Drug companies make convenient villains, but is painting an entire industry with a broad brush the best way to encourage innovation and advance health care?

In this political season, drug companies have become a convenient whipping boy. Congress called some firms on the carpet to defend their drug pricing practices, while some presidential candidates have suggested that drug companies are greedy profiteers. Their commonly suggested remedies include calls for Medicare to negotiate directly with drug makers; for consumers to see caps on out-of-pocket drug costs; for loosening regulations to allow drug re-importation (notably from Canada); and for eliminating "pay-for-delay" deals between branded drug and generic drug makers. Election year promises are sometimes at odds with reality. Do these policy positions present an improvement to our health care system?

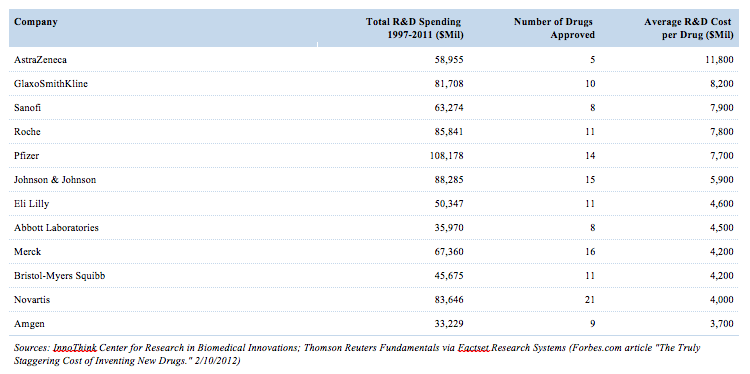

The costs of bringing a new drug onto market

According to academic literature, bringing a new drug to market costs between $1 billion and $3 billion.1 A report published by Tufts Center for the Study of Drug Development puts the cost at $2.6 billion. Part of this reflects the increasing complexity of clinical trials, part reflects the difficulty of targeting diseases, and part reflects the cost of failed clinical trials. Failed studies tend to advance science but represent a real cost of doing business for drug companies.

Existing market systems motivate payers to keep prices low while striving to maintain universal access

266 million Americans get access to prescription medications through their health plans via drug programs administered by a pharmacy benefit manager (PBM). The plans range from commercial health to government and military employee plans. PBMs also administer programs for Medicare Part D. Some presidential candidates suggest the public good is better served by allowing Medicare to negotiate directly with drug manufacturers. Currently, health insurance companies offer Medicare Supplementary coverage to the public at pricing that must be competitive in order to gain subscribers. The health insurer in turn engages a PBM to administer the drug program under a contract to acquire drugs at the least expensive rates possible. They do this via administration of a formulary — a health plan's list of preferred drugs. Products not on the formulary generally experience weaker sales. Often, when multiple medications exist to treat the same condition, drug companies compete for inclusion on a formulary. With the current system, the free market is working twice as hard to get the best prices for consumers.

Will direct negotiations between drug companies and Medicare/government improve drug pricing without compromising access?

Probably not. European countries certainly pay less, but price negotiations sometimes fail, causing drug manufacturers to refuse to sell into a market. For example, even though Germany is Europe's biggest health care market, Novo Nordisk stopped marketing its insulin drug Tresiba there because it regarded the price offered by German officials as insignificant relative to the value offered. In the United Kingdom, patients served by the National Health Service have no access to Humira, the world's best-selling immunosuppressant. In general, formularies in countries with national health care have fewer options for patients. Will the government be able to procure drugs at prices better than PBMs can? It is possible though far from guaranteed. Can a government mandate achieve lower prices than organizations competing in a free market? Given Medicare already operates in a competitive environment, savings, if any, would mostly come from restricting access.

Will caps on out-of-pocket costs put pressure on drug prices?

Not likely. Caps on out-of-pocket costs are more likely to impact insurance premiums than drug prices. If a drug offers legitimate therapeutic value, then the manufacturer has an incentive to realize its economic value. If the insurer is paying more of the cost, unable to pass it on to the patient through copays, it will be forced to increase premiums. Insurance companies are simply not in the business of losing capital.

Should the US Food and Drug Administration allow drug re-importation to give Americans access to cheaper medicines?

One consistent observation and criticism of US health care has been the difference between drug prices in the US and many other developed countries. US providers pay market prices. Foreign governments negotiate a single price on behalf of their citizens, so market pricing is impaired. Assuming assured quality, re-importation would certainly impact US prices but risks higher future drug costs for exporting countries. We must face some realities. Since drug companies seek to maximize the value of innovation, regardless of political jurisdiction, they would undoubtedly change their approach to selling into foreign markets. Foreign prices could increase, or products might be sold at discounts so long as they were not available for export. Also, for jurisdictions that provide drug subsidies, drug exports represent a direct loss of their tax dollars to foreigners. Might we see offsetting legislation in other countries denying export as a response to this move? Consider Canada: can a country of 35.2 million effectively negotiate drug prices for its southern neighbor, which has a population of 318.9 million, without impacting health care costs for its own population?

Should "pay-for-delay" be prohibited to speed generic competition?

"Pay-for-delay" describes when a branded drug maker pays a generic drug maker to defer generic entry once a drug goes off patent. Governments enter into a social contract with companies by allowing them patent exclusivity on their research. Once that patent expires, the rights to the innovation fall to the public domain. Pay-for-delay inhibits competition and deserves antitrust scrutiny from the Federal Trade Commission (FTC). Indeed, a court settlement in 2013 paved the way for FTC review. With antitrust weapons in hand, it appears pay-for-delay will see further challenges by existing authorities.

Concluding thoughts

Drug companies make convenient villains. Of course, bad actors exist, such as Turing Pharmaceuticals whose buy-and-hike strategy oozes greed while giving short shrift to advancing science and serving patients. Yet, how does Medivation, recently called to testify before Congress over price hikes of prostate cancer drug Xtandi, fit the picture of a mischief-maker? It brought to market an innovative drug in high demand while failing to report a profit until 2014. Certainly there have been troublemakers, but painting the industry with a broad brush hardly constitutes a good way to encourage innovation and advance health care.

Copyright 2016 Saturna Capital Corporation and/or its affiliates. All rights reserved. Vol. 10 · No. 3

Saturna Capital publishes From The Yardarm Market Commentary & Analysis monthly. Saturna Capital does not share subscriber information with third parties.

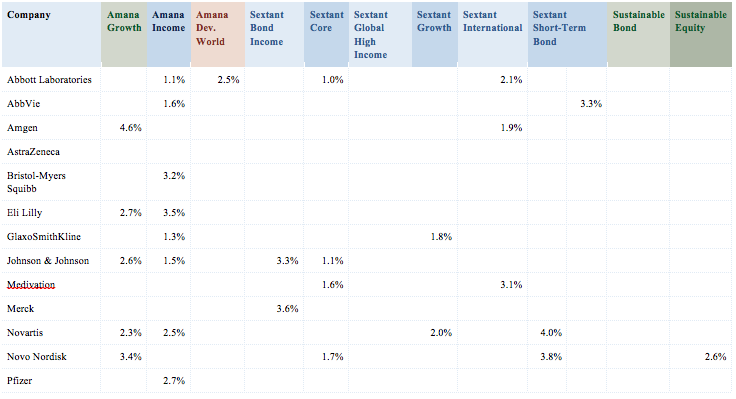

Ownership of Companies Mentioned (as of 3/31/2016)

Ownership of Companies Mentioned (as of 3/31/2016)

Security weightings are shown as a percentage of total net assets.

Amana Participation and Idaho-Tax-Exempt did not own any securities of the companies mentioned.

Footnotes:

¹ Mullin, Rick. Cost to Develop New Pharmaceutical Drug Now Exceeds $2.5B, Scientific American, November 24, 2014. http://www.scientificamerican.com/article/cost-to-develop-new-pharmaceutical-drug-now-exceeds-2-5b/

Important Disclaimers and Disclosures

This material is for general information only and is not a research report or commentary on any investment products offered by Saturna Capital. This material should not be construed as an offer to sell or the solicitation of an offer to buy any security in any jurisdiction where such an offer or solicitation would be illegal. To the extent that it includes references to securities, those references do not constitute a recommendation to buy, sell or hold such security, and the information may not be current. Accounts managed by Saturna Capital may or may not hold the securities discussed in this material.

We do not provide tax, accounting, or legal advice to our clients, and all investors are advised to consult with their tax, accounting, or legal advisers regarding any potential investment. Investors should not assume that investments in the securities and/or sectors described were or will be profitable. This document is prepared based on information Saturna Capital deems reliable; however, Saturna Capital does not warrant the accuracy or completeness of the information. Investors should consult with a financial advisor prior to making an investment decision. The views and information discussed in this commentary are at specific point in time, are subject to change, and may not reflect the views of the firm as a whole.

All material presented in this publication, unless specifically indicated otherwise, is under copyright to Saturna. No part of this publication may be altered in any way, copied, or distributed without the prior express written permission of Saturna.