KEY TAKEAWAYS

· As noted in our Outlook 2016, we expect the dollar to stabilize after its large increase between mid-2014 and mid-2015.

· The Fed’s QE programs and global monetary policies have impacted the value of the dollar over time.

· Should the dollar stabilize at today’s levels, it could turn into a tailwind for U.S. exports, commodity prices, and corporate revenue and earnings.

Since the middle of 2014—as markets prepared for the start of Federal Reserve (Fed) interest rate hikes and more easing from the European Central Bank (ECB) and the Bank of Japan (BOJ)—the U.S. dollar has been on a near historic run higher versus the currencies of major U.S. trading partners. In fact, the 20% gain in the dollar between mid-2014 and mid-2015 matched its largest percentage gain over any 12-month period since the dollar went off the gold standard in the early 1970s. As we noted in our Outlook 2016: Embrace the Routine, we expect the dollar may begin to stabilize as central bank policies and their outcomes become clearer. A stabilizing dollar should help to boost exports and remove a key headwind for manufacturing and profits of U.S. corporations.

Indeed, central banks, corporations, and commodity traders have frequently cited the strong dollar over the past 18 months or so as the key to (or cause of) low inflation, falling oil prices, weak export growth, slowing overseas sales (for U.S. corporations), and lackluster earnings. But now that headwind is abating, and may turn into a tailwind by the end of 2016.

Over the past several weeks, the dollar has moved lower as financial markets reconsidered the path of Fed policy over the coming years. At the start of 2016, the federal funds futures market was pricing in two more 25 basis point (0.25%) rate hikes after the Fed’s 25 basis point hike on December 16, 2015, versus December 2015 guidance from the Fed that it planned four more 25 basis point hikes in 2016. In late February 2016, the fed funds futures market doesn’t see a rate hike until the end of 2017. The Fed’s guidance is only updated four times a year, and the Fed will not provide a new set of forecasts until the March 15–16 Federal Open Market Committee (FOMC) meeting. Heading into 2016, we were forecasting that the Fed would raise rates three times (or by 75 basis points) this year.

KEY DRIVERS OF THE DOLLAR

The last time we dedicated an entire Weekly Economic Commentary to the dollar was in mid-2014, amid widespread concern in some circles (believe it or not) of a collapse in the dollar related to a 2010 law passed by Congress that required foreign banks to report holdings of U.S. dollars by U.S. citizens to the IRS. Those fears of “collapse” never materialized, and instead, fundamental factors took over and drove the dollar higher. But what are those “fundamentals”?

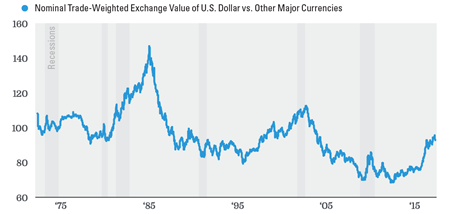

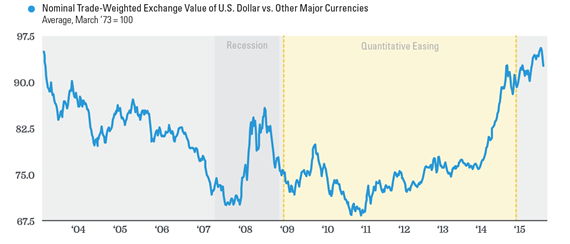

Aside from two periods in the early 1980s and late 1990s, the U.S. dollar has been declining since it went off the gold standard in the early 1970s [Figure 1]. The value of the dollar is set in the open market, although the Fed, Congress, and the President can have an impact. Of the three, the Fed probably has the most direct impact on the value of the dollar, as it sets short-term interest rates, which often have a big influence on the value of a nation’s currency. The Fed’s quantitative easing (QE) program, which ended in late 2014, increased the number of dollars in the global economy, and the law of supply and demand suggests that the greater the supply of an item, the lower the price. Thus, at the margin, QE likely put downward pressure on the dollar, all else equal [Figure 2].

Figure 1, With Few Exceptions, the U.S. Dollar Was Declining in Value Since the 1970s, Until Its 20% Gain Between Mid-2014 and Mid-2015

Source: LPL Research, Federal Reserve Board, Haver Analytics 02/22/16

The performance data presented represents past performance and is no guarantee of future results.

Figure 2, The Fed’s QE Programs Likely Put Downward Pressure on the Dollar

Source: LPL Research, Federal Reserve Board, Haver Analytics 02/22/16

The performance data presented represents past performance and is no guarantee of future results.

The value of the dollar must be quoted relative to something else, usually currency (or a basket of currency) from other countries. Therefore, the monetary policy of other nations also influences the value of the dollar in world markets. After all major central banks eased policy in response to the Great Recession and its aftermath, global central bank policies began to diverge in 2011 and 2012, with some central banks tightening policy, and others—notably the ECB and BOJ—beginning or ramping up QE programs of their own, just as the Fed was ending its foray into QE.

FOREIGN HOLDINGS

Despite the big run-up in the dollar in recent years, some market participants continue to fear an imminent collapse in the dollar, and the recent devaluation of the Chinese yuan reignited some of these fears. The concern is that countries with large holdings of Treasuries (and dollars) like China, Japan, and, to a lesser extent, Russia, will suddenly sell all of these holdings in the open market all at once, for either political reasons (disagreements with the U.S.) or economic reasons (the need to fund their own budgets or a loss of confidence in the U.S. economy, the Fed, Congress etc.).

Our view remains that a major shift in China’s or Japan’s (or even Russia’s) holdings of dollars and Treasuries is unlikely anytime soon given the tight trade linkages between the countries. China and Russia depend on U.S. goods and services to help advance their own economies, making it difficult for them to operate their economies efficiently without dollar holdings to fund purchases of goods and services. Over time (years and decades, not days and weeks), economies outside the U.S. are likely to continue to move away from the dollar and Treasuries—a trend that has already been in place for some time—but a move out of dollar holdings all at once would not be in the best economic interest of the selling country.

LONGER-TERM FACTORS INFLUENCING THE DOLLAR

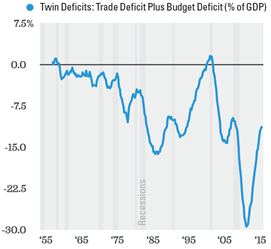

Trade policy, broad economic policy, and even foreign policy—set by Congress and/or the President—can also have an impact on the value of the dollar. Our “twin deficits,” trade and budget [Figure 3], have put downward pressure on the dollar over the past several decades; but since the end of the Great Recession, both the budget and trade deficit narrowed, which, all else equal, helped to boost the value of the dollar. Longer term, the budget deficit is likely to widen again, absent major reform to programs like Medicare, Medicaid, and Social Security, which should put downward pressure on the dollar.

Figure 3, The Trade and Budget Deficits, Our “Twin Deficits,” Have Also Put Downward Pressure on the Dollar Over Past Decades

Source: LPL Research, Haver Analytics 02/22/16

The performance data presented represents past performance and is no guarantee of future results.

The U.S. is the world’s largest economy, and as a result, most global trade is denominated in dollars; in turn, this makes the U.S. dollar the world’s “reserve currency.” Central banks and governments of most nations outside the United States hold reserves in dollars, although the rise of China’s economy and the sheer size of the Eurozone’s economy has eroded the dollar’s “reserve currency” status in recent years. Still, the dollar is still viewed as a “safe haven” currency, as are U.S. Treasury notes and bonds, which, of course, are denominated in dollars. In times of global economic and political uncertainty, the dollar typically rises in value, as investors must use dollars to purchase Treasuries, and those commodities viewed as traditional safe havens.1

Although our “twin deficits” and the Fed’s actions to stimulate the economy have put downward pressure on the dollar over time, the dollar’s status as the world’s reserve currency, and the position of the U.S. as the world’s largest economy and largest exporter, with its diversified and dynamic economy and labor force, suggest that any sudden, sharp movements in the value of the dollar either up or down are unlikely. On balance, the dollar is impacted by many factors in the short, medium, and long term. Interest rate differentials; monetary, fiscal, and regulatory policy divergences; movements in budget and trade deficits; changes in economic growth prospects; and even inflation and inflation expectations all influence the value of the dollar.

HEADWIND ABATING

Since mid-2014, just as many market participants were gearing up for a collapse in the dollar, a stronger dollar emerged. This has been a headwind for U.S. exports, commodity prices, and corporate revenue and earnings, and played a large role in Fed policy via the tighter monetary conditions caused by the stronger dollar. That headwind, which was running between 12– 20% during 2015 [Figure 4], has subsided substantially: In the first seven weeks of 2016, the dollar is up just 3% from the first quarter of 2015.

Figure 4, The Dollar Headwind, Impacting U.S. Exports, Commodity Prices, and Corporate Revenue/Earnings, Has Abated

|

Q1 2015 |

Q2 2015 |

Q3 2015 |

Q4 2015 |

Q1 2016 |

||

|

Dollar Headwind* |

18% |

20% |

17% |

12% |

3% |

Source: LPL Research, Bloomberg 02/22/16

*Year-over-year % change in the U.S. dollar versus the currencies of the Eurozone, Japan, the U.K., Canada, Sweden, and Switzerland.

The performance data presented represents past performance and is no guarantee of future results.

If the dollar stabilizes at current levels—which is consistent with our view—by the end of 2016, the dollar headwind would disappear altogether, and could turn into a small tailwind for U.S. exports, commodity prices, and corporate revenue and earnings. In the longer term, however, we continue to believe the dollar will slowly depreciate over time—continuing the trend that has been in place since the early 1970s, but at a pace that will not undermine the nation’s health or its role as a global economic power.

IMPORTANT DISCLOSURES

The opinions voiced in this material are for general information only and are not intended to provide or be construed as providing specific investment advice or recommendations for your clients. Any economic forecasts set forth in the presentation may not develop as predicted and there can be no guarantee that strategies promoted will be successful.

Investing in stock includes numerous specific risks including: the fluctuation of dividend, loss of principal and potential illiquidity of the investment in a falling market.

Investing in foreign and emerging markets securities involves special additional risks. These risks include, but are not limited to, currency risk, geopolitical risk, and risk associated with varying accounting standards. Investing in emerging markets may accentuate these risks.

The fast price swings in commodities and currencies will result in significant volatility in an investor’s holdings.

DEFINITIONS

Quantitative easing (QE) refers to the Federal Reserve’s (Fed) current and/or past programs whereby the Fed purchases a set amount of Treasury and/or mortgage-backed securities each month from banks. This inserts more money in the economy (known as easing), which is intended to encourage economic growth.

1 U.S. Treasury notes and bonds may be considered “safe haven” investments but do carry some degree of risk, including interest rate, credit, and market risk. They are guaranteed by the U.S. government as to the timely payment of principal and interest, and, if held to maturity, offer a fixed rate of return and fixed principal value.