The American economist Paul Samuelson famously noted that the stock market has “predicted nine out of the last five recessions! And its mistakes were beauties.”

With the major equity indices suffering peak-to-trough declines of nearly 20% from last summer through February, how should investors consider the latest bear move in the context of what is known about the economy?

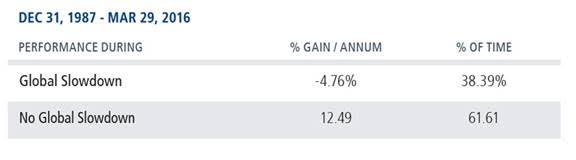

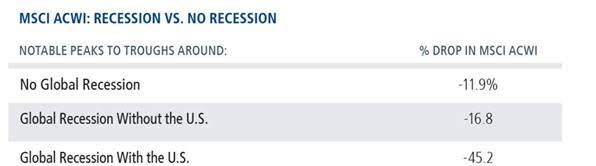

U.S. recession fears have ebbed in recent weeks and this is a critical development. Bear markets have been much shallower and shorter when they have not coincided with recessions. According to Ned Davis Research, since 1968, cyclical U.S. bear markets not associated with recessions have lasted an average of seven months with average declines of 19%—or about the magnitude of the past year’s correction. If my forecast that a U.S. recession is highly unlikely in 2016 proves correct, the near-term prospects for equities should be brighter.

Another reason why this non-recession judgment is critical relates to earnings. The U.S. has witnessed an earnings recession in the past year and this is the gist of the bear argument. After all, how can equities advance if earnings are not growing? Addressing this starts with understanding the cause of the earnings slowdown, which in my view amounts to weakness across global manufacturing including energy and commodities, sluggish economies overseas (such as China, Brazil) and the strong U.S. dollar. Fortuitously and through all of this, the U.S. consumer has performed just fine.

This economic setting of weakness abroad but respectable U.S. activity has happened before.

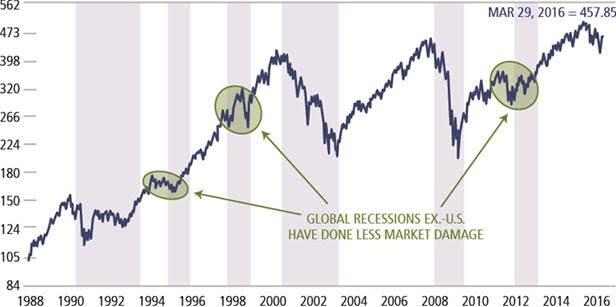

The chart below highlights the performance of the MSCI ACWI since 1988, with the gray shaded areas representing OECD-defined periods of global economic slowdown. The three circles highlighted in green are periods when the weakness was predominantly overseas and did not notably impact the U.S. economy. In those instances, the “global recession” excluded the U.S. and posed less of a threat to equities. In fact, the magnitude of those three prior declines appears much in line with the decline of the past year.

Figure 1. Performance of MSCI ACWI (Local Currency) During OECD-Defined Global SlowdownsDecember 1987 – March 2016, Daily Data (Log Scale)Shaded areas represent contractions based on peaks and troughs of OECD Reference

Source: Ned David Research Group, using data from MSCI, OECD, Main Economic Indicators (MEI), www.OECD.org

© Copyright 2016 Ned Davis Research, Inc. Further distribution prohibited without prior permission. All Rights Reserved. See NDR Disclaimer at www.ndr.com/copyright.html. For data vendor disclaimers refer to www.ndr.com/vendorinfo/.

Regardless of how our global long/short team slices the latest data, we don’t see it as supporting an apocalyptic view of the U.S. economy. To the contrary, the healing has been substantial and 2016 may ultimately be viewed as another global slowdown, excluding the U.S. And as the economies outside the U.S. eventually recover, this should restart the cycle of earnings growth.

This is why stronger global GDP is the necessary underpinning for equities to break sustainably higher.

Past performance is no guarantee of future results. The opinions referenced are as of the date of publication and are subject to change due to changes in the market or economic conditions and may not necessarily come to pass. Information contained herein is for informational purposes only and should not be considered investment advice.

The MSCI ACWI Index is a free float-adjusted market capitalization weighted index that is designed to measure the equity market performance of developed and emerging markets. OECD is the Organisation for Economic Co-operation and Development, a global organization with stated mission of promoting policiesthat will improve the economic and social well-being of people around the world.

101509 0416O C