Key Points

▪ Despite recent negative headlines from the retail sector, we believe consumer spending remains on track and should be a tailwind for the broader U.S. economy.

▪ Market volatility is likely to persist, but we think equity prices will grind higher as corporate earnings results improve.

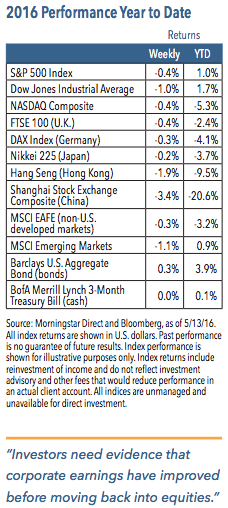

The S&P 500 Index fell 0.4% last week, although it remains in positive territory for the year.1 The retail sector was a heavy focus last week as earnings results were broadly disappointing. The cancellation of the Staples/Office Depot merger also caused sentiment to sour on retailers. The rally in the U.S. dollar continued, as U.S. growth continues to outpace most of the rest of the world.1 Oil prices rallied while most industrial metals were lower.1

The Consumer Sector Should Help Drive Economic Growth

Disappointing first quarter earnings results from many large retailers have been causing some to question the strength of consumer spending. Economic data from last week, however, showed some positives for the consumer. April’s retail sales figures showed a 1.3% increase, notably higher than the consensus expectations of 0.8%.2 Likewise, the latest reading of the University of Michigan’s Index of Consumer Sentiment rose from 89 in April to 95.8 in May, its highest level in eleven months.3

In our view, these readings help reinforce the notion that the consumer sector remains quite healthy despite some earnings struggles. A possible slowdown in employment growth should be counter-balanced by rising wages. We believe consumer spending remains an important tailwind for the broader economy, which we expect should continue to grow close to 2%.

Reasons for Optimism...and Pessimism

Rather than our usual weekly economic and investment themes, this week we offer a list of reasons to be optimistic about the economy and equities, as well as a list of reasons to be pessimistic, adapted from some thoughts by J.P. Morgan Research. On the positive side, we would include 1) Equity valuations do not appear to be stretched, 2) Earnings improvements should start to materialize in the coming quarters, 3) The oil rout appears to be over, 4) Investor sentiment may be overly bearish and 5) Corporate tax reform prospects for next year appear bright.

In contrast, the negatives include 1) Earnings remain shaky and improvements are probably necessary for equities to experience a sustained move higher, 2) Investors may be overly complacent about Federal Reserve rate hikes, 3) Global growth is likely to remain anemic, 4) The U.S. political backdrop is highly uncertain and 5) Regulatory scrutiny over mergers and acquisitions appears to be growing, which may suppress this equity-friendly activity.

Despite a Solid Outlook, Sentiment Remains Depressed

A back-and-forth in markets has been the theme that has dominated 2016. Markets pulled back over the past several weeks after rallying from mid-February through mid-April. In retrospect, it shouldn’t be surprising that this rally faded. Investor sentiment has remained weak and investors are defensively positioned, continuing to hold large amounts of cash. This suggests the recent rally was a result of short covering and a sense that recession and deflation risks were fading, rather than coming about through growing optimism. In other words, investors may believe that conditions aren’t as dire as they thought early in the year, but they are hardly optimistic about earnings and economic growth prospects.

Overall, we think the positives will win out over the negatives, but near-term concerns mean risk assets are unlikely to move up in a straight line. The current risks and hurdles include next month’s referendum on whether the U.K. will leave the European Union, the prospect of a more aggressive than expected pace of Fed rate hikes and the possibility of another downturn in oil prices. We think the odds are better than not that markets will weather these potential storms. But given the fragile state of sentiment, it wouldn’t take much for equities to experience another sell-off or consolidation.

Ultimately, we think investors need evidence that corporate earnings have recovered before they will feel more comfortable moving back into equity investments. We expect this evidence will materialize over the coming quarters, which is why we believe equities will outpace bonds and cash over the next six to twelve months. But investors will be slow to embrace good news and there is still ample reason for caution. As such, we think volatility will remain elevated.

1 Source: Morningstar Direct, as of 5/13/16

2 Source: Commerce Department

3 Source: University of Michigan

The S&P 500 Index is a capitalization-weighted index of 500 stocks designed to measure the performance of the broad domestic economy. The Dow Jones Industrial Average is a price-weighted average of 30 significant stocks traded on the New York Stock Exchange and the Nasdaq. The Nasdaq Composite is a stock market index of the common stocks and similar securities listed on the NASDAQ stock market. FTSE 100 Index is a capitalization-weighted index of the 100 most highly capitalized companies traded on the London Stock Exchange. Deutsche Borse AG German Stock Index (DAX Index) is a total return index of 30 selected German blue chip stocks traded on the Frankfurt Stock Exchange. Nikkei 225 Index is a price-weighted average of 225 top-rated Japanese companies listed in the First Section of the Tokyo Stock Exchange. Hong Kong Hang Seng Index is a free-float capitalization-weighted index of selection of companies from the Stock Exchange of Hong Kong. Shanghai Stock Exchange Composite is a capitalization-weighted index that tracks the daily price performance of all A-shares and B-shares listed on the Shanghai Stock Exchange. MSCI EAFE Index is a free float-adjusted market capitalization weighted index designed to measure developed market equity performance, excluding the U.S. and Canada. The MSCI Emerging Markets Index is a free float-adjusted market capitalization index that is designed to measure equity market performance of emerging markets. Barclays U.S. Aggregate Bond Index covers the U.S. investment grade fixed rate bond market. The BofA Merrill Lynch 3-Month U.S. Treasury Bill Index is an unmanaged market index of U.S. Treasury securities maturing in 90 days that assumes reinvestment of all income.

RISKS AND OTHER IMPORTANT CONSIDERATIONS

The views and opinions expressed are for informational and educational purposes only as of the date of writing and may change at any time based on market or other conditions and may not come to pass. This material is not intended to be relied upon as investment advice or recommendations, does not constitute a solicitation to buy or sell securities and should not be considered specific legal, investment or tax advice. The information provided does not take into account the specific objectives, financial situation, or particular needs of any specific person. All investments carry a certain degree of risk and there is no assurance that an investment will provide positive performance over any period of time. Equity investments are subject to market risk or the risk that stocks will decline in response to such factors as adverse company news or industry developments or a general economic decline. Debt or fixed income securities are subject to market risk, credit risk, interest rate risk, call risk, tax risk, political and economic risk, and income risk. As interest rates rise, bond prices fall. Noninvestment-grade bonds involve heightened credit risk, liquidity risk, and potential for default. Foreign investing involves additional risks, including currency fluctuation, political and economic instability, lack of liquidity and differing legal and accounting standards. These risks are magnified in emerging markets. Past performance is no guarantee of future results.

CFA® and Chartered Financial Analyst® are registered trademarks owned by CFA Institute.

Nuveen Asset Management, LLC is a registered investment adviser and an affiliate of Nuveen Investments, Inc.

©2016 Nuveen Investments, Inc. All rights reserved.