The markets had a great run until last August—years of rising prices across nearly every asset class. Unfortunately, long-term investing doesn’t stay that easy.

The synchronized actions of the global central banks, the primary driver of those halcyon days, have devolved into disparate, competitive, unpredictable, pronouncements. Now, the factors that helped keep the waters calm and rising for several years are creating major turbulence; and there’s reason to expect a period of heightened volatility lasting at least as long as the abnormally pacific one that just ended.

No, it’s not just a question of whether the Fed raises rates—the chances for which during this year, I believe, the market is seriously underestimating. Because even if the Fed goes “one and done” with its hikes, it will be on a radically different course than the other central banks. They aren’t just implementing a zero-interest-rate-policy (ZIRP), but some are actually moving to negative-interest- rate-policy (NIRP), rates below zero. And there is serious chatter about even more extreme policies, like “helicopter money.” That means that even if the Fed merely stands still, the resulting policy divergences could set off currency fireworks that, in our highly leveraged and fully interdependent globalized economy, could mean asset price spasms for years to come.

The impact could be amplified by two less obvious changes. One is an elephant hiding in plain sight: the exponentially rising impact of automatic investing. Many trillions of investment dollars are on autopilot, directed by formulas to buy and sell in reaction to market moves, and without regard for price or value. In such ways, ticks are amplified into trends. Simultaneously, we’ve lost critical financial shock absorbers, like bank market makers and prop trading desks that, in the past, have distributed and diluted sudden asset flows reasonably well.

Money Machines

The Fed’s extraordinary monetary policies of the past few years have done exactly what they were intended to do: raise asset prices. If you doubt for a moment that this was the explicit point, or that the game is now over, take a listen to Dick Fisher, the immediate past president of the Dallas Fed, speaking earlier this year:

“What the Fed did, and I was part of it, was front-loaded an enormous market rally in order to create a wealth effect… and an uncomfortable digestive period is likely now.”

Indeed, the Fed has been playing less potent versions of this game all the way back to the days of the famous “Greenspan put”, the satirically named, but highly predictable, policy of easing credit conditions in response to each serious market downturn. Bernanke and Yellen took such policies to new levels with ZIRP and quantitative easing. As a result, quite ironically, our own Fed slowly rendered ever less relevant organic pricing based on factors like the cost of capital, risk, and future profitability.

But it now seems to understand that the jig is up, that stimulus too is subject to the law of diminishing returns. Indeed, there’s a creeping realization that much of the excess liquidity of the past few years flowed into overproduction, as in the oil patch, and so created short-term jobs but long-term deflationary pressures, an unintended consequence of the most extreme sort.

So now we’re headed back to the future. And we believe that return path to pricing off fundamentals, instead of the Fed’s next generous move, is bound to be rocky, treacherous and, for many, disappointing.

But in our modern world, the monetary policy drama hardly ends there. The other major central banks, looking for their own economic adrenaline, adopted and administered our medicine in even greater doses than we did. Extraordinary liquidity became not just an emergency tool for last-ditch financial rescues, but rather a daily vitamin to buck up ailing stock markets, bleak employment numbers, and overall economic health. No need for difficult things like fiscal action by governments, clearing regulatory arteries, or entrepreneurial vigor. Just print and borrow until prosperity arrives.

So while we may be in a digestive period, as Dick Fisher says, the rest of the globe’s powers continue to imbibe. Sovereign bonds trading with negative rates now total an incredible $7 trillion. This is simply astonishing, all the more so given that mainstream economists had always thought the phenomenon literally impossible until it started to happen merely months ago. According to Bloomberg News, 29% of the global economy is now overseen by central banks propagating negative rates.1

Needless to say, this matters, not least because interest rate wars are also currency wars. Of course, capital will generally seek to leave a negative rate currency in search of better returns, and so depress that currency’s value.

Central banks like that because lower currency values help their exporters, and also help them hit inflation targets—with so much debt outstanding, deflation would be a true disaster. The competitive nature of this game is obvious—Japan’s recent move to negative rates was a direct response to the devaluation of the Chinese Yuan—and is not likely to end soon.

This Great Divergence, the Fed versus the Rest of the World (and the Rest of the World against itself), looms as a dominant theme of global finance for years to come. The resulting currency volatility is nearly certain to spill into securities prices. On the most basic level, consider the consequences for U.S. corporate earnings: Apple, for example, derives two- thirds of its revenues from overseas2 and must be translated back into dollars for earnings reports, and many of the largest companies in the [S&P 500] now derive more than half from foreign sources.

But other crucial consequences are more subtle, and harder to foresee. For example, China has been selling big chunks of Treasuries to raise the cash necessary for its various market interventions; and other sovereign holders have too, for similar reasons. This exerts substantial and surprising downward pressure on Treasuries during periods of stock market turbulence, and can more than offset the standard “stocks down/bonds up” logic that is built into many allocation models. Another new dynamic: foreign issuers around the globe have raised $4 trillion or so of USD-denominated debt over the past few years, often supported by expected commodity sales to China; their debt has gotten much more expensive as their revenues have collapsed.

Such unintended, and unpredictable, consequences of the Great Divergence will keep appearing; and as they do, the game theory reactions of each affected country’s policy makers are simply not knowable. There is no playbook for what happens next.

As a result, asset prices are likely to kaleidoscope in highly unpredictable patterns for years to come. Oil is merely exhibit A.

Automatic Accelerants

High frequency trading has a significant impact on exchanges; Commodity Trading Advisors race each other to identify and follow trends; risk parity strategies instantaneously buy and sell massive asset baskets to maintain their volatility budgets; rebalancing formulas adjust enormous portfolios at least daily. Meantime, there is about $3 trillion in ETFs that mechanically buy and sell preselected securities. And the Age of Automatic Investing appears to be reaching a zenith as robo-advisors are unleashed by nearly every major brokerage and advisory firm.

The “wisdom” of such trends is beyond the scope of this article. Here, we are concerned only with the way these forces can amplify any small movement into a significant, self-reinforcing trend, and thereby exacerbate volatility and divorce securities’ prices from the underlying fundamentals.

Indeed, the first two months of 2016 have seen more days with a 1% move than any year in history even though the actual economic news has been relatively muted. So the moves do not appear to be driven by thoughtful reevaluation of fundamentals. The “tick to trend” impact of automatic investing is one of the few plausible explanations.

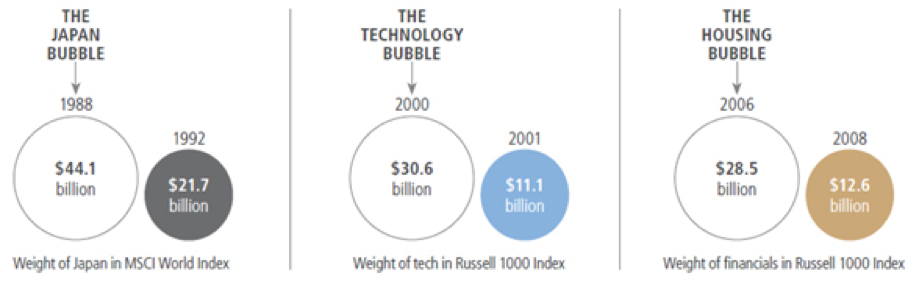

It’s interesting to see how, as indexed investing has become more popular, so have its distortive effects. The phenomenon itself isn’t new; think back to the finance, tech or Japanese bubbles. Each time, the sector du jour comes to dominate the related cap weighted index (say the MSCI or S&P), attracting an ever greater percentage of new flows into the related investment vehicles.

It’s often a self-reinforcing loop—until it creates a bubble that bursts.

But the passive investing tidal wave since the Great Financial Crisis has taken these distortions to a new level. Consider:

In 2006, the average stock included in the Russell traded at about a 12% premium to other small stocks; today, that premium is 50%. Perversely, “passive” investing itself is dividing winners from losers.3

Risk Is Relevant: Bubbles Burst!

As bubbles form, indexes buy “over-weighted” positions following popular trends. For index investors, the danger is the ease with which you participate in that bubble.

Source: PIMCO, MSCI, Bloomberg.

So now imagine what can happen when we layer in all the warring algorithms of competing players with different motives, and especially ones specifically aiming to exploit other systems’ weaknesses (such as ETF pricing mechanisms). Actually, you don’t have to imagine: just look at last August 24, the largest point swing day in history. And note that 42% of U.S. equity ETFs experienced trading halts, even though just eight S&P stock did; and fully one-fifth of equity ETFs saw price swings of 20% or more.

Broken Breakers

Of all the great contradictions of the past few years, none surpasses the Fed’s efforts to foster risk-taking in to our economic system and to deter it at the same time. “Risk on” was encouraged by those massive liquidity injections, and “risk off” was attempted by significantly inhibiting financial institutions’ market making and prop desk activities through express bans on proprietary trading (via Dodd Frank) and imposition of prohibitive capital charges on financial asset inventories (via Basel III and other new bank capital standards). Our largest financial institutions, which historically ameliorated unwarranted short-term securities price movements (in order, of course, to profit from them over time) are now largely foreclosed from that role.

If you create more risk, but limit the financial system’s ability to absorb the resulting volatility, what happens? Shocks are instantly transmitted into securities prices in ways more dramatic than would have previously been the case.

The primary concern here is the credit markets, in which the banks had served as the primary market makers in a clunky over-the-counter system. And just as they’ve decamped, the percentage of bonds owned by patient institutional holders has fallen dramatically, while the number in “hot money” hands such as ETFs and mutual funds has soared. Very many of these new investors may not appreciate just how much interest rate and duration risk they’re sitting on. Any shift to higher rates could trigger selling pressure, which, without the traditional bank market makers in place, could easily spiral into serious price dislocations.

Volatility’s Back

Volatility was artificially dampened for years by intertwined phenomena: trillions of dollars of synchronized central bank liquidity injections, and the rise of “automatic investing” as all those dollars flooded in on the long side. All systems were go, and everyone was headed in the same direction.

No longer. As the Fed’s elixir is withdrawn over the next several years, we may be forced back into a world of fundamentally driven prices. That road would have been jarring in any event, but now each shaky step will be amplified by the tidal waves of reactions—and reactions to reactions—of both global policy makers and all the new automatic investing systems and formulas. Those price moves won’t be cushioned by the traditional financial shock absorbers that might have damped them in days gone by.

Volatility had a great vacation. It may have returned to work refreshed and recharged.

About Bob Rice

Bob Rice, Senior Advisor to Neuberger Berman, is a financial expert, best-selling author and is a frequent guest speaker on several national business news programs. Bob uses his 25 years of experience in non-traditional investments as an advisor, lawyer and principal to work with advisory firms engaged with Neuberger Berman. He is the author of The Wall Street Journal bestseller, The Alternative Answer. Bob has served as a financial products partner at Milbank Tweed; the CEO of a publicly traded technology company (the successor to his own startup); and a trial lawyer for the U.S. Department of Justice.

1 Source: Bloomberg, February 9, 2016.

2 Source: Apple Inc. Q1 2016 Investor Call, CEO Tim Cook: “66% of Apple’s revenue is now generated outside the United States, so foreign currency fluctuations have a very meaningful impact on our results.”

3 Source: S&P Capital IQ as of 12/31/15.

This material is provided for informational purposes only and nothing herein constitutes investment, legal, accounting or tax advice, or a recommendation to buy, sell or hold a security. Information is obtained from sources deemed reliable, but there is no representation or warranty as to its accuracy, completeness or reliability. All information is current as of the date of this material and is subject to change without notice. Any views or opinions expressed may not reflect those of the firm or the firm as a whole. Neuberger Berman products and services may not be available in all jurisdictions or to all client types. This material may include estimates, outlooks, projections and other “forward-looking statements.” Due to a variety of factors, actual events may differ significantly from those presented. Investing entails risks, including possible loss of principal. Indexes are unmanaged and are not available for direct investment. Past performance is no guarantee of future results.

This material is being issued on a limited basis through various global subsidiaries and affiliates of Neuberger Berman Group LLC. Please visit www.nb.com/disclosure-global-communications for the specific entities and jurisdictional limitations and restrictions.

The “Neuberger Berman” name and logo are registered service marks of Neuberger Berman Group LLC.

Certain products and services may not be available in all jurisdictions or to all client types.

© 2009-2016 Neuberger Berman LLC. | All rights reserved