Our quantitative tools have delivered an emphatic bear warning, and we are subjectively convinced the message is correct. But it’s precisely these times when our conviction level is highest that we find it helpful to entertain the other side of the investment argument (no matter how utterly wrong-headed that argument may be).

We won’t back off our bear market call unless our model does, but we don’t want overplay our hand, either. Such is the b(ew)itchery of the stock market: We’ve been correctly positioned near our equity minimum, yet we’re somehow compelled to very publicly second-guess that move.

The charts and tables herein are the ones we find the most challenging (even frightening) to our bearish stance—the ones that appear during those fitful nights when we worry, “What could go right?”

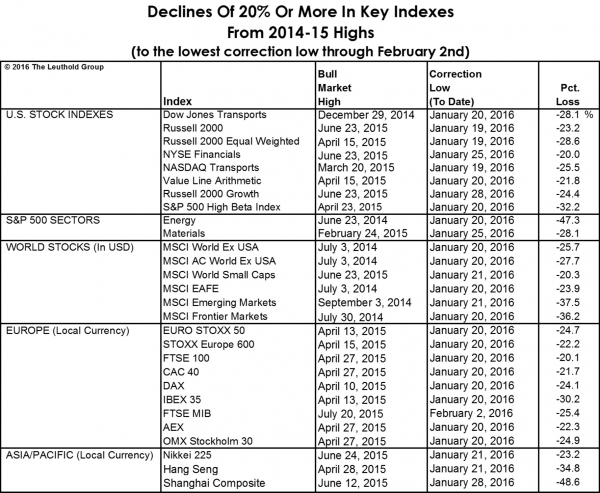

Declines Are Already Substantial

While declines in the S&P 500 and DJIA remain well short of the common -20% bear market definition, losses in most other domestic and global measures have already blown through that threshold.

In most cyclical bear markets, however, the Dow and S&P 500 tend to be not only the “last shoes to drop,” but also the shoes to drop the least when the final losses are tallied. All bear markets hurt. But several cyclical bears have terminated with the S&P 500 in the vicinity of that 20% loss threshold, including 1956-57 (-21.6%), 1966 (-22.2%), 1976-78 (-19.4%), 1990 (-19.9%), 1998 (-19.3%), and 2011 (-19.4%). The new millennium brought with it a pair of costly counter-examples, of course.

· Those who believe a shallow U.S. cyclical bear market is the worst-case outcome should now be preparing their BUY lists—with a particular emphasis on the countries, industry groups, and stocks down the most in price from bull market highs. (Buying high relative strength stocks works most of the time, but not at bear market lows.)

Broad Market No Longer Expensive

Predictably throughout this cycle, P/E ratios based on Forward EPS estimates failed to indicate stocks had become expensive—even at last May’s peak. They never do. It’s why we maintain a diversified list of Intrinsic Value measures (and why ratios using Forward EPS don’t make that list).

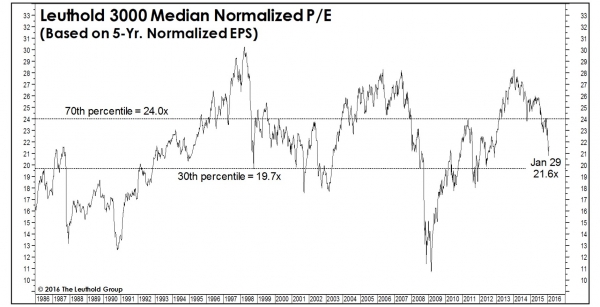

Beginning more than two years ago, we warned that—despite superficially benign readings for the S&P 500—unweighted (median stock) P/E ratios had moved into danger territory. But thanks to the last several months’ collapse in market breadth, the median stock in the Leuthold 3000 universe now trades at a palatable 21.6x 5-Year Normalized EPS (Chart 1)—a shade below its long-term median of 21.9x. (We know—those figures sound high. Remember we’re using a 5-year EPS smoothing.) The broad market has already suffered a significant valuation re-set—a re-set that’s based on a fundamental measure we consider “legit”: Normalized Earnings.

Chart 1

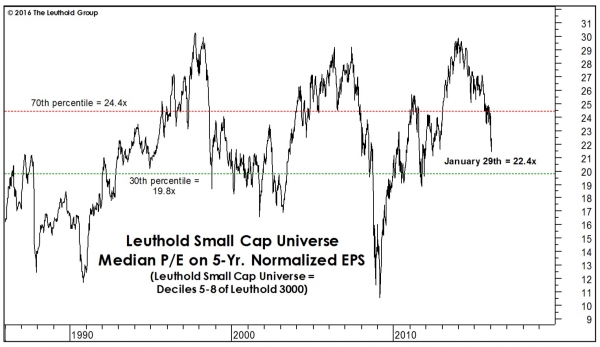

The Small Cap valuation correction has been especially severe, with the median Normalized P/E ratio across the Leuthold Small Cap Universe shrinking by almost eight points, to 22.4x, since the onset of the QE taper in January 2014 (Chart 2). We no longer consider Small Caps overvalued on either a stand-alone or relative basis.

Chart 2

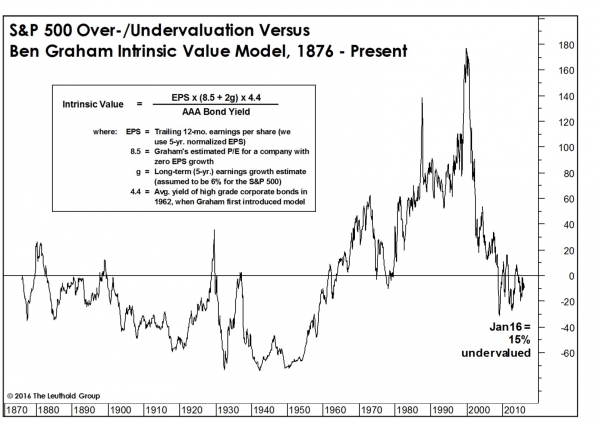

Would Ben Graham Be A Buyer?

While the great Benjamin Graham is certainly a forefather of fundamental investing, in his later years he migrated toward simpler, more mechanistic valuation approaches. We’ve monitored one of them—the Intrinsic Value Model—for about a decade, though we’d emphasize that, unlike Graham’s, our focus has been valuation of stock market composites rather than individual securities.

Our analysis suggests Graham might well be a buyer of the S&P 500 at recent levels (though it’s impossible he’d do so through an index fund). The simple Intrinsic Value Model inputs are few:

· A measure of trailing “economic earnings” (we use our 5-Year Normalized S&P 500 EPS estimate—currently $99.77).

· A long-term EPS growth estimate (6% per annum for S&P 500 is a defensible number, as we’ve discussed many times over the years).

· The average yield available on the shrinking supply of AAA U.S. Corporate bonds (around 4% today).

Plugging these figures into the equation yields a Graham Intrinsic Value S&P 500 estimate of 2250.

· Yes, we recognize that figure sounds like an S&P 500 year-end price target from half a dozen sell-side strategists. (Perhaps there’s more science behind those forecasts than we suspected.)

· This exercise helped us maintain our composure near the 2009 market low, and taken at face value, today’s message is bullish.

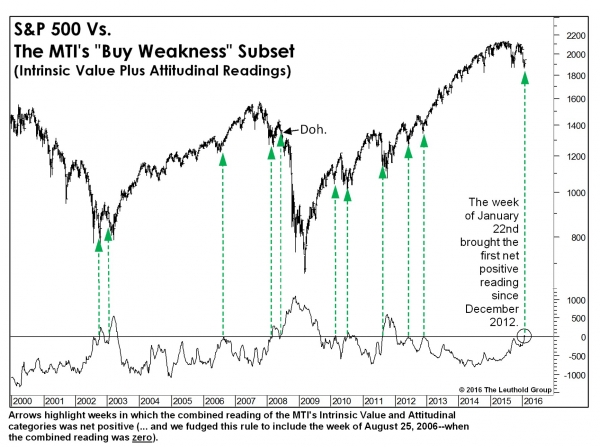

The “Glass Half Full” MTI

While the Major Trend Index remains bearish at 0.80, there have been sizable adjustments within its individual categories over the last year that many readers will find encouraging—if not outright bullish.

The Intrinsic Value and Attitudinal categories are the ones that—practically by definition—benefit from significant price weakness, and we’ve detailed the improvement of both categories in the weekly MTI release. We combined these two indicator groupings to create a “Buy Weakness” MTI subset and found that January’s last two weekly tallies were the first net positive readings since December 2012!

· This “Buy Weakness” subset of the MTI worked terrifically near the 2002 bear market lows, and helped pinpoint most of the latest bull market’s occasional setbacks.

· The bullish tallies in the first of half of 2008 were—it almost goes without saying—spectacular. But bear markets change the boundaries on everything, from technical and economic inputs to the valuation and sentiment work captured here.

· The high batting average of the “Buy Weakness” combo is certainly a challenge to our bearish stance (although we ultimately think the relevant measure for investment decisions is “slugging percentage”).

Bullish Footnote: There are several “countertrend” indicators within the Momentum/Breadth/Divergence category that, if included, would conceivably make this work look even better for the bulls. But isolating and incorporating all of those measures would test the patience of even Leuthold’s original quant, Jim Floyd.

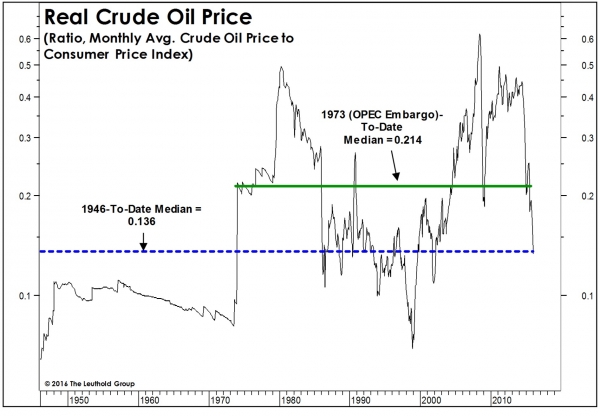

Oil Just Reached A Critical Lower Bound

Oil has played a major role in the stock market (and junk bond) correction, the profits recession, and the near-standstill in manufacturing. But during January crude prices reached our “mental” lower boundary when the inflation-adjusted price of crude oil fell to its 1946-to-date median value.

· This is certainly no magic support level; crude crashed far below that during 1998, for example.But a bet on major downside from here is only for those with extreme agility.

We’ve drawn two historical medians on the accompanying chart, the first being the 1946-to-date figure already referenced. The second (and, we think, more relevant) threshold is the median inflation-adjusted oil price during the OPEC Embargo era (1973-to-date). Note there was a brief bounce in crude at that threshold several months ago.

· We find it ironic that prices have fallen promptly to their longer-term median with OPEC abandoning all market discipline.

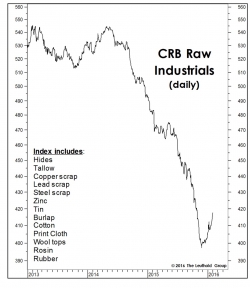

Industrial Economy Bottoming?

Not to minimize the importance of oil, but there’s a commodity index we’ve tracked for decades that’s proven to be an excellent coincident indicator of U.S. industrial activity: the CRB Raw Industrials index (shown in Chart 3, along with its eclectic mix of constituents). And lately, it’s shown signs of life.

· Chart 3

The CRB Raw Industrials index captured, in real-time, the extent of the EM-led manufacturing slowdown throughout 2014 and 2015. We’re now intrigued that the index has quietly managed to rise 5% during a 2 1/2-month span in which global equities are down two to four times that amount.

· This is the best action since the spring of 2014. From a contrary perspective, we like that this move has been overshadowed by the daily gyrations in oil. And, unlike the first half of 2014, virtually no one is calling for a sustained rebound in commodities, let alone this group of commodities that’s so closely tied to the fortunes of Smokestack America. This is the most encouraging omen to emerge from the industrial economy in almost two years.

· Chart 4

January’s bounce in the ISM New Orders Index also suggests that the manufacturing economy may have made a short-term low in December (Chart 4). Make no mistake: the latest reading from this diffusion measure remains weak at 51.5, but that follows contractionary readings (below the 50 level) in three of the past four months.

· The New Orders Index is a component of one of the best market indicators, based solely on economic data, we’ve ever tested.

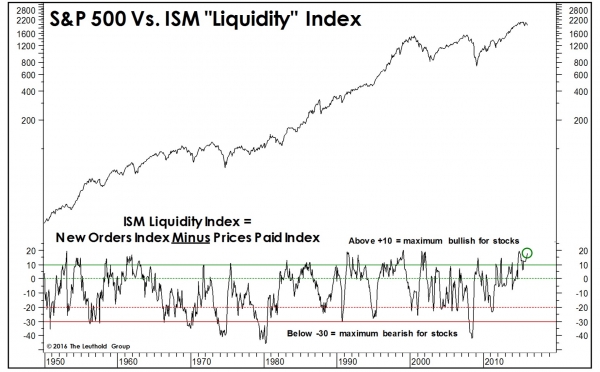

This Economic Model Says BUY

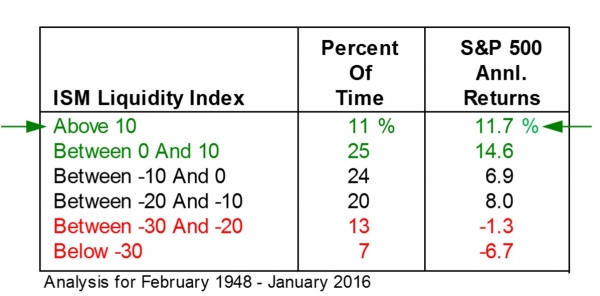

The action of stock, bond, and commodity markets is helpful in forecasting economic variables, but the reverse is only occasionally true. One of the best economy-based forecasting tools we’ve tested is our own ISM Liquidity Index, defined as the spread between the monthly New Orders Index minus the Price Index. The rationale of this simple indicator is that non-inflationary growth provides the best path to stock market prosperity (to paraphrase a CNBC icon).

Bulls might find comfort in January’s extremely high Liquidity Index of 18.0 (New Orders Index of 51.5 minus a seven-year low Price Index of 33.5). This reading ranks in the 98th percentile of all monthly figures since 1948. Admittedly, this work focuses solely on the spread between these two indexes. All else being equal, we’d rather see much higher numbers for both components, but a large and positive spread has itself been historically bullish.

Table 2 summarizes stock market performance associated with varying levels of the ISM Liquidity Index. While we still consider the highest reading to be the most bullish for stocks, historical market results no longer quite conform to that view, thanks to: (1) the latest seasonal adjustments from the ISM’s statisticians; and, (2) the market’s flattish performance over the latest 14-month period. (The Liquidity Index was maximum bullish (i.e., above 10) in 12 of those months.)

Table 2

© 2016 The Leuthold Group. www.leutholdfunds.com