Several highly punitive credit downgrades of higher-quality energy companies surprised the investment grade bond market recently, with some downgrades representing cuts of four to five notches. But Invesco Fixed Income believes there may be a silver lining to these downgrades: Together with low commodity prices, these moves may be driving a positive shift toward more prudent corporate balance sheet management, largely in favor of creditors. While commodity price volatility, an oversupplied oil market and broader macroeconomic uncertainty cause us to be very cautious about investing in energy-related credit, we believe such volatility and change in corporate behavior may create unique opportunities for active investment managers.

Fundamental crude outlook downgraded, but companies have responded positively

Forward commodity price assumptions are key inputs in the credit-rating process of many energy-related companies. Following OPEC’s (Organization of the Petroleum Exporting Countries) decision to leave currently elevated production levels in place at its December meeting (rather than agreeing to any form of production freeze or reduction), crude prices have remained volatile in 2016. Rating agencies have accordingly lowered their forward commodity price assumptions under the view that oil price weakness could persist for an extended period of time. These price assumption revisions have resulted in meaningful credit rating downgrades.

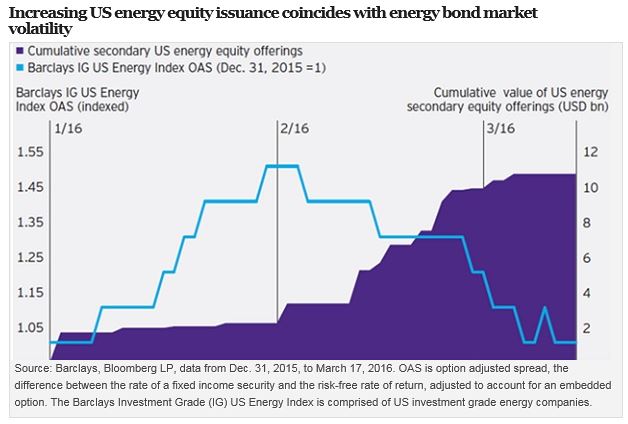

We believe that certain rating agencies have taken the view that depressed commodity prices may have severely compromised the energy industry’s cash flow generative capacity. Historically, if a company anticipated generating negative cash flow given large capital expenditure requirements, it could typically fully or partially offset this with public debt or equity issuance. However, with capital markets remaining highly volatile during recent months, many energy companies have generated negative cash flow while being unable to fully access debt and equity markets.

While this funding gap has proven highly negative from a ratings standpoint, the silver lining is that it has forced reductions in both operating and capital spending to better align operating cash flow with capital expenditures throughout the industry. When combined with rating agency downgrade risk, the result is an ongoing shift in industry-wide balance sheet and cash flow management, largely to the ultimate benefit of bondholders, in our view.

Commodity weakness and ratings downgrades spur renewed balance sheet focus

As industry-wide cost structure rationalization continues, we expect companies to remain keenly focused on:

- Targeting breakeven cash flow at depressed commodity prices (exclusive of capital market access).

- Reducing balance sheet and cash flow risk via dividend reductions, asset sales, equity offerings, etc.

We have recently seen a number of companies execute on various balance sheet-oriented corporate actions, including equity offerings, asset monetizations, reductions in capital spending programs, tender offers and dividend reductions or eliminations, and we expect this behavior to continue.

Remaining nimble, disciplined and opportunistic while cautiously awaiting industry recovery

Given a renewed focus by management teams on maintaining healthy balance sheets, Invesco Fixed Income anticipates further creditor-friendly corporate activity. As energy balance sheets continue through the de-risking process, downside creditor protection should be further enhanced, in our view — a key requirement of our highly selective investment process. While we remain highly cautious and selective in the near term, it is encouraging to see a focus on balance sheet strengthening from management teams across the industry. We continue to await further improvement in crude market fundamentals, but we believe the ongoing balance sheet preservation trend will potentially provide unique investment opportunities for selective, risk-averse, value-oriented credit investors in the volatile commodity price environment.

We remain highly focused on selectively evaluating the volatile energy landscape in search of investment opportunities that exhibit a few key investment attributes:

- Attractive downside protection afforded through favorable competitive and/or operating characteristics

- Strong near-term liquidity

- Identifiable positive catalysts

- Attractive risk-adjusted return potential

Important information

Businesses in the energy sector may be adversely affected by foreign, federal or state regulations governing energy production, distribution and sale as well as supply-and-demand for energy resources. Short-term volatility in energy prices may cause share price fluctuations.

Commodities may subject an investor to greater volatility than traditional securities such as stocks and bonds and can fluctuate significantly based on weather, political, tax, and other regulatory and market developments.

Fixed-income investments are subject to credit risk of the issuer and the effects of changing interest rates. Interest rate risk refers to the risk that bond prices generally fall as interest rates rise and vice versa. An issuer may be unable to meet interest and/or principal payments, thereby causing its instruments to decrease in value and lowering the issuer’s credit rating.

The information provided is for educational purposes only and does not constitute a recommendation of the suitability of any investment strategy for a particular investor. Invesco does not provide tax advice. The tax information contained herein is general and is not exhaustive by nature. Federal and state tax laws are complex and constantly changing. Investors should always consult their own legal or tax professional for information concerning their individual situation. The opinions expressed are those of the authors, are based on current market conditions and are subject to change without notice. These opinions may differ from those of other Invesco investment professionals.

All data provided by Invesco unless otherwise noted.

Invesco Distributors, Inc. is the US distributor for Invesco Ltd.’s retail products and collective trust funds. Invesco Advisers, Inc. and other affiliated investment advisers mentioned provide investment advisory services and do not sell securities. Invesco Unit Investment Trusts are distributed by the sponsor, Invesco Capital Markets, Inc., and broker-dealers, including Invesco Distributors, Inc. PowerShares® is a registered trademark of Invesco PowerShares Capital Management LLC (Invesco PowerShares). Each entity is an indirect, wholly owned subsidiary of Invesco Ltd.

©2016 Invesco Ltd. All rights reserved.

Energy bonds: Finding the silver lining in credit downgrades by Invesco Blog