A Tale of Two Markets: Dividend, Low Volatility and Quality Factors Earn Top Spots in Q1 2016

The first quarter of 2016 has come to a close, and what a period it was. The past quarter’s returns were a clear testament to the power of factor investing, and provide further evidence that smart beta strategies can add value to a diversified portfolio.

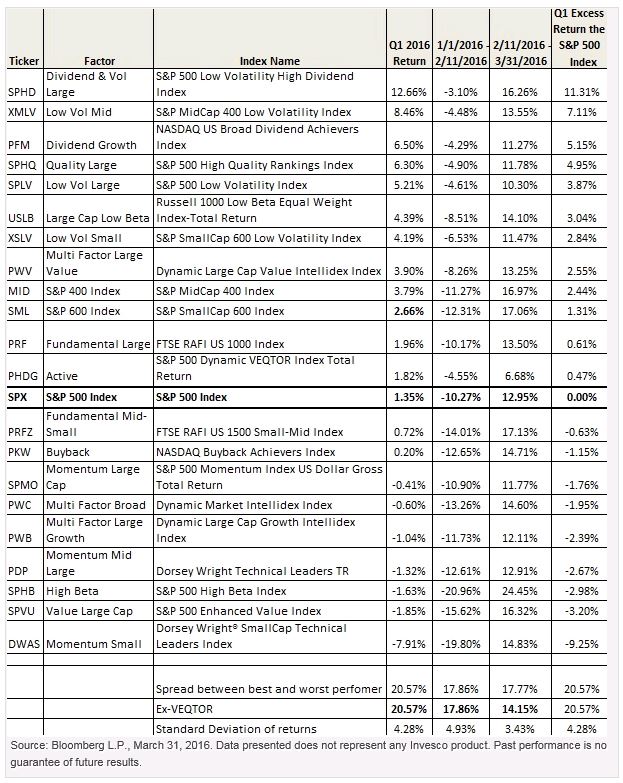

As shown in the table below, the dividend, low volatility and quality factors were the best performers during the first quarter, while the small-cap momentum, value and high beta factors lagged.

Interest rates, credit risk helped drive first-quarter returns

Macroeconomic conditions were favorable for the low volatility, quality and dividend factors – helping drive first quarter returns. Momentum stocks were hurt by investors’ propensity to make sector bets without discriminating between strong and weak companies.

In my view, these were the key drivers of first-quarter returns:

Falling interest rates: The decline in the German 10-year bond yield from 63 basis points to 15 basis points put pressure on the US 10-year Treasury yield.1 Falling sovereign yields triggered strong flows into dividend-yielding stocks, as investors sought income opportunities in a low interest rate environment. Because one characteristic of low volatility stocks is the payment of dividends, it is not surprising that the low volatility factor outperformed amid falling Treasury yields and heightened market volatility. Of course, low volatility cannot be guaranteed.

Wider credit spreads: Rising credit risk has historically benefited the low volatility and quality factors, and credit stress was indeed profound during the first quarter. High yield spreads, as measured by the BarCap US Corporate High Yield Index, shot to nearly 8.50% above the 10-year Treasury bond, before narrowing later in the quarter.1

Market volatility: Market volatility, as measured by the CBOE Volatility Index (VIX), spiked during the first part of the quarter before tailing off after Feb. 11.

Economic uncertainty: During the quarter, investors were concerned about global economic health. This was evident in the Economic Policy Uncertainty Index, which jumped from a level of 99.3 in December to 150.86 in February, before settling to 118.22 in March.1 Stocks with low risk and quality characteristics tend to see increased demand during periods of economic uncertainty.

A tale of two markets

The first quarter was really a tale of two markets. The first six weeks of the period were marked by significant market volatility, before recession and credit fears abated. Despite early market upheaval, commodity prices showed strength and pointed to steady economic growth. This was confirmed by the rebound in the ISM Manufacturing Index late in the quarter. The following table highlights the performance dispersion of market drivers during the first quarter.

A shift in the macroeconomic backdrop after Feb. 11 led to a marked change in the performance of many different factors. High beta, as represented by the S&P 500 High Beta Index, was the best performer in the back half of the first quarter – jumping nearly 24.5%. Value, fundamental weight and buyback – a form of value strategy – also displayed strength, as can be seen in the first table. Surprisingly, low volatility and high dividend remained in the top-performing camp even as market conditions improved. Falling rates abroad may have played a role in this phenomenon. Meantime, signs of economic recovery fueled the performance of economically sensitive value and high-beta stocks.

Key Q1 2016 takeaways

So what can we take away from first-quarter factor results?

- Low volatility showed clear upside participation with limited downside exposure. The low volatility factor generated excess return by outperforming in down markets during the quarter. As a result, it had less ground to make up when markets stabilized. The S&P 500 Low Volatility Index declined about 4.60% in the first half of the quarter, while the S&P 500 Index declined more than 10.25%. And while the S&P 500 Low Volatility Index lagged the S&P 500 Index on the upside, it still outperformed the broader market during the quarter as a whole. Mid-cap and small-cap low volatility returns demonstrated similar patterns during the first quarter, with downside cushion making up for lower returns on the upside.

- There were benefits to multi-factor strategies. Multi-factor strategies paid off in the first quarter, as evidenced by the combination of large-cap low volatility and dividend (S&P 500 Low Volatility High Dividend Index), which outperformed all other factors by a wide margin. In addition, the combination of low beta and equal weight (Russell 1000 Low Beta Equal Weight Index – Total Return) offered investors the benefit of a reduced-risk portfolio via a low beta strategy, while providing access to value and size through equal-weighting.

- Lastly, it is interesting that the dispersion in return (as measured by standard deviation and the spread between high- and low-performing factors) lessened dramatically when the overall market rallied – suggesting that factor-based strategies may add measurable value in down markets.

While valuations may be important, it is abundantly clear that the larger macroeconomic environment plays a critical role in driving factor returns, at least over short-term periods.

Investors looking for access to the large-, mid-, or small-cap low volatility factor may wish to consider the PowerShares S&P 500 Low Volatility Portfolio (SPLV), the PowerShares S&P MidCap Low Volatility Portfolio (XMLV) or the PowerShares S&P SmallCap Low Volatility Portfolio (XSLV), or a combination of these.

Likewise, investors interested in the large-cap quality factor may wish to consider the Powershares S&P 500 Quality Portfolio (SPHQ).

1 Source: Bloomberg L.P., March 31, 2016

Important information

Past performance is no guarantee of future results.

A basis point is one hundredth of a percentage point.

Beta is a measure of risk representing how a security is expected to respond to general market movements.

Excess return refers to excess return generated by one index, strategy or investment factor over another.

Spread represents the difference between the yield on a corporate bond and a similar maturity US Treasury bond.

Standard deviation measures a portfolio’s range of total returns and identifies the spread of a portfolio’s short-term fluctuations.

Dividends/High Dividend: Shows how much a company pays out each year to shareholders relative to its share price. Companies characterized as high dividend tend to issue higher annual payouts. Securities that pay high dividends as a group can fall out of favor with the market, causing such companies to underperform companies that do not pay high dividends.

Dividend Growth: Ranks securities by their dividend yield while seeking to increase overall portfolio yield and potential for improved price performance.

Low Volatility: Utilizes volatility rankings while seeking to minimize the effects of market fluctuations. Volatility is a statistical measurement of the magnitude of up and down asset price fluctuations over time. Of course, low volatility cannot be guaranteed.

Volatility: Measures the amount of fluctuation in the price of a security or portfolio.

Momentum: Ranks securities relative to peers, utilizing relative strength methodology to identify the strongest and weakest investment trends. Momentum investing is subject to the risk that the securities may be more volatile than the market as a whole, or that the returns on securities that have previously exhibited price momentum are less than returns on other styles of investing.

Quality/High Quality: A ranking that reflects the long-term growth and stability of a company’s earnings and dividends. Focuses on companies that have a Standard & Poor’s quality ranking of A- or above that have historically exhibited higher Sharpe ratios and lower volatility.

High Beta: Utilizes a beta-weighted methodology to increase exposure to market movements of a benchmark without incorporating leverage. (Beta is a measure of risk representing how a security is expected to respond to general market movements.) Beta investing entails investing in securities that are more volatile based on historical market index data.

Buyback: Tracks US companies that consistently repurchase their own outstanding shares used by institutions and active managers for decades.

Fundamentals Weighted: Ranks all publicly listed US companies according to four fundamental measures of company size: sales, cash flow, book value and dividends.

The CBOE Volatility Index® (VIX®) is a key measure of market expectations of near-term volatility conveyed by S&P 500 stock index option prices. VIX is the ticker symbol for the Chicago Board Options Exchange (CBOE) Volatility Index, which shows the market’s expectation of 30-day volatility.

The Economic Policy Uncertainty Index is compiled from three underlying components that quantify newspaper coverage of policy-related economic uncertainty, reflect the number of federal tax code provisions set to expire in future years, and use disagreement among economic forecasters as a proxy for uncertainty.

The ISM Manufacturing Index, which is based on Institute of Supply Management surveys of more than 300 manufacturing firms, monitors employment, production inventories, new orders and supplier deliveries.

The S&P 500 Low Volatility High Dividend Index is composed of 50 securities traded on the S&P 500 Index that historically have provided high dividend yields and low volatility.

The NASDAQ US Broad Dividend AchieversTM Index is comprised of 50 stocks selected principally on the basis of dividend yield and consistent growth in dividends.

The S&P MidCap 400 Low Volatility Index consists of 80 out of 400 medium-capitalization range securities from the S&P MidCap 400 Index with the lowest realized volatility over the past 12 months.

The S&P 500® Low Volatility Index consists of the 100 stocks from the S&P 500® Index with the lowest realized volatility over the past 12 months.

The S&P 500® High Quality Rankings Index is designed to provide exposure to the constituents of the S&P 500 Index that are identified as stocks reflecting long-term growth and stability of a company’s earnings and dividends.

The Dynamic Large Cap Growth IntellidexSM Index seeks to provide capital appreciation while maintaining consistent stylistically accurate exposure. The Style Intellidexes apply a rigorous 10-factor style isolation process to objectively segregate companies into their appropriate investment style and size universe.

The S&P 500® Index is an unmanaged index considered representative of the US stock market.

The NASDAQ US BuyBack Achievers™ Index is designed to track the performance of companies that meet the requirements to be classified as BuyBack Achievers™. The NASDAQ US BuyBack Achievers Index is comprised of US securities issued by corporations that have effected a net reduction in shares outstanding of 5% or more in the trailing 12 months.

PMI (formerly Purchasing Managers Index), a commonly cited indictor of the manufacturing sectors’ economic health, is calculated by the Institute of Supply Management.

The S&P 500® High Beta Index consists of the 100 stocks from the S&P 500® Index with the highest sensitivity to market movements, or beta, over the past 12 months. Beta is a measure of relative risk and is the rate of change of a security’s price.

The Dynamic Large Cap Value IntellidexSM Index is designed to provide capital appreciation while maintaining consistent stylistically accurate exposure. The Style Intellidexes apply a rigorous 10-factor style isolation process to objectively segregate companies into their appropriate investment style and size universe.

The Dorsey Wright Technical LeadersTM Index includes approximately 100 US companies from a broad mid- and large-capitalization universe. The Index is constructed pursuant to Dorsey, Wright & Associates, LLC’s proprietary methodology, which takes into account, among other factors, the performance of each of the approximately 1,000 largest companies in the eligible universe as compared to a benchmark index, and the relative performance of industry sectors and sub-sectors.

The FTSE RAFI US 1000 Index is designed to track the performance of the largest US equities, selected based on the following four fundamental measures of firm size: book value, cash flow, sales and dividends. The 1,000 equities with the highest fundamental strength are weighted by their fundamental scores.

The FTSE Low Beta Equal Weight Index is designed to capture stocks exhibiting low beta and high profitability.

The S&P SmallCap 600 Low Volatility Index consists of 120 out of 600 small-capitalization range securities from the S&P SmallCap 600® Index with the lowest realized volatility over the past 12 months.

The S&P MidCap 400 Index is an unmanaged index considered representative of mid-sized US companies.

The Dynamic Market IntellidexSM Index seeks to identify and select companies from the US marketplace with superior risk-return profiles.

The S&P 500® Dynamic VEQTOR Index provides investors with broad equity market exposure with an implied volatility hedge by dynamically allocating between equity, volatility and cash. The index allows investors to receive exposure to the equity and volatility of the S&P 500 Index in a dynamic framework.

The S&P 500® Enhanced Value Index is designed to measure the performance of the top 100 stocks in the S&P 500® with attractive valuations based on “value scores” calculated using three fundamental measures: book value-to-price, earnings-to-price, and sales-to-price.

The S&P SmallCap 600® Index is a market-value weighted index that consists of 600 small-cap US stocks chosen for market size, liquidity and industry group representation.

The FTSE RAFI US 1500 Small-Mid Index is designed to track the performance of small and medium-sized US companies. Companies are selected based on the following four fundamental measures of size: book value, cash flow, sales and dividends. Each of the equities with a fundamental weight ranking of 1,001 to 2,500 is then selected and assigned a weight equal to its fundamental weight.

The Dorsey Wright SmallCap Technical Leaders™ Index includes securities pursuant to a Dorsey, Wright & Associates, LLC proprietary selection methodology that is designed to identify companies that demonstrate powerful relative strength characteristics. Approximately 200 companies are selected for inclusion from a small-cap universe of approximately 2,000 of the smallest US companies selected from a broader set of 3,000 companies.

JP Morgan Global Composite PMI is an index that provides an overview of global economic activity based on monthly surveys of over 16,000 purchasing executives in 32 countries. Together the countries measured account for an estimated 86% of global gross domestic product (GDP). Questions are asked about real events and are not opinion based. Data are presented in the form of diffusion indices, where an index reading above 50.0 indicates an increase in the variable since the previous month and below 50.0 a decrease.

The Russell 1000® Growth Index, a trademark/service mark of the Frank Russell Co.®, is an unmanaged index considered representative of large-cap growth stocks.

The Russell 1000® Value Index, a trademark/service mark of the Frank Russell Co.®, is an unmanaged index considered representative of large-cap value stocks.

The Russell 1000® Equal Weight Index captures the risk and return performance of an equal weight investment strategy for U.S. large-cap stocks. The Russell 1000® Equal Weight Index is a trademark/service mark of the Frank Russell Co.

The BarCap US Corporate High Yield Index – 10-Year Treasury Spread Index, which displays the yield spread between a portfolio of high yield notes as defined by Barclays Capital and the 10-year Treasury yield, measures risk in the high yield market.

The Spot Market Price Index is a measure of price movements of 22 sensitive basic commodities whose markets are presumed to be among the first to be influenced by changes in economic conditions. As such, it serves as one early indication of impending changes in business activity.

PowerShares® is a registered trademark of Invesco PowerShares Capital Management LLC, investment adviser. Invesco PowerShares Capital Management LLC (Invesco PowerShares) and Invesco Distributors, Inc., ETF distributor, are indirect, wholly owned subsidiaries of Invesco Ltd.

There are risks involved with investing in ETFs, including possible loss of money. Index-based ETFs are not actively managed. Actively managed ETFs do not necessarily seek to replicate the performance of a specified index. Both index-based and actively managed ETFs are subject to risks similar to stocks, including those related to short selling and margin maintenance. Ordinary brokerage commissions apply. The Fund’s return may not match the return of the Index.

Shares are not individually redeemable and owners of the Shares may acquire those Shares from the Fund and tender those Shares for redemption to the Fund in Creation Unit aggregations only, typically consisting of 50,000, 75,000, 100,000 or 200,000 Shares.

All data provided by Invesco unless otherwise noted.

Before investing, investors should carefully read the prospectus/summary prospectus and carefully consider the investment objectives, risks, charges and expenses. For this and more complete information about the Fund, call 800 893 0903 or visit invescopowershares.com for the prospectus/summary prospectus.

Invesco Distributors, Inc. is the US distributor for Invesco Ltd.’s retail products and collective trust funds. Invesco Advisers, Inc. and other affiliated investment advisers mentioned provide investment advisory services and do not sell securities. Invesco Unit Investment Trusts are distributed by the sponsor, Invesco Capital Markets, Inc., and broker-dealers, including Invesco Distributors, Inc. PowerShares® is a registered trademark of Invesco PowerShares Capital Management LLC (Invesco PowerShares). Each entity is an indirect, wholly owned subsidiary of Invesco Ltd.

©2016 Invesco Ltd. All rights reserved.

A tale of two markets: Dividend, low volatility and quality factors earn top spots in Q1 2016 by Invesco Blog