Alternative investment options available to most investors present challenges and opportunities. Until recently, retail investors had limited access to alternative strategies and therefore may not be very familiar with these types of investments and how they can add value. They are increasingly popular, with assets in liquid alternative funds growing from around $50 billion in 2006 to more than $300 billion in 2015. What often gets lost when investors are sorting out all these distinctions is the reason they turned to alternatives in the first place. A better understanding of the role of alternatives in today’s economic environment — and in tomorrow’s — can help guide investors’ decisions as they weigh their options in the alternatives space.

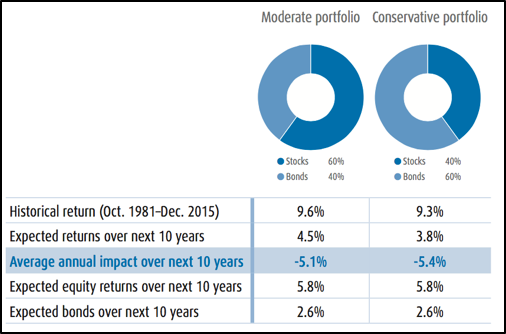

As we move further away from the Great Recession, the traditional 60/40 portfolio faces headwinds. This much-used paradigm allocates 60 percent of a portfolio to equities and 40 percent to bonds, balancing over the long term the growth (and higher risk) associated with equities with the stability (and lower risk) associated with bonds. Yet a significant assumption within the 60/40 paradigm — historically strong bond returns with low volatility — is no longer realistic with low bond yields in the current environment. We expect that even moderately risky balanced portfolios should expect more than a four percent decrease in returns over the next 10 years compared to what a 60/40 portfolio delivered in the last 35 years.

Investors need to find a way to adapt, as doing nothing may result in missing one’s diversification objectives. Assuming lower returns, greater risk or reduced liquidity are unsatisfactory options; a plan to find new sources of return should involve choosing from a spectrum of alternative options, noting these should provide either a higher return for the same amount of risk or the same return for a lower amount of risk.

To meet these diversification challenges, investors will need to distinguish liquid alternative strategies that rely on new market exposure, such as volatility and frontier markets, and those that rely on manager skill, such as market neutral, 130/30, long/short equity and macro strategies. Here it is important to note that many “new market exposures” may already appear in investors’ portfolios via REITs and commodities. The difficulty of finding truly new exposures, then, encourages a longer look at active management.

Our research indicates best practice may be to compile a complementary blend of active alternative managers specializing in different strategies, thus creating a multi-alternative fund. Manager selection in the alternatives space is arguably more difficult than in traditional long-only strategies. As evidence of this, we have found the dispersion of returns among several categories within the alternative space is greater than that of long-only funds. More importantly, we believe such dispersion among alternative managers suggests diverse sources of alpha: Alternative managers generate alpha using very different skill sets.

When conducting due diligence, it’s important to take sources of differentiation into account in regard to strategy, performance, risk management, organization and structure, among other items. To avoid diluting the contribution of an individual manager, we recommend a pool of six to 10 underlying managers while evenly distributing allocation to each one.

A multi-alternative fund can offer access to a concentrated portfolio of alternative managers, combining front-end due diligence, portfolio construction and management, and risk oversight, all performed by experienced, professional managers. The built-in diversification of multi-alternative approaches helps answer the fundamental question that began the search process in the first place: Is the portfolio diversified by manager and strategy? In short, an alternative allocation that combines expertise on manager research, asset allocation, portfolio construction and risk management should offer a flexible, portfolio-ready option.

You may view the full report by visiting http://bmogamviewpoints.com/.

All investments involve risk, including the possible loss of principal.

You should consider the Fund’s investment objectives, risks, charges, and expenses carefully before investing. For a prospectus and/or summary prospectus, which contain this and other information about the BMO Funds, call 1-800-236-3863. Please read it carefully before investing.

BMO Asset Management Corp. is the investment adviser to the BMO Funds. BMO Investment Distributors, LLC is the distributor. Member FINRA/SIPC.

Index definitions: S&P 500® is an unmanaged index of large-cap common stocks. Barclays U.S. Aggregate Bond Index is an index that covers the U.S. investment-grade fixed-rate bond market, including government and credit securities, agency mortgage pass through securities, asset-backed securities and commercial mortgage-based securities. To qualify for inclusion, a bond or security must have at least one year to final maturity and be rated Baa3 or better, dollar denominated, non-convertible, fixed rate and publicly issued.

Investments cannot be made in an index.

Additional definitions: Beta is a measure of a portfolio’s volatility. Statistically, beta is the covariance of the portfolio in relation to the market. A beta of 1.00 implies perfect historical correlation of movement with the market. A higher beta manager will rise and fall more rapidly than the market, whereas a lower beta manager will rise and fall slower. Alpha is the incremental return of a manager when the market is stationary. In other words, it is the extra return due to non-market factors. This risk-adjusted factor takes into account both the performance of the market as a whole and the volatility of the manager.

This is not intended to serve as a complete analysis of every material fact regarding any company, industry or security. The opinions expressed here reflect our judgment at this date and are subject to change. Information has been obtained from sources we consider to be reliable, but we cannot guarantee the accuracy. This presentation may contain forward-looking statements. “Forward-looking statements,” can be identified by the use of forward-looking terminology such as “may”, “should”, “expect”, “anticipate”, “outlook”, “project”, “estimate”, “intend”, “continue” or “believe” or the negatives thereof, or variations thereon, or other comparable terminology. Investors are cautioned not to place undue reliance on such statements, as actual results could differ materially due to various risks and uncertainties. This publication is prepared for general information only. This material does not constitute investment advice and is not intended as an endorsement of any specific investment. It does not have regard to the specific investment objectives, financial situation and the particular needs of any specific person who may receive this report. Investors should seek advice regarding the appropriateness of investing in any securities or investment strategies discussed or recommended in this report and should understand that statements regarding future prospects may not be realized. Investment involves risk. Market conditions and trends will fluctuate. The value of an investment as well as income associated with investments may rise or fall. Accordingly, investors may receive back less than originally invested.

Past performance is not necessarily a guide to future performance.

CTC | myCFO is a brand delivering family office services and investment advisory services through CTC myCFO, LLC, an investment adviser registered with the U.S. Securities and Exchange Commission, a Commodity Trading Advisor registered with the Commodity Futures Trading Commission (“CFTC”), and a member of the National Futures Association (“NFA”); trust, deposit and loan products and services through BMO Harris Bank N.A., a national bank with trust powers; and trust services through BMO Delaware Trust Company, a Delaware limited purpose trust company. BMO Delaware Trust Company offers trust services only, does not offer depository, financing or other banking products, and is not FDIC insured. Not all products and services are available in every state and/or location. Family Office Services are not fiduciary services and are not subject to the Investment Advisers Act of 1940 or the rules promulgated thereunder.

BMO Global Asset Management is the brand name for various affiliated entities of BMO Financial Group that provide investment management and trust and custody services. Certain of the products and services offered under the brand name BMO Global Asset Management are designed specifically for various categories of investors in a number of different countries and regions and may not be available to all investors. Products and services are only offered to such investors in those countries and regions in accordance with applicable laws and regulations. BMO Financial Group is a service mark of Bank of Montreal (BMO).

BMO Asset Management Corp., BMO Investment Distributors, LLC, BMO Private Bank, BMO Harris Bank N.A. and BMO Harris Financial Advisors, Inc. are affiliated companies. BMO Private Bank is a brand name used in the United States by BMO Harris Bank N.A. BMO Harris Financial Advisors, Inc. is a member FINRA/SIPC, an SEC registered investment adviser and offers advisory services and insurance products. Not all products and services are available in every state and/or location.

Investment products are: NOT FDIC INSURED — NOT BANK GUARANTEED — MAY LOSE VALUE.