In today’s low interest rate environment, the Invesco Municipal Bond team believes there are still attractive yields in the municipal bond market, making the asset class a compelling stand-alone opportunity or addition to a broader investment portfolio.

Municipal bonds’ tax-exempt status certainly enhances their relative appeal, but even before taxes, these bonds have the potential to offer attractive opportunities for income and capital appreciation. Municipal bonds may also serve as diversifiers in an overall investment portfolio because of their low correlation to other major asset classes. Below are four key reasons why investors may want to consider municipal bonds.

1. Tax advantages

New laws, as well as tax provisions that expired at the end of 2013, have led to larger tax bills for many high-income earners. Some of the significant changes to tax law include: a top marginal rate of 39.6%, up from 35%; a 20% tax on long-term capital gains and dividends, up from 15%; and a new 3.8% tax on investment income — which municipal income is exempt from.

We believe that these higher tax rates increase the incentive for taxpayers to consider municipal bonds as they are exempt from federal income tax and can be exempt from state and local income taxes.

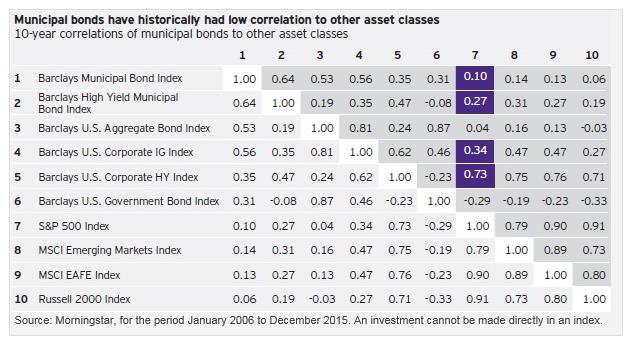

2. Diversification potential

In our view, diversification can potentially increase opportunities for growth and reduce overall portfolio volatility. Because municipal bonds historically have had very low correlation to other asset classes, including equities and Treasuries, they can be effective portfolio diversifiers. Of course, diversification does not ensure a profit or eliminate the risk of loss.

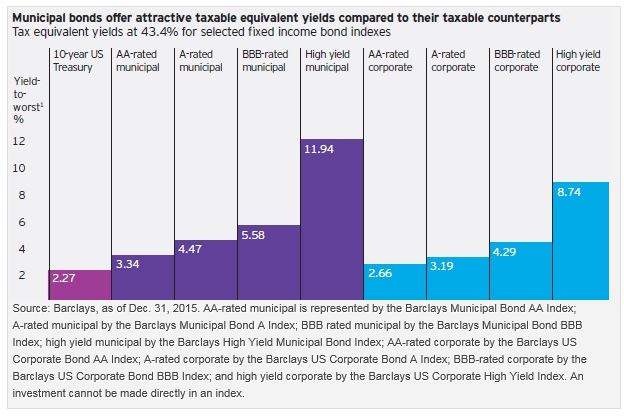

3. Attractive yields on a before- and after-tax basis

The sell-off of 2013 resulted in lower bond prices and higher yields, creating an opportunity for long-term investors with a focus on after-tax income. As shown below, yields on municipal bonds, particularly high yield municipals, are attractive relative to other fixed income asset classes, even on a before-tax basis.

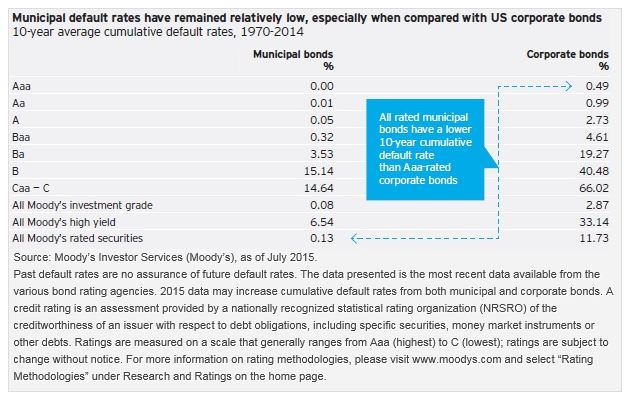

4. Relatively lower default risk

Contrary to popular belief, the vast majority of municipal bond issuers remain creditworthy, and municipal default rates have remained relatively low, especially when compared with US corporate bonds.

As shown in the chart below, when the credit structure decreases, the odds of a default rise. However, the percentages are much higher for investment grade corporates than for municipals. Since 1970, there has never been an AAA-rated municipal bond default. Similarly, in the same time frame, only 0.01% of munis have defaulted with an AA-rating. By contrast, AA-rated corporate bonds have had a nearly 1% default rate since 1970.2

Talk to your advisor

While municipal bonds are rightly renowned for generating tax-exempt income, there are several other reasons to consider them as well, including their potential for producing relatively attractive yields, low default risk and diversification benefits. Talk to your advisor to get more information about the benefits and risks of using municipal bonds in your portfolio.

For more information about investing in municipal bonds, read Invesco’s Investible Ideas piece, “Municipal bonds: More than just tax-exempt income.”

1 (39.6% federal tax rate + 3.8% NIIT). 2013 top marginal tax rate for single taxpayers with more than $400,000 in taxable income or couples with $450,000 or more. NIIT is the Net Investment Income Tax of 3.8% on investment income for single taxpayers with more than $200,000 in taxable income or couples with $250,000 or more.

2 Source: Moody’s “US Municipal Bond Defaults and Recoveries, 1970-2014” as of May 2015

Important information

Income may be subject to state and local taxes and to the alternative minimum tax.

Diversification does not guarantee a profit or eliminate the risk of loss.

The opinions expressed are those of the portfolio managers, are based on current market conditions and are subject to change without notice. There is no guarantee the outlooks mentioned will come to pass. These opinions may differ from those of other Invesco investment professionals.

Municipal securities are subject to the risk that legislative or economic conditions could affect an issuer’s ability to make payments of principal and/or interest. Municipal bonds are issued by state and local government agencies to finance public projects and services. They typically pay interest that is not subject to federal regular income tax or state and local income taxes in their state of issuance. Because of their tax benefits, municipal bonds usually offer lower pretax yields than similar taxable bonds. Unlike bonds, senior secured loans are secured by collateral but are typically made to below investment grade companies. The risk of default may be higher when compared with loans or bonds issued for investment grade companies, but senior secured loans typically have a lower risk when compared with non-investment grade or high yield bonds. High yield bonds invest in non-investment grade bonds and are therefore subject to greater volatility than investment grade bonds. Securities that are in the medium- and lower-grade categories generally offer higher yields than are offered by higher-grade securities of similar maturity, but they also generally involve more volatility and greater risks, such as greater credit, market, liquidity, management and regulatory risks. Fixed income investments are subject to credit risk of the issuer and the effects of changing interest rates. Interest rate risk refers to the risk that bond prices generally fall as interest rates rise and vice versa. An issuer may be unable to meet interest and/or principal payments, thereby causing its instruments to decrease in value and lowering the issuer’s credit rating.

The Barclays U.S. Corporate High Yield Index is an unmanaged index considered representative of fixed-rate, non-investment grade debt. The Barclays High Yield Municipal Bond Index is an unmanaged index considered representative of non-investment grade bonds. The Barclays Municipal Bond Index is an unmanaged index considered representative of the tax-exempt bond market. The Barclays U.S. Corporate Investment Grade Index is an unmanaged index considered representative of publicly issued, fixed-rate, nonconvertible, investment grade debt securities. The Barclays U.S. Aggregate Bond Index is an unmanaged index considered representative of the US investment grade, fixed-rate bond market. The S&P 500 Index is an unmanaged index considered representative of the US stock market. The MSCI EAFE Index is an unmanaged index considered representative of stocks of Europe, Australasia and the Far East. The index is computed using the net return, which withholds applicable taxes for nonresident investors. The MSCI Emerging Markets Index is an unmanaged index considered representative of stocks of developing countries. The index is computed using the net return, which withholds applicable taxes for nonresident investors. The Russell 2000 Index is an unmanaged index considered representative of small-cap stocks, and is a trademark/service mark of the Frank Russell Co. Russell® is a trademark of the Frank Russell Co. The Barclays U.S. Government Bond Index is an index that measures the performance of all public US government obligations with remaining maturities of one year or more.

Past performance is not a guarantee of future results.

An investment cannot be made directly in an index.

Correlation indicates the degree to which two investments have historically moved in the same direction and magnitude.

Yield-to-worst is the lowest potential yield that can be received on a bond without the issuer actually defaulting.

©2016 Morningstar, Inc. All rights reserved. The information contained herein is proprietary to Morningstar and/or its content providers. It may not be copied or distributed and is not warranted to be accurate, complete or timely. Neither Morningstar nor its content providers are responsible for any damages or losses arising from any use of this information.

The information provided is for educational purposes only and does not constitute a recommendation of the suitability of any investment strategy for a particular investor. Invesco does not provide tax advice. The tax information contained herein is general and is not exhaustive by nature. Federal and state tax laws are complex and constantly changing. Investors should always consult their own legal or tax professional for information concerning their individual situation. The opinions expressed are those of the authors, are based on current market conditions and are subject to change without notice. These opinions may differ from those of other Invesco investment professionals.

All data provided by Invesco unless otherwise noted.

Invesco Distributors, Inc. is the US distributor for Invesco Ltd.’s retail products and collective trust funds. Invesco Advisers, Inc. and other affiliated investment advisers mentioned provide investment advisory services and do not sell securities. Invesco Unit Investment Trusts are distributed by the sponsor, Invesco Capital Markets, Inc., and broker-dealers, including Invesco Distributors, Inc. PowerShares® is a registered trademark of Invesco PowerShares Capital Management LLC (Invesco PowerShares). Each entity is an indirect, wholly owned subsidiary of Invesco Ltd.

©2016 Invesco Ltd. All rights reserved.

Four reasons to consider investing in municipal bonds by Invesco