KEY TAKEAWAYS

- The S&P 500 celebrated the one-year anniversary of its all-time high on May 21, 2016.

- One-year periods without new highs during bull markets have often preceded strong stock market gains.

- We continue to expect a volatile, range-bound stock market for the balance of 2016.

The one-year anniversary of the S&P 500’s all-time high took place on May 21, 2016. Stocks have largely been spinning their wheels for the past year. The S&P 500 has failed to return to its May 21, 2015, record high for 12 months. Stocks have actually been spinning their wheels for even longer, considering the S&P 500 is at the same level as it was on November 18, 2014—an 18-month stretch. This week we take a look at what the stock market’s lackluster performance since the last record high might mean for the current bull market, now the second longest since 1950.

DID THIS BULL MARKET ALREADY END?

So does this long period without a new high mean the aging bull market, now more than seven years old, is about to end? Before we answer that question, keep in mind that it is possible that the current bull market actually ended on May 21, 2015. If the S&P 500 does not reach another new high before dropping 20% from that high (which would leave the S&P 500 at 1704), then the bull market will have ended in May 2015. We don’t know yet, but it’s possible that the bull market will not have celebrated its seventh birthday on March 9, 2016 (don’t we all wish we could undo previous birthdays). We see the potential for more new highs before the next bear arrives; but just in case, now we know what’s at stake.

WHERE DO WE GO FROM HERE?

So what does this drought mean? For perspective, going back to 1955 and including the most recent period, the S&P 500 has gone a full calendar year without a new high 13 times (no new highs were made from 1929 through mid-1954 so there is no need to look further back). Six of those new high droughts took place during bull markets, six were during bear markets, and we’ll call the current one a question mark [Figure 1]. The droughts lasted as little as 259 trading days in 1994–95 (for reference, one calendar year is 252 trading days), or as long as nearly 1900 trading days during the late 1970s and early 1980s.

Looking at all of those 12 previous instances when the S&P 500 didn’t make a new high for a full year, subsequent near-term returns were lackluster. Three and six months out, the average and median gain for the S&P 500 was very close to flat. But going out a full year, average and median performance was close to the long-term average annual gain for stocks at about 9% [Figure 2].

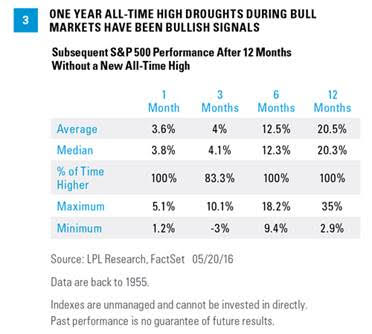

Isolating the bull markets reveals that one-year periods without a new high have actually been very good times to buy stocks. As shown in Figure 3, those instances were followed by 6- and 12-month gains of 12.5% and 20.5%, on average, and were higher in all six periods both 6 and 12 months later. The most recent bull market example, February 1995, preceded double-digit gains over the subsequent 3- and 6-month periods and a tremendous 35% gain over the following 12 months as the tech boom got underway. Stocks also produced very strong gains after the August 1987–88 all-time high drought, as that bull market continued through July 1990.

The most recent two occurrences—March 2001 and October 2008—did not take place during bull markets and are certainly not comforting. Six months after those one-year droughts, stocks dropped by 9.7% and 13.0%, respectively. Looking at all six bear market periods, the average performance over the following 6 and 12 months was -11.5%, and -1.8%, respectively, and stocks were lower 6 months laterin all instances. Like virtually any stock market analysis, the key is to avoid the bear markets—clearly easier said than done.

THE CLOSER THE BETTER

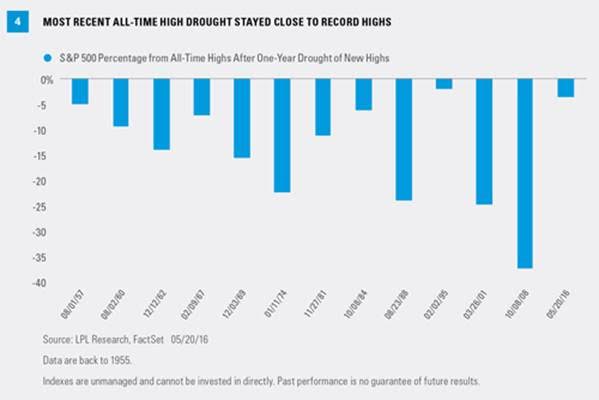

What stands out about this most recent drought without a new high is how close the S&P 500 is to its record high after one year. In fact, the current 3.7% shortfall from the new high is the second closest to a new high among all 13 new high droughts [Figure 4], with only 1994–95 closer (1.9% off the high). That mid-1990s drought took place right ahead of the tech boom and spectacular late 1990s rally.

The two other most recent instances that the S&P 500 was within 10% of a new high after a year without one were in the late 1960s and mid-1980s. Both of those times saw continued gains and an eventual resumption of the bull markets. In other words, if a full year goes by without a new high but the S&P 500 is close to its highs, the odds have historically been good that stocks will set a new high and continue higher before the bull market ends.

Also note that the maximum drawdown over the past year, at 14%, compares favorably to these other one-year periods, with only the 1959–60 and 1994–95 periods experiencing smaller maximum drawdowns.

THEN AND NOW

So now that we’ve gone another year without a new stock market high, does that make stocks a better opportunity? Below we address that question, comparing the investment environment today to one year ago for some perspective [Figure 5].

· Market performance. A year ago stocks were up 13% over the trailing one-year period, compared with the S&P 500’s drop over the past 12 months of 3.7%. Oil is lower (but has stabilized), interest rates (based on the 10-year Treasury) are down 0.34%, and the yield curve is flatter. The defensive utilities sector has topped the sector rankings, while a year ago the leaders were more cyclical (biotech-driven healthcare, technology, and consumer discretionary). Stocks have been adjusting to a weaker global growth environment for a year and we have not seen much evidence to date that things will get much better—or worse—in the near term.

· Valuations.The better stock market performance and stronger earnings growth in the year leading up to May 21, 2015, left stocks more expensive a year ago than they are today based on price-to-earnings ratios (PE). Despite a 0.6–0.7 point reduction in the S&P 500 PE, we still see stocks as slightly overvalued based on long-term averages, but fair when factoring in low interest rates. The good news is earnings are poised to improve in the second half of 2016.

· Sentiment.Sentiment has been subdued for much of this bull market, but has deteriorated over the past 12 months. Fewer bulls (based on the American Association of Individual Investors [AAII] survey) and lower consumer confidence readings are consistent with market-based indicators cited above that show slightly weaker market conditions.

· Economic growth. A year ago the U.S. economy was coming off of a year-over-year increase in gross domestic product of 2.9% for Q1 2015, followed by 2.7% for the second quarter of 2015, better than today’s level (2.0%) based on first quarter 2016 data. Other key measures of U.S. economic growth—the Institute for Supply Management (ISM) indexes—have weakened slightly. Generally, the economic growth outlook today is a bit softer than a year ago.

· Employment. The U.S. economy produced similar job growth over the past year as it did the year prior. The economy added slightly fewer jobs in the year ending May 2016 compared to the year ending May 2015, but job gains were sufficient to push the unemployment rate down to 5.0% from 5.4%. The job market has also been strong enough to help push wage growth high enough to get the Federal Reserve’s (Fed) attention, as evidenced by the minutes from the latest Federal Open Market Committee (FOMC) meeting, released on May 18, 2016.

· Inflation. That wage growth over the past year has shown up in inflation measures such as the Consumer Price Index (CPI). The good news is the economy and labor markets are healthy enough to create some inflation. The bad news is fears about Fed rate hikes may continue to create market volatility.

· Fed policy. A year ago, market expectations for the federal funds rate at the end of 2016 were about 50 basis points higher (0.5%) than they are today, based on fed fund futures, reflecting a slightly weaker macroeconomic environment. That translates to market expectations taking about two rate hikes off the table over the last year. The Fed’s expectations have contracted more rapidly, falling 1.0% based on the Fed’s most recent “dot plots,” but still exceed market expectations for the end of the year by about two rate hikes.

All in all, based on our assessment of the current market environment, we see no reason to change our expectation for a volatile, range-bound stock market for the balance of 2016, with an eventual full-year 2016 return in the mid-single-digits.*

Thank you to Ryan Detrick for his contributions to this report.

* Historically since WWII, the average annual gain on stocks has been 7-9%. Thus, our forecast is roughly in-line with average stock market growth. We forecast a mid-single digit gain, including dividends, for U.S. stocks in 2016 as measured by the S&P 500. This gain is derived from earnings per share (EPS) for S&P 500 companies assuming mid-to-high-single-digit earnings gains, and a largely stable price-to-earnings ratio. Earnings gains are supported by our expectation of improved global economic growth and stable profit margins in 2016.

IMPORTANT DISCLOSURES

The opinions voiced in this material are for general information only and are not intended to provide specific advice or recommendations for any individual. To determine which investment(s) may be appropriate for you, consult your financial advisor prior to investing. All performance referenced is historical and is no guarantee of future results.

The economic forecasts set forth in the presentation may not develop as predicted and there can be no guarantee that strategies promoted will be successful.

Investing in stock includes numerous specific risks including: the fluctuation of dividend, loss of principal, and potential liquidity of the investment in a falling market.

All investing involves risk including loss of principal.

The PE ratio (price-to-earnings ratio) is a measure of the price paid for a share relative to the annual net income or profit earned by the firm per share. It is a financial ratio used for valuation: a higher PE ratio means that investors are paying more for each unit of net income, so the stock is more expensive compared to one with lower PE ratio.

The AAII Investor Sentiment Survey measures the percentage of individual investors who are bullish, bearish, and neutral on the stock market for the next six months; individuals are polled from the ranks of the AAII membership on a weekly basis. Only one vote per member is accepted in each weekly voting period. For more information, go to:http://www.aaii.com/sentimentsurvey.

INDEX DESCRIPTIONS

The Standard & Poor’s 500 Index is a capitalization-weighted index of 500 stocks designed to measure performance of the broad domestic economy through changes in the aggregate market value of 500 stocks representing all major industries.

The Institute for Supply Management (ISM) Index is based on surveys of more than 300 manufacturing firms by the Institute for Supply Management. The ISM Manufacturing Index monitors employment, production inventories, new orders, and supplier deliveries. A composite diffusion index is created that monitors conditions in national manufacturing based on the data from these surveys.

The Consumer Price Index (CPI) is a measure of the average change over time in the prices paid by urban consumers for a market basket of consumer goods and services.