Misbehavioral Finance: Countering Emotional Investment Decisions

Today’s concerns over the uneven state of the global economy, the direction of interest rates, and the price of oil – to name just a few current issues -- create a risk that emotions may unduly influence investment decisions. In our view, short-term market events and the emotions they can trigger should not drive investment choices. But how, exactly, can these factors be acknowledged while maintaining a proper focus on long-term goals and long-term investment strategies?

For financial professionals, we believe today’s environment demands a renewed focus on “softer” skills such as managing behavior. Here are five common behavioral biases we often see in the marketplace as well as potential solutions we often discuss with clients.

Unrealistic expectations: After years of stellar returns in stocks and bonds, investors’ expectations may exceed what today’s markets are capable of delivering. Assuming the continuation of recent trends may lead to decisions which work against an investor’s long-term goals. Potential solutions include (1) maintaining a long-term investment plan for both rising and falling markets, (2) focusing on goals instead of equity indexes or other market benchmarks, (3) asking questions in lieu of delivering unsolicited advice and matching the style of the client, and (4) not predicating one’s value on investment returns alone.

Loss aversion: The rule of thumb that “more risk may lead to more return” may not apply if an investor’s perception of gains and losses is asymmetric. Participants in one famous psychology experiment were shown to dislike losses 2 to 3 times more than the pleasure they derives from gains.1 For this reason, lowering overall portfolio risk may increase the likelihood of achieving objectives.

Potential solutions when loss aversion prevails include (1) reducing risk with more effective portfolio construction, (2) identifying the extent of loss aversion by probing investors’ willingness to risk short-term losses, and (3) testing and retesting the suitability of a given investment strategy.

Familiarity bias: Bias in favor of familiar investments is widespread and can result in excessive ownership of the stock of one’s own employer or of investments domiciled in one’s home country. Familiarity bias introduces at least three potential shortfalls: (1) missing out on attractive potential investment opportunities, (2) failing to avail one’s self of a fuller range of diversification possibilities, and (3) taking on unnecessary total risk.

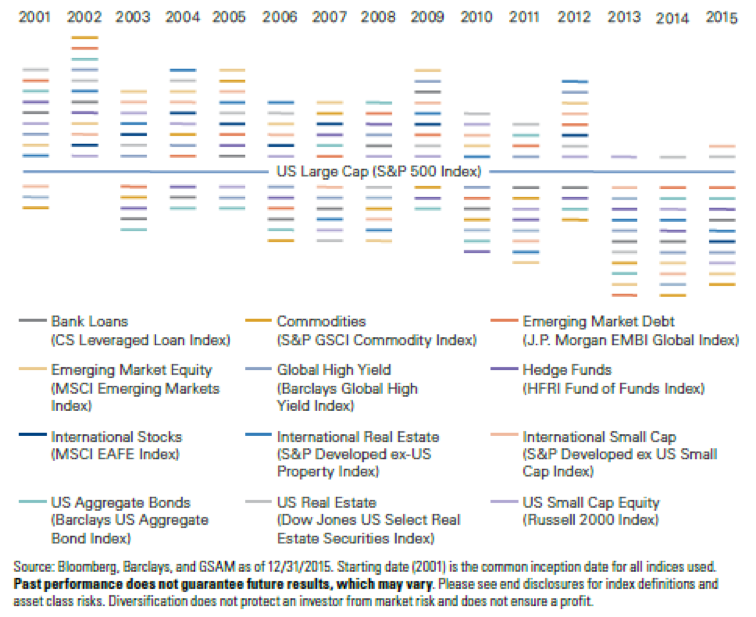

What to do about familiarity bias? (1) Consider incorporating a wider range of asset classes, since no trend (such as recent years’ outperformance in US equities) lasts forever (See Exhibit), (2) learn more about “core and diversifier” portfolio construction, to fine-tune one’s approach to sources of risk and return; and (3) Frame discussions of change around similarities to the familiar investment or reference point.

EXHIBIT: Diversifying Asset Classes in Context

Anchoring: Mental shortcuts by which investors assign unwarranted importance to a single reference point can lead to undesirable investment outcomes. A focus on regaining an investment’s recent performance high is one common example. Such “anchoring” can also occur when investors become too dependent on a single benchmark, for instance, the S&P 500, which we view as too risky (with its 15% annualized volatility over the long term2) for most investors to handle at the total portfolio level.

Respond to anchoring by (1) checking the relevance of reference points, (2) using diversified benchmarks which match risk tolerance levels, and (3) drilling down to the reasons an investor may be attached to a less-than-ideal reference point.

Overconfidence: Finance scholars Brad M. Barber and Terrance Odean have documented individual investors’ tendency to overestimate their abilities. Overconfidence can lead to owning undiversified portfolios, holding onto losing investments while selling winners, and engaging in excessive trading – all potentially leading investors to underperform long-term fund returns. We believe a clear and concise philosophy behind the construction of portfolios can help prevent high turnover, over-trading, and other destructive behaviors. Investment professionals may be especially well positioned to help clients develop a process which focuses on long-term, buy-and-hold investment strategies, and seek to build a well-constructed portfolio which blends core and diversifying asset classes.

Consider responding to overconfidence by (1) ensuring an investment process and philosophy to reduce excessive trading and other destructive behaviors, (2) conducting regular self-assessment and (3) conducting postmortems of important investment decisions.

Views are as of 2/1/2016 and subject to change in the future.

Risk Considerations

Commodities may be subject to greater volatility than investments in traditional securities.

Equity securities are more volatile than bonds and subject to greater risks. Small and mid-sized company stocks involve greater risks than those customarily associated with larger companies.

An investment in real estate securities is subject to greater price volatility and the special risks associated with direct ownership of real estate.

International securities entail special risks such as currency, political, economic, and market risks.

Emerging markets securities may be less liquid and more volatile and are subject to a number of additional risks, including but not limited to currency fluctuations and political instability.

High yield, lower-rated securities involve greater price volatility and present greater credit risks than higher-rated fixed income securities.

Exhibit notes

High yield is represented by the Barclays Global High Yield Index. The Barclays Global High Yield Index provides a broad-based measure of the global high-yield fixed income market. US aggregate bonds are represented by the Barclays Aggregate Bond. The Barclays Aggregate Bond Index represents an unmanaged diversified portfolio of fixed income securities, including U.S. Treasuries, investment-grade corporate bonds, and mortgage backed and asset-backed securities.

Bank loans are represented by the Credit Suisse Leveraged Loan Index. The Credit Suisse Leveraged Loan Index tracks the investable leveraged loan market by representing tradable, senior-secured, US-dollar denominated, noninvestment-grade loans.

Large cap value index is represented by the Russell 1000 Value index. The Russell 1000 Value Index is an unmanaged index of common stock prices that measures the performance of the large-cap value segment of the US equity universe. The peer group for yields is the Morningstar Large Value peer group.

Emerging market debt is represented by the JPM EMBI Global Composite. The JPM EMBI is an unmanaged index tracking foreign currency denominated debt instruments of 31 emerging markets.

US real estate is represented by the FTSE NAREIT COMPOSITE Index. The FTSE NAREIT COMPOSITE Index includes both price and income returns of all publicly traded REITS (equity, mortgage, and hybrid.)

Index Definitions

The Barclays U.S. Aggregate Index represents securities that are SEC-registered, taxable, and dollar denominated. The index covers the U.S. investment grade fixed rate bond market, with index components for government and corporate securities, mortgage pass-through securities, and asset-backed securities. These major sectors are subdivided into more specific indices that are calculated and reported on a regular basis.

The S&P 500 Index is an index based on the prices of the securities of 500 different companies, 400 of which are industrial, 40 of which are utility, 40 of which are financial and 20 of which are transportation companies.

The MSCI EAFE Index (unhedged) is a market capitalization-weighted composite of securities in 21 developed markets. The Index is unmanaged and the figures for the Index do not include any deduction for fees, expenses or taxes. It is not possible to invest directly in an unmanaged index.

The Dow Jones U.S. Select Real Estate Securities Index (RESI) represents equity real estate investment trusts (REITs) and real estate operating companies (REOCs) traded in the U.S.

The Barclays U.S. Corporate High Yield Bond Index is a total return performance benchmark for fixed income securities having a maximum quality rating of Ba1 (as determined by Moody’s Investors Service). The Index is unmanaged and the figures for the Index do not include any deduction for fees, expenses or taxes. It is not possible to invest directly in an unmanaged index.

The Barclays Global High-Yield Index provides a broad-based measure of the global high-yield fixed income markets. The Global High-Yield Index represents the union of the U.S. High-Yield, Pan-European High-Yield, U.S. Emerging Markets High-Yield, and Pan-European Emerging Markets High-Yield Indices.

The Barclays EM (USD) Aggregate Index is a hard currency Emerging Markets debt benchmark that includes fixed and floating-rate US dollar-denominated debt issued from sovereign, quasi-sovereign, and corporate EM issuers.

The Credit Suisse Leveraged Loan Index is an unmanaged index of U.S. leveraged loans.

Past performance does not guarantee future results, which may vary. The value of investments and the income derived from investments will fluctuate and can go down as well as up. A loss of principal may occur.

The indices are unmanaged and the figures for the Index reflect the reinvestment of dividends, but do not include any deduction for fees, expenses or taxes. It is not possible to invest directly in an unmanaged index. The figures for the index reflect the reinvestment of dividends but do not reflect the deduction of any taxes, fees or expenses which would reduce returns.

This material is for informational purposes only. It is not an offer or solicitation to buy or sell any securities.

This information discusses general market activity, industry or sector trends, or other broad-based economic, market or political conditions and should not be construed as research or investment advice. This material has been prepared by GSAM and is not financial research nor a product of Goldman Sachs Global Investment Research (GIR). It was not prepared in compliance with applicable provisions of law designed to promote the independence of financial analysis and is not subject to a prohibition on trading following the distribution of financial research. The views and opinions expressed may differ from those of Goldman Sachs Global Investment Research or other departments or divisions of Goldman Sachs and its affiliates. Investors are urged to consult with their financial advisors before buying or selling any securities. This information may not be current and GSAM has no obligation to provide any updates or changes.

Although certain information has been obtained from sources believed to be reliable, we do not guarantee its accuracy, completeness or fairness. We have relied upon and assumed without independent verification, the accuracy and completeness of all information available from public sources.

Goldman, Sachs & Co., member FINRA.

Views and opinions expressed are for informational purposes only and do not constitute a recommendation by GSAM to buy, sell, or hold any security. Views and opinions are current as of the date of this page and may be subject to change, they should not be construed as investment advice.

© 2016 Goldman Sachs. All rights reserved. Date of first use: March 31, 2016

Compliance code: 40615-OTU-222487

1 Kahneman and Tversky, “Choices, Values and Frames,” American Psychologist, Vol 39 (4), April 1984.

2 As measured by the historical volatility of the S&P 500 Index over the two decades ending Dec. 31, 2015.