Since we just finished tax time (or filed an extension to delay facing the reckoning until October), it is a good time to review your tax-advantaged retirement accounts. Whether you have five or 35 years until think you will retire, you will want to make progress to full retirement readiness.

Assuming you are saving 10% to 15% of your income (and receiving your full employer’s match, if any,) three of the largest impediments in investing retirement funds to reach your goals are:

- Not taking enough diversified risk to earn the returns necessary to build the needed retirement balances

- Investing with active managers for the wrong reasons

- Utilizing investment vehicles that charge high fees

As we discuss these points, we will need to differentiate funds in employer’s retirement plans (401k, 403b, 457) and individually directed accounts (IRA – Traditional and Roth, SEP, Simple.) Unless your employer’s retirement plan has a brokerage window, you can only invest in offerings provided by the employer. At times this is a positive feature since the employer or its plan advisor will have conducted significant due diligence into the funds best suited to employee needs.

In other cases, the investments offered are mainly affiliated with the plan’s advisor. These funds will need to be researched more carefully.

To the extent that you can direct your own investments, you have control over the points enumerated above. You can determine the asset classes, investment vehicles and individual securities to own. To the extent that you have balances in past employers’ retirement plans, you may wish to have them sent directly into a brokerage firm IRA (a rollover) so you can direct the investments as you wish.

Most individuals do not take on enough risk to grow their retirement balances at a fast enough rates. According to the Employee Benefit Research Institute1, at year-end 2013, only 44% of assets in retirement plans were invested in diversified equity funds. Another 23% was invested in “balanced funds” both target-date and traditional in nature. If half of these funds are invested in equities than that means there is a 55% allocation to diversified equities. Assuming that participants do not have large balances outside of their retirement accounts (and that 20% of them have loan balances on these accounts), it is likely that, overall, equity allocations are too low. Given that most employees today will be living into the 80s and may not retire until they are 70 or later, only those in their 60s should not have a high percentage of their portfolios in stocks.

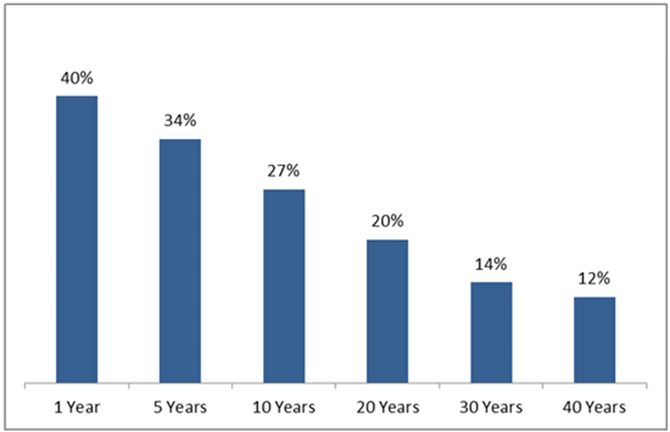

Even if their assets are properly allocated, individuals tend to overly rely upon actively managed funds, to their own peril. Vanguard2 determined the percentage of actively-managed equity funds that had higher returns than that of their benchmarks. As the graph below indicates, not only has a minority of these funds outperformed, the longer the timeframe studied, the more select the group became.

Percentage of Actively-Managed U.S. Equity Funds that Beat their Benchmarks

Source: Vanguard

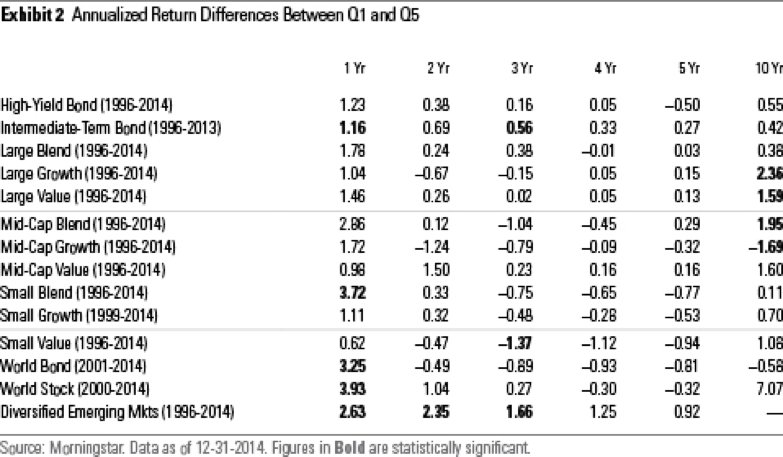

Morningstar3 recently studied persistence in outperformance by strategy category. They categorized funds by quintiles (Q1 through Q5) to see if the performance gap held in the next period of the same length. Assuming retirement investors wish to buy and hold funds for a long time, Morningstar found that for four and five year periods, outperformance in any category does not indicate outperformance for the next four or five year timeframe (see chart below.) After 10 year periods, there seems to be persistence in the Large Growth, Large Value and Mid-Cap Blend categories but not in any other. In fact, using their statistical test, you should invest in the worst Mid-Cap Growth funds over the past 10 years to enjoy good returns for the next ten.

Most investors should utilize index-based vehicles (such as exchange traded funds or ETFs) for exposure to various asset classes and their sectors. Although one will not have much cocktail party discussion about these investments, receiving returns close to that of the index is assured.

Finally, investors should stick with the advantages that indexed-based ETFs provide:

- Since there is no active management, the fund company has low investment personnel and research systems costs

- ETFs are created and redeemed using securities not cash. Thus, the ETF does not have to hold cash, which usually acts as a drag on performance, or sell securities and incur trading costs and possible capital gains, in case there are redemptions

- Indexed-based ETFs publish their holdings every day for complete transparency unlike mutual funds that only have to do so quarterly

- Since ETFs are traded throughout the market day on exchanges, they have complete liquidity

The combination of low management fees, reduced transaction costs and no recognition of capital gains can result in up to one percentage point advantage over index-based mutual funds and up to three percentage point advantages over actively managed mutual funds.

References

1 Jack VanDerhei, Sarah Holden, Luis Alonso, Steven Bass, and AnnMarie Pino. “401(k) Plan Asset Allocation, Account Balances, and Loan Activity in 2013.” EBRI Issue Brief, no. 408, and ICI Research Perspective, Vol. 20, no. 10 (December 2014).

2 Vanguard, “The Case for Indexing.” April 2012; S&P SPIVA 2012 Report, The Power of Passive Investing, Wiley, 2011

3 Alex Bryan, “Winners Often Flame out.” Morningstar Magazine, April/May 2016, 56-58.

© iSectors