Commodities

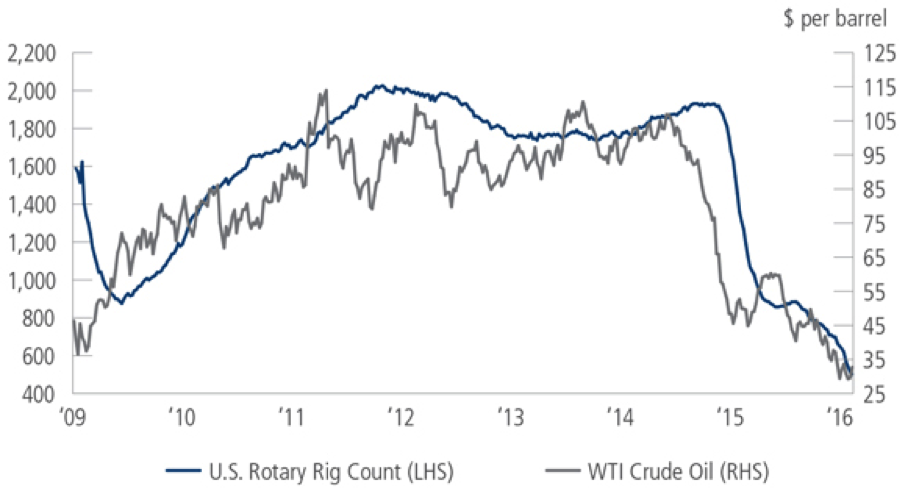

We are maintaining a neutral view and anticipate ongoing choppiness across the commodities complex in the near term. Precious metals have been strong performers against a backdrop of volatile equity markets, negative interest rates and a slightly weaker dollar, and crude oil and industrial metals have recovered from declines in early February. Oil remains a wild card but, in our view, a bottom may be forming with supply/demand potentially coming back into balance later this year or in early 2017.

Commodities: Falling Rig Count May Lead to Improved Supply/Demand Dynamics

Source: FactSet. Data as of February 29, 2016.

Hedge Funds

Committee members vigorously debated our views on hedge funds this quarter, but in the end elected to maintain our slightly above normal return outlook for both lower volatility and directional hedge funds. Within lower volatility hedge funds, unusual circumstances—crowded trades, exposure to the challenged sectors—hampered performance in an investment segment we felt should perform well. We continue to believe that these strategies offer an attractive risk/return balance given their ability to help buffer market shocks and their return potential in range-bound markets.

Private Debt

Yields available from private debt investing have been rising, presenting many attractive opportunities for investors who can lock up capital. Due to the current risk environment, however, the Committee feels it is important to avoid segments within private debt that are cyclical in nature or non-recurring. Energy and new issuance may present higher risks for the time being, but credits that we feel have been unfairly penalized could offer compelling return potential. In our view, distressed debt, particularly within a private equity versus a hedge fund vehicle, appears attractive.

Currency

U.S. Dollar: The Committee moderated its view for the dollar based on a more dovish FOMC rate path and communication that was delivered in March. While a strong labor market and aggressive easing by other major central banks may lend support to the USD, we believe currency markets have priced in these expectations accordingly and thus we anticipate a more constrained dollar following multiple years of strength.

Euro: We are holding a slightly underweight view of the euro, and anticipate that it will be range-bound in the near term. Weaker-than-expected inflation dynamics are likely to drive more ECB easing. Uncertainty about the global economy and broader geopolitical risks are also dampening our view.

Yen: We hold a slightly overweight view as a long yen remains a valid hedge against global risk aversion. In addition, PPP and real exchange rates may indicate that the yen is still undervalued against other G10 currencies.

Pound: A number of factors are contributing to our overweight view of the pound. The UK is experiencing relatively strong growth and supportive dynamics in output growth exist. Further, interest rate market pricing of a Bank of England hike is very low and we believe that the “Brexit” risk premium is attractive.

Swiss Franc: We hold an underweight view of the Swiss franc, believing it is overvalued and at risk of ongoing weakness.

EM FX (broad basket): We anticipate that pressure on EM currencies will continue until we see a more constructive and durable backdrop for global growth and commodities.

About the Asset Allocation Committee

Neuberger Berman’s Asset Allocation Committee meets every quarter to poll its members on their outlook for the next 12 months on each of the asset classes noted. The panel covers the gamut of investments and markets, bringing together diverse industry knowledge, with an average of 24 years of experience.

This material is provided for informational purposes only and nothing herein constitutes investment, legal, accounting or tax advice, or a recommendation to buy, sell or hold a security. Information is obtained from sources deemed reliable, but there is no representation or warranty as to its accuracy, completeness or reliability. All information is current as of the date of this material and is subject to change without notice. Any views or opinions expressed may not reflect those of the firm as a whole. Neuberger Berman products and services may not be available in all jurisdictions or to all client types. Investing entails risks, including possible loss of principal. Investments in hedge funds and private equity are speculative and involve a higher degree of risk than more traditional investments. Investments in hedge funds and private equity are intended for sophisticated investors only. Indexes are unmanaged and are not available for direct investment. Past performance is no guarantee of future results.

The views expressed herein are generally those of Neuberger Berman’s Asset Allocation Committee which comprises professionals across multiple disciplines, including equity and fixed income strategists and portfolio managers. The Asset Allocation Committee reviews and sets long-term asset allocation models, establishes preferred near-term tactical asset class allocations and, upon request, reviews asset allocations for large diversified mandates and makes client-specific asset allocation recommendations. The views and recommendations of the Asset Allocation Committee may not reflect the views of the firm as a whole and Neuberger Berman advisors and portfolio managers may recommend or take contrary positions to the views and recommendation of the Asset Allocation Committee. The Asset Allocation Committee views do not constitute a prediction or projection of future events or future market behavior. This material may include estimates, outlooks, projections and other “forward-looking statements.” Due to a variety of factors, actual events or market behavior may differ significantly from any views expressed.

A bond’s value may fluctuate based on interest rates, market conditions, credit quality and other factors. You may have a gain or a loss if you sell your bonds prior to maturity. Of course, bonds are subject to the credit risk of the issuer. If sold prior to maturity, municipal securities are subject to gain/losses based on the level of interest rates, market conditions and the credit quality of the issuer. Income may be subject to the alternative minimum tax (AMT) and/or state and local taxes, based on the investor’s state of residence. High-yield bonds, also known as “junk bonds,” are considered speculative and carry a greater risk of default than investment-grade bonds. Their market value tends to be more volatile than investment-grade bonds and may fluctuate based on interest rates, market conditions, credit quality, political events, currency devaluation and other factors. High Yield Bonds are not suitable for all investors and the risks of these bonds should be weighed against the potential rewards. Neither Neuberger Berman nor its employees provide tax or legal advice. You should contact a tax advisor regarding the suitability of tax-exempt investments in your portfolio. Government Bonds and Treasury Bills are backed by the full faith and credit of the United States Government as to the timely payment of principal and interest. Investing in the stocks of even the largest companies involves all the risks of stock market investing, including the risk that they may lose value due to overall market or economic conditions. Small- and mid-capitalization stocks are more vulnerable to financial risks and other risks than stocks of larger companies. They also trade less frequently and in lower volume than larger company stocks, so their market prices tend to be more volatile. Investing in foreign securities involves greater risks than investing in securities of U.S. issuers, including currency fluctuations, interest rates, potential political instability, restrictions on foreign investors, less regulation and less market liquidity. The sale or purchase of commodities is usually carried out through futures contracts or options on futures, which involve significant risks, such as volatility in price, high leverage and illiquidity.

This material is being issued on a limited basis through various global subsidiaries and affiliates of Neuberger Berman Group LLC. Please visit www.nb.com/disclosure-global-communications for the specific entities and jurisdictional limitations and restrictions.

Certain products and services may not be available in all jurisdictions or to all client types.

© 2009-2016 Neuberger Berman LLC. | All rights reserved