Are Republican presidents better for markets, or are Democrats?

Should the outcome of the election change our investment plans? Particularly during campaign season, these questions concern many investors, as presidential candidates offer plans for taxes, regulation and fiscal spending goals.

Yet, research suggests that the impact of presidents and parties on the markets is too complex and varied to be a compass for long-term investment advice.

That may be surprising to some. After all, we know that policies, presidents and even candidates can move markets at times. One example: When Hillary Clinton tweeted about pharmaceutical drug pricing practices last fall, stock prices for some biotech companies responded with a swift decline in the days that followed. Additionally, the passage of Obamacare has impacted the insurance and healthcare sectors.

Policies do matter for markets. But the examples above had narrow influence, affecting specific stocks or sectors. Both examples involved Democrats, but one case hurt some stocks, while the other case boosted some. Can we find tangible evidence that markets at large have tended to be better or worse under specific parties or candidates?

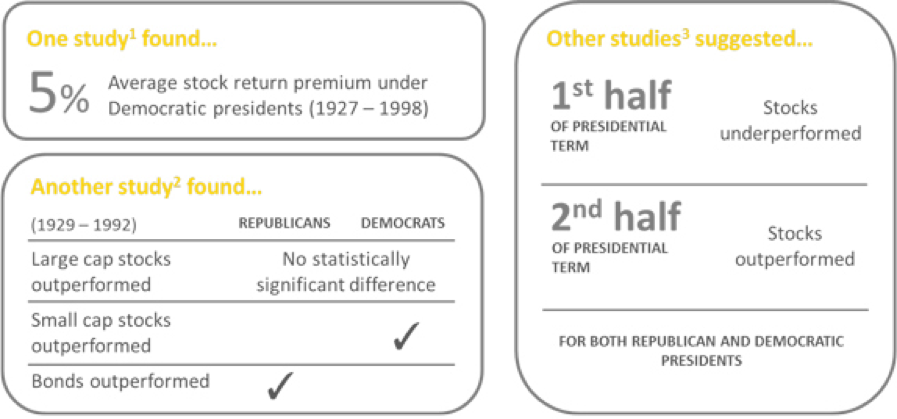

Researchers have come to contradictory verdicts about presidents and stock markets.1 Some studies find that Democratic presidents have been better for stock returns. Others suggest that only small cap stocks have outperformed under Democrats, while large caps have fared about the same in both types of administrations and bonds outperformed under Republicans.2 Other studies observe that no matter which party was at the helm, stock prices fell in the first half of a presidency and rose in the second half.3

Importantly, these patterns have depended a lot on the data set used. For instance, the study that found that small caps outperformed under Democrats from 1929-1992 also noted that the pattern disappeared if using data from 1937-1992. For studies that observed a trend for better stock performance in last two years of a presidential term, the patterns depended on an average market cycle of four years. Yet, here we are in year seven of a bull market.

Presidents and Markets: What effects have presidents and parties had on returns?

Sources: 1. Santa-Clara, P. and Valkanov, R. (2003), The Presidential Puzzle: Political Cycles and the Stock Market. The Journal of Finance, 58: 1841–1872. 2. Hensel, C. and Ziemba, W. (1995), United States Investment Returns during Democratic and Republican Administrations, 1928-1993. Financial Analysts Journal, March-April 1995: 61-69. 3. Gartner, M. and Wellershoff, K. (1995), Is There an Election Cycle in American Stock Returns? International Review of Economics & Finance, Volume 4, Issue 4: 387-410. Investing entails risk including possible loss of principal. Past performance is not indicative of future results.

We believe that context matters far more than a simple Republican-or-Democrat outcome. One complication to finding an airtight relationship between parties and markets is that the core positions of both parties evolve over time. A Republican or Democrat of 50 years ago could look very different from the same party profile today.

Presidents also face different degrees of power in office. For instance, many scholars consider the current Congress to be the most divided and partisan since the Civil War. That means the president, facing majorities of the other party in both houses, has less power relative to Congress. Only a same-party trifecta—meaning a president, Senate and House led by the same party—could evade the current gridlock and increase the current power of the president when it comes to passing legislation.

Perhaps the biggest factor is that the issues facing politicians are wildly different from one decade to another. Trade agreements, foreign exchange trends, wars, technology, demographics—all of these conditions change over time, and offer up unique challenges and opportunities to whichever party occupies the Oval Office. In the end, can we say that the impact of the White House is really stronger than all of the other inputs to the economy? Probably not.

As we see it, presidents and politics are just one of many inputs that can move markets. Just about anything can introduce short-term volatility to stocks, from bad weather, to oil prices, to interest rate changes in other countries—and yes, even comments by presidents or candidates. Indeed, some expect market volatility to subside as the candidate for each party becomes clearer. When it comes to the long-term effects of particular policies on sectors and individual stocks, that’s an issue for active managers. But when it comes to trying to position long-term portfolios around politics, the relationship of parties and presidents is generally too weak to be a useful input.

1 Santa-Clara, P. and Valkanov, R. (2003), The Presidential Puzzle: Political Cycles and the Stock Market. The Journal of Finance, 58: 1841–1872.

2 Hensel, C. and Ziemba, W. (1995). United States Investment Returns during Democratic and Republican Administrations, 1928-1993. Financial Analysts Journal, March-April 1995: 61-69.

3 Gartner, M. and Wellershoff, K. (1995). Is There an Election Cycle in American Stock Returns? International Review of Economics & Finance, Volume 4, Issue 4: 387-410. Nickles, M. (2004) Presidential Elections and Stock Market Cycles. Graziadio Business Review, Volume 7, Issue 3.

This material is provided for informational purposes only and nothing herein constitutes investment, legal, accounting or tax advice, or a recommendation to buy, sell or hold a security. Information is obtained from sources deemed reliable, but there is no representation or warranty as to its accuracy, completeness or reliability. All information is current as of the date of this material and is subject to change without notice. Third-party economic or market estimates discussed herein may or may not be realized and no opinion or representation is being given regarding such estimates. Any views or opinions expressed may not reflect those of the firm as a whole. Information presented may include estimates, outlooks, projections and other “forward looking statements.” Due to a variety of factors, actual events may differ significantly from those presented. Neuberger Berman products and services may not be available in all jurisdictions or to all client types. Investing entails risks, including possible loss of principal. Diversification does not guarantee profit or protect against loss in declining markets. Unless otherwise indicated returns shown reflect reinvestment of dividends and distributions. Indexes are unmanaged and are not available for direct investment. Past performance is no guarantee of future results.

Neuberger Berman LLC is a registered investment adviser. The “Neuberger Berman” name and logo are registered service marks of Neuberger Berman Group LLC.

Certain products and services may not be available in all jurisdictions or to all client types.

© 2009-2016 Neuberger Berman LLC. | All rights reserved