A late March issue of The Economist proclaimed “profits are too high” and “America needs a giant dose of competition.” Funny. NIPA Corporate Profits figures released that week show The Economist’s plea for lower profits had already been fulfilled—and not just in the latest quarter.

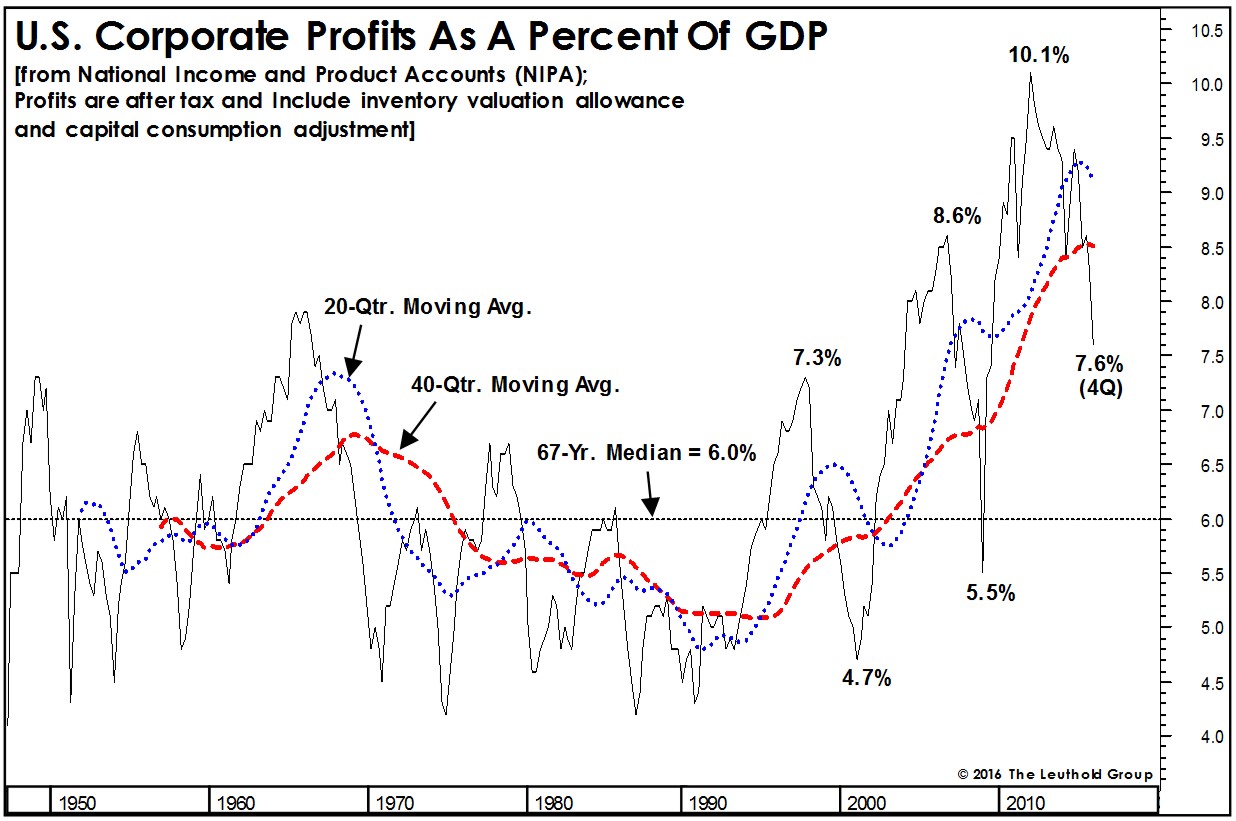

NIPA after-tax corporate profits (Chart 1) have declined at a 1% annualized rate in the 20 quarters ended last December—a period during which the unemployment rate dropped from 9.3% to 5.0%. From this perspective, labor’s participation in the economic recovery certainly looks favorable relative to the return on capital. If today’s profit figures—which are now flat over the last five years—are “too high,” we wonder what levels The Economist editors might deem acceptable.

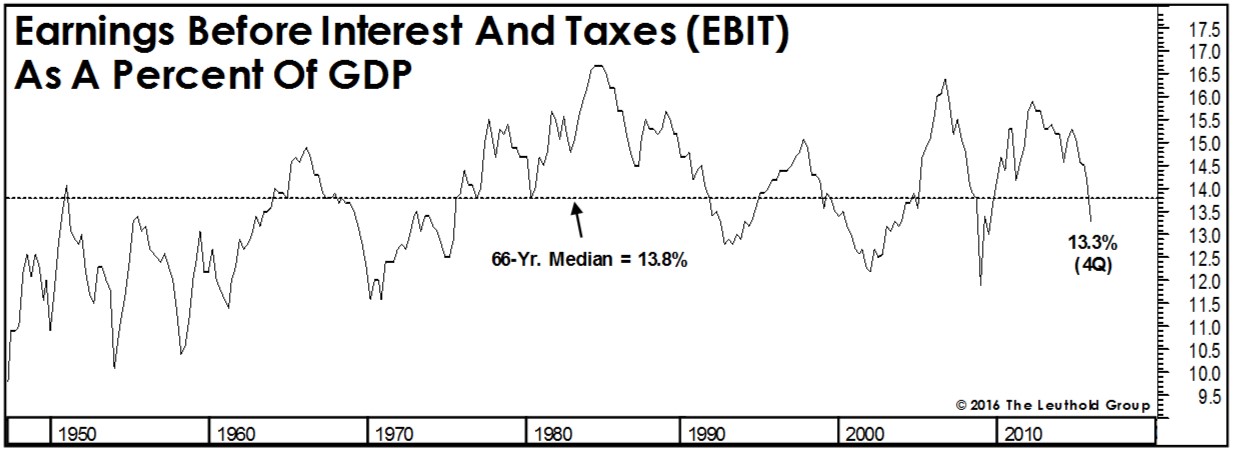

Admittedly, the Q4 net profit margin of 7.6% (while down considerably from its late-2011 peak) is still above its very-long term median of 6.0%. However, it’s critical to note that the latest quarter’s EBIT margin of 13.3% is already half a percent below its long-term median (1947-to-date, Chart 2). What could have possibly triggered mean-reversion? We suspect it was a “giant dose of competition,” particularly within the commodity-oriented sectors.

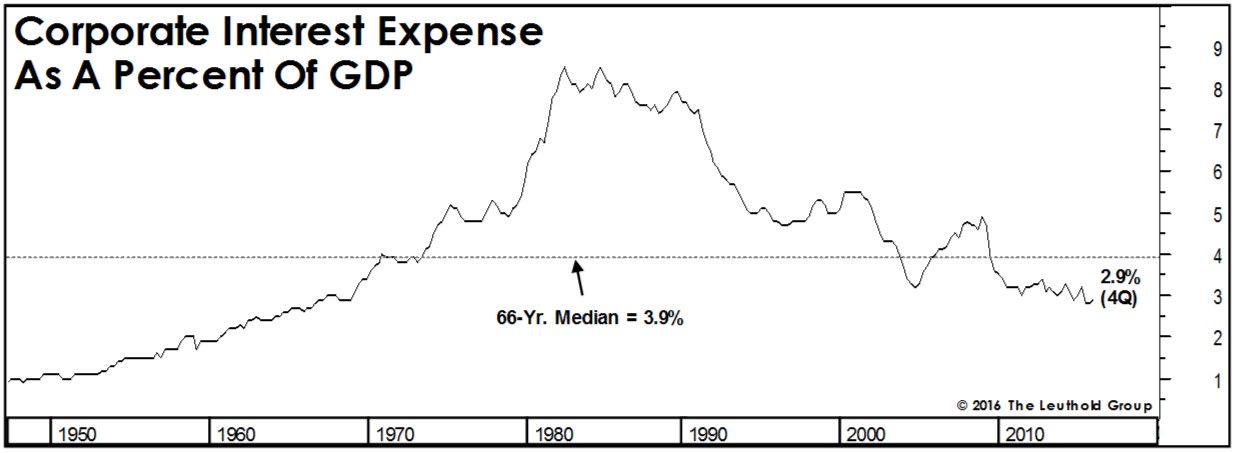

We’ve said this before but it bears repeating. Operating (EBIT) margins failed to reach previous cycle highs and came under pressure only three years into the current economic recovery—evidence that the gravitational forces of capitalism remain in effect. Net margins remain above average mainly because interest expense remains low (Chart 3)—a benefit that’s set to wear off following the last three years’ corporate borrowing binge.