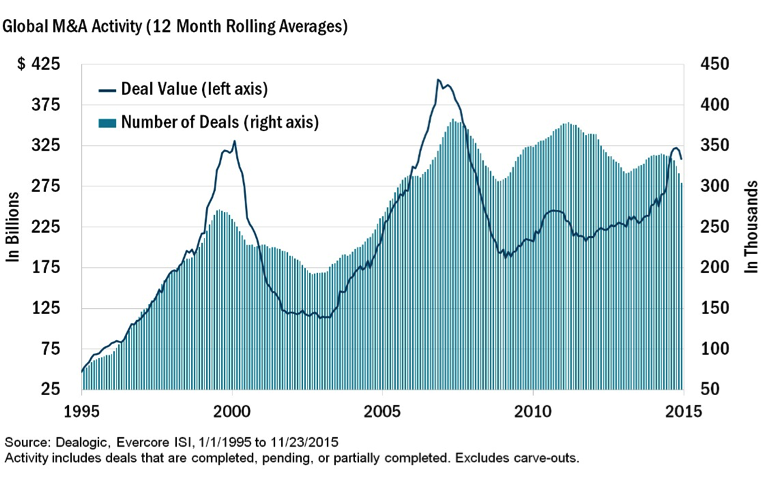

Friendly lending terms have also led to an explosion in mergers and acquisitions (M&A), as shown. Many of these deals provided a fleeting boost to earnings and were feasible due only to artificially low interest rates. With recent tightening in the credit markets and signs that investors may be focusing on company debt levels, this distorting force may be winding down.

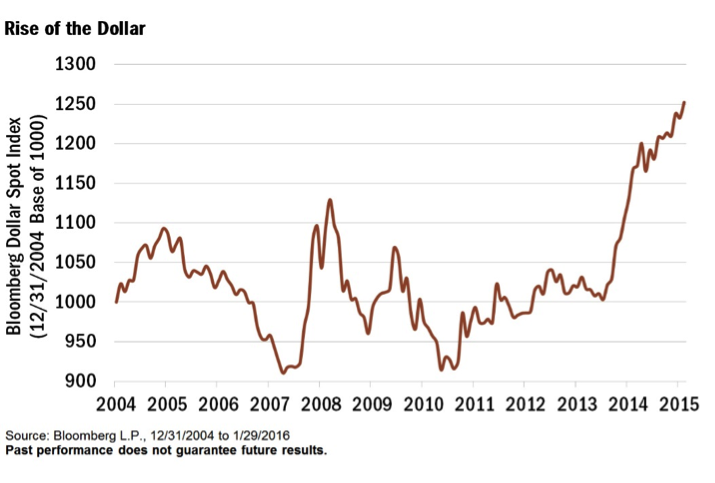

Deflation. Global central banks have been slashing rates in an effort to devalue local currencies and make products cheaper on the world stage. The moves have resulted in a strengthening of the U.S. dollar, as shown, and a flood of inexpensive foreign goods that has reduced pricing power for large, multinational businesses. With no end in sight to these efforts, a continued robust dollar will remain a challenge for corporations in the quarters ahead.

Where is the opportunity? While the challenges outlined could continue to weigh on the markets for the coming year, we believe they also present an opportunity for smaller companies.

Here is why:

The law of small numbers. Slower growth can be an outsized problem for large companies that need significant sales increases to drive improved earnings. For small companies, even minor movements in economic activity can translate into large upward changes in the rate of sales.

Follow the debt. While many companies have binged on debt during the current low rate period, the use of borrowing has been more pronounced among larger firms. Over the past five years, the long term debt-to-capital ratio of companies in the Russell 1000® Index has increased 34%. By comparison, smaller companies in the Russell 2000® Index have reduced their debt levels by 42%. The upshot is that as credit markets tighten, large companies that used leverage to boost results will be challenged.

Home field advantage. Large companies, as represented by the S&P 500, relied on foreign markets for nearly half of all sales in 2014. In contrast, companies in the Russell 2000® Index receive a much smaller portion of revenue from abroad. Given the relatively low level of income smaller companies generate outside of U.S. borders, we believe the impact of a stronger dollar will be modest and give them a competitive advantage over stocks of larger counterparts.

Summary

After seven years of a bull market defined by cheap debt and modest growth, we believe challenges are emerging. The effects of these will vary at the company level and, we believe, will be felt most by larger businesses. Small companies may have a relative advantage in the coming quarters and we are convinced a focus on balance sheets, valuations and business strategy is key to identifying companies in the small-cap space with the greatest chance for success.

Disclosure:

Past performance does not guarantee future results.

The statements and opinions expressed in this article are those of the presenter(s). Any discussion of investments and investment strategies represents the presenter’s views as of the date created and are subject to change without notice. The opinions expressed are for general information only and are not intended to provide specific advice or recommendations for any individual. Any forecasts may not prove to be true.

Investing involves risk, including the potential loss of principal. There is no guarantee that a particular investment strategy will be successful.

Heartland Advisors, Inc. considers large-cap companies to be larger than $15 billion in market cap, mid-cap companies to be between $2 billion and $15 billion, small-cap companies to be between $300 million and $2 billion, and micro-cap companies to be less than $300 million. The above breakdown does not include short-term investments.

Definitions: Free Cash Flow: is the amount of cash a company has after expenses, debt service, capital expenditures, and dividends. The higher the free cash flow, the stronger the company’s balance sheet. Gross Domestic Product (GDP): is the monetary value of all the finished goods and services produced within a country’s borders in a specific time period, though GDP is usually calculated on an annual basis. Long-Term Debt/Capitalization Ratio: represents the portfolio’s long-term debt as a proportion of the capital available in the form of long-term debt, preferred stock and common stockholder’s equity. Bloomberg Dollar Spot Index: tracks the performance of a basket of 10 leading global currencies versus the U.S. Dollar. Each currency in the basket and their weight is determined annually based on their share of international trade and foreign exchange liquidity. The index rebalances annually to capture annual trading flows versus the U.S. dollar as reported by the Federal Reserve and the triennial survey of most liquid currencies from the Bank of International Settlements. Each currency in the basket and their weight is determined annually based on their share of international trade and FX liquidity. The index data starts from Dec 31, 2004 with a base level of 1000. Russell 1000® Index: measures the performance of the large-cap segment of the U.S. equity universe. It is a subset of the Russell 3000® Index and includes approximately 1000 of the largest securities based on a combination of their market cap and current index membership. The Russell 1000® represents approximately 92% of the U.S. market. Russell 2000® Index: includes the 2000 firms from the Russell 3000® Index with the smallest market capitalizations. Russell Investment Group is the source and owner of the trademarks, service marks and copyrights related to the Russell Indexes. Russell® is a trademark of the Frank Russell Investment Group. S&P 500 Index: is an index of 500 U.S. stocks chosen for market size, liquidity and industry group representation and is a widely used U.S. equity benchmark. All indices are unmanaged. It is not possible to invest directly in an index.

©2016 Heartland Advisors heartlandadvisors.com

2016058