As clients start receiving their 1099-DIV tax forms for 2015 and the implications of their taxable distributions sink in, advisors may want to brace themselves for some challenging conversations.

Indeed, 2015 was another year where many mutual funds had sizable capital gain distributions – but this time it was coupled with underwhelming investment returns. It was truly a double whammy – flat returns + tax hit.

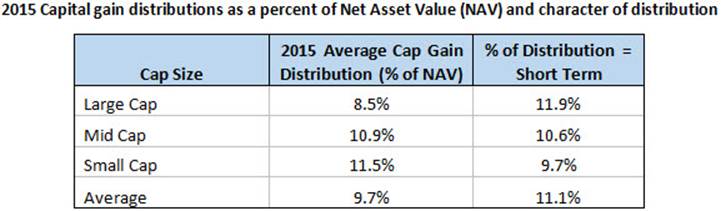

With flat returns in U.S. equity markets in 20151, many investors may have assumed they would have a similarly flat tax bill. But as the table below highlights, for many, that was simply not the case. Thousands of funds – even those with modest or low portfolio turnover and that are not explicitly tax-managed – had sizeable capital gains that reflected the strong equity markets since March 2009.

Source: Morningstar and Russell Investments calculations. Includes all open ended U.S. equity mutual funds to include all both active and passive funds. Includes all share classes.

Think about this. In a year where U.S. stocks generally had uninspiring returns for the year (for example, the Russell 3000® Index was up 0.5%), average equity fund had a 9.7% distribution of the fund’s net asset value as of December 31, 2015.1 In fact, 15% of the mutual funds evaluated had capital gains greater than 15% of their NAV in 2015.2 The 2015 amount is even higher than the previous year’s average of 9.0% of NAV. But 2014 was a different year with the U.S. equity market up 13% ( Russell 3000 Index ).

The after-tax return rub of 2015

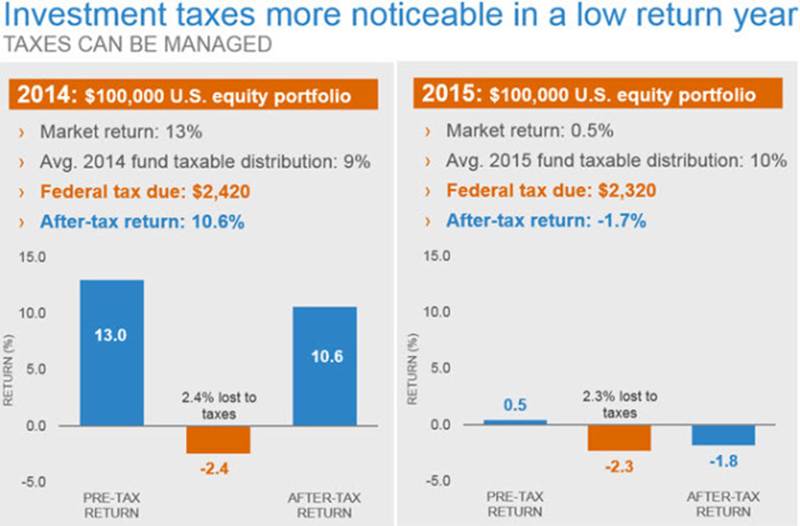

Investors seem to be less bothered by taxes in years when their investments appreciate, like in 2014. The exhibit below shows why that might be the case.

The exhibit represents the pre-tax and after-tax returns of a hypothetical $100,000 investment in a portfolio whose pre-tax return matched that of broad equity markets in both 2014 and 2015.

Note the impact of the taxable distribution on the after-tax return. Although the total federal tax due is essentially the same in both years ($2,420 in 2014 and $2,320 in 2015), the after-tax returns are very different from one year to the next. In 2015, the tax liability actually pulls the after-tax return into negative territory – because it exceeds the amount of pre-tax return.

Hypothetical example for illustrative purposes only. Market return: Russell 3000® Index. Average Taxable Distribution includes average capital gain distribution for all Morningstar U.S. equity categories for listed year. Distribution is assumed to be made the last day of the year and reinvested. Tax rate is 23.8% (Max ST Cap Gain 20% + Net Investment Income 3.8%). Returns represent past performance, are not a guarantee of future performance, and are not indicative of any specific investment.

Additional comments on the above exhibit:

- This example would look worse if we had assumed that any of the distributions were short-term in character – the tax hit would be larger. As it is, the exhibit assumes a long-term capital gains tax rate of 23.8% (top rate of 20% + 3.8% for Net Investment Income).

- While the tax hit in 2014 may feel less punitive because of the positive equity return, it is no less corrosive than 2015’s tax. Consider a tax-managed strategy that is able to reduce the tax to $500 (a ~2% distribution). That would leave an additional $1,920 in the investor’s account ($2,420 – $500). And imagine what the power of compounding can do to $1,920 as it grows in subsequent years. This is the real power of tax-managed investing. Keeping more of what you earn and unleashing the power of compounding to help grow investment amounts for successful future outcomes.

Taxes related to investments can be managed. Investors don’t have to accept an average after-tax outcome such as the exhibit above. Tax-managed funds can use strategies throughout the year to try and reduce the impact of taxes. Think of the recent volatility in global equity markets. While this volatility can be unsettling, an active tax-managed approach has the potential to harvest this volatility in an attempt to create tax losses to be used against gains in current or future periods. Done successfully, this can help to defer gain recognition and improve after-tax returns.

The bottom line

Taxes can be a major headwind for taxable investors. 2015 was a year where investors likely experienced underwhelming returns and witnessed investment-related taxes in line with those of 2014. Except, the silver lining in 2014 was a respectable equity market return. It does not have to be this way, though. Taxes can be managed. Make sure your client’s taxable assets have a tax-managed approach to help improve their odds for successful outcomes.

1 Represented by the Russell 3000® Index.

2 Source: Morningstar and Russell Investments calculations.

The Russell 3000® Index: Measures the performance of the largest 3000 U.S. companies representing approximately 98% of the investable U.S. equity market.

Strategic asset allocation and diversification do not assure profit or protect against loss in declining markets.The general information contained in this publication should not be acted upon without obtaining specific legal, tax, and investment advice from a licensed professional.

Returns represent past performance, are not a guarantee of future performance, and are not indicative of any specific investment.

Indexes are unmanaged and cannot be invested in directly.

Russell Investments is a trade name and registered trademark of Frank Russell Company, a Washington USA corporation, which operates through subsidiaries worldwide, including Russell Financial Services, Inc., member FINRA. Russell Investments is part of London Stock Exchange Group.

Copyright © Russell Investments 2016. All rights reserved.

This material is proprietary and may not be reproduced, transferred, or distributed in any form without prior written permission from Russell Investments. It is delivered on an “as is” basis without warranty.

RFS 16661