Global financial markets were unexpectedly volatile in January and there have been few signs of calm in February. Some of the worries are real; others imagined or overdone. It’s difficult for investors to slice through the noise. There is genuine concern that market fear could become self-fulfilling, and while the expectation is that the U.S. economy will muddle through and avoid a recession this year, the risks are tilted to the downside and policy options to counter a downturn are limited.

Recessions are defined as a broad-based decline in economic activity, usually visible in GDP, employment, personal income, real business sales, and industrial production. All of these have remained positive in the latest readings. The exception has been industrial production, which peaked in December 2014 and has reflected the contraction in energy exploration and warm temperatures in November and December. Still, taken together, the data do not suggest that we are in a recession.

Of the leading indicators of recession, it’s a mixed bag. The yield curve, the single best predictor of recessions, is still positively sloped (although less steep more recently). Jobless claims are trending low, and other labor market gauges do not reflect any broad-based increase in job destruction. The stock market is down, to be sure, but as Paul Samuelson noted many years ago, the stock market has predicted nine of the last five recessions (that is, it’s not foolproof). This week, we’ll get updates on two recession gauges. The Chicago Fed National Activity Index, a composite of 85 economic indicators (released Monday), is expected to remain consistent with growth slightly below trend in the near term, but still not close to a recession. On Tuesday, the Conference Board releases its monthly survey results on consumer confidence. The year-over-year change in evaluations of current conditions has been a moderately successful gauge of an impending downturn (while the y/y change was still positive in January, it has been falling sharply).

There is an important psychological aspect to recessions. Fear of a downturn can become self-fulfilling if consumers stop spending and if businesses curtail capital expenditures. Businesses do have to act on expectations. Firms are not going to expand if they don’t expect the demand for their goods or services to increase. Shipments of nondefense capital goods declined in 2015, and orders fell even more sharply. That’s not a good sign, but it’s unclear whether the weakness reflects a short-term correction or a longer-lasting slowdown. The capital goods story has been inconsistent with the job market outlook. Announcements of corporate layoff intentions (not the same as actual layoffs) did pick up in January, but the trend (while a bit higher) remains very low by historical standards.

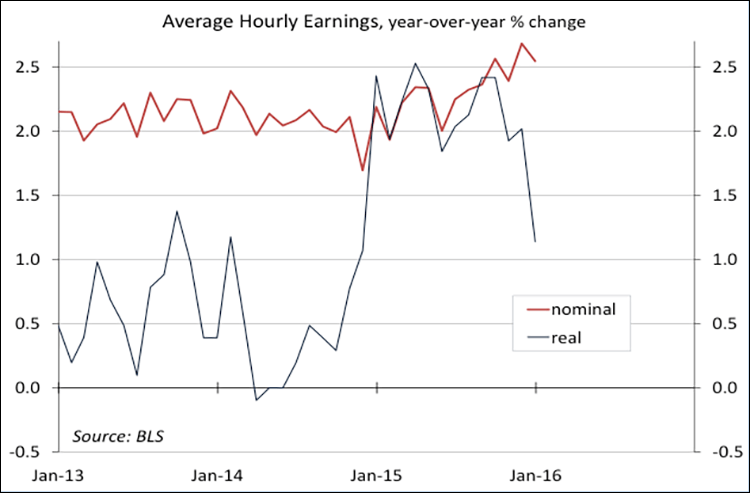

If every consumer decided to save an extra 5% of his or her income, we would have a depression. By saving more, households would be spending less, and that spending is someone else’s income. Fortunately, consumers seem to be ready and willing to spend. The drop in gasoline prices has added to consumer purchasing power, but that impact is going to fade over time (as gasoline prices won’t fall forever).

As part of recent bank stress tests, the Fed posed scenarios with negative interest rates – a remote possibility, not an expectation. If the economy were to weaken substantially, the Fed would be less inclined to pursue another round of asset purchases (QE4) and more likely to opt for negative interest rates. Currently, about a quarter of the world’s central banks have some form of negative interest rates. There are legitimate questions about whether negative interest rates would be legal in the U.S. and what effects they would have on the economy and the banking industry. However, as with concerns about a possible recession, market fear has outpaced reality by a wide margin. Still, while fear seems to be overdone and the economy is still expected to grow at a moderate pace this year, there are limited policy options available if the economy were to fall into a recession. That’s something to worry about.