U.S. Presidential Election Brings Key Economic Issues into Focus

The 2016 U.S. presidential election. has drawn more potential candidates, more controversy and perhaps more media coverage than any election in modern U.S. history. It also has been said that this year’s presidential contest is the most important of our time.* The same argument could be made from an economic perspective.

This campaign season has already been full of surprises. The unexpected popularity of Donald Trump and Bernie Sanders as potential presidential candidates has caused consternation and excitement. There is talk that the race for the Republican nomination won’t be decided until the Republican National Convention in Cleveland, OH, later this summer. Some even speculate that we could have a “brokered convention,” in which no single candidate has enough delegates at the start of the convention to lock up the nomination.

It still is too early to know who the nominees will be from the two major parties and the races for both nominations continue at a fever pitch. However, recent polls show that Hillary Clinton for the Democrats and Donald Trump for the Republicans are the likely presidential candidates.

As we consider the candidates and the upcoming election, we think it’s important to review the economic issues that the next occupant of the White House and the country will face in the coming years.

Demand, demographics and debt

Disappointing growth in domestic demand during the latest economic recovery has been the result of a variety of factors, including the country’s demographics, the debt overhang, residual effects from the global financial crisis and weak external demand. We think a few of these key issues have largely been ignored in the current presidential campaign.

Domestic demand is something that the government can directly impact. We believe the federal government will need to walk a fine line between productive investments and spending that boosts demand in the short term but hinders demand in the future. This is especially true given the federal government’s high level of debt, both on an absolute basis and relative to the size of the economy.

In the past, we have written about the benefits of a plan to upgrade and invest in the nation’s infrastructure. Not only would this boost demand in the short-term, but it also is likely to allow an increase in U.S. economic growth potential via an improvement in productivity growth. In addition, promoting investment in new technologies would foster new development and jobs in the high-technology industry. While government debt levels are high, we believe that officials could prioritize spending towards more productive areas.

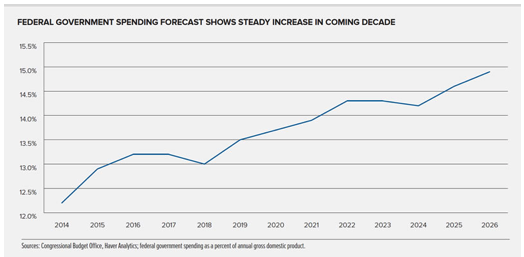

Demographics will be a key issue for the next administration. Many developed countries are experiencing population declines, while the U.S. population is expected to continue to grow. Even so, the aging U.S. population will put pressure on federal spending. The Congressional Budget Office estimates that “mandatory” federal spending, which is mostly comprised of entitlement spending, will rise by more than $1.5 trillion during the period 2016-2026. This increase equates to more than 1.5% of gross domestic product (GDP).

We believe government leaders and the next president will have several options, including:

- Cut entitlement spending, which would be politically difficult.

- Raise taxes, but current federal revenues are just over 18% of GDP and historically have not been able to sustainably get above 19% of GDP given the current tax structure.

- Cut so-called “discretionary” spending. But “discretionary” federal spending, which is everything outside of mandatory spending and interest, is at near-record lows relative to the size of the economy following recent budget cuts.

We think it is likely that the demographic pressures on the federal budget will be dealt with through a combination of entitlement cuts and tax increases, but the choices will not be easy.

Debt is a topic we have discussed in the past. Until the global financial crisis, private debt in the U.S. increased steadily for a number of years. While that debt has been reduced, it is still at relatively high historical levels, which is likely to be constraining economic activity. A high level of government debt also could have a dampening effect on private demand as consumers and businesses assume that taxes could rise in the future or benefits could be cut.

There is a perception that the wealthiest Americans continue to see strong gains in income as most U.S. households deal with debt in an environment in which incomes are relatively stagnant. This so-called “income gap” or “wealth gap” has been brought up by some presidential candidates during this campaign. The debt issue for these lower income households is unlikely to go away in the short-term and could be an overhang on domestic demand going forward.

What will the federal government do to control its growing debt loads? Will the government decide to implement policies that discourage increasing levels of private debt, or encourage a further buildup in private debt with promises to cancel portions of that debt? Answers to these questions could have important implications for individual consumers and the U.S. economy overall.

Bringing key issues into focus

We have identified three key issues but there are other important issues getting attention in the current campaign. However, the issues of demand, demographics and debt are central to the growth of the U.S. economy going forward and in some cases are not receiving the attention we think they deserve. They are among the critical topics for the next president and will be increasingly difficult to ignore.

* Source: Bloomberg Businessweek, “Why 2016 May Be the Most Important Election of Our Lifetime,” Nov. 5, 2015

Past performance is not a guarantee of future results. The opinions expressed in this article are those of Mr. Hamilton and are current through April 2016. These views are subject to change at any time based on market and other current conditions, and no forecasts can be guaranteed.

IVY INVESTMENTS℠ refers to the financial services offered by Ivy Distributors, Inc., a FINRA member broker dealer and the distributor of IVY FUNDS® mutual funds, and those financial services offered by its affiliates.

Before investing, investors should consider carefully the investment objectives, risks, charges and expenses of a mutual fund. This and other important information is contained in the prospectus and summary prospectus, which may be obtained at www.ivyinvestments.com or from a financial advisor. Read it carefully before investing.