With the first four months of the year in the books, I’d like to take a moment to break down the performance of alternatives thus far.

As readers of Invesco’s blog may already know, I am a big believer of investing “by looking through the windshield, rather than looking in the rearview mirror,” meaning investors need to invest in anticipation of what lies ahead, rather than based on past market performance. Furthermore, I continue to believe that after several years of equities generating returns well above their long-term average — while at the same time experiencing volatility well below the historical average — we are due to see lower returns and higher volatility return to the markets.

Looking at the markets this year, it clearly has been a tale of two periods. The first period occurred in the first six weeks of the year, as the S&P 500 Index sold off by over 10% and volatility, as measured by the CBOE Volatility Index (VIX), spiked to over 28. In the second period, from mid-February through April 30, 2016, the S&P 500 shot up about 13%, while volatility fell back to about 15. Clearly the first six weeks can be characterized as a “risk off” environment in which investors fled risk assets, while the second period was a “risk on” period in which investors flocked back to risk assets.

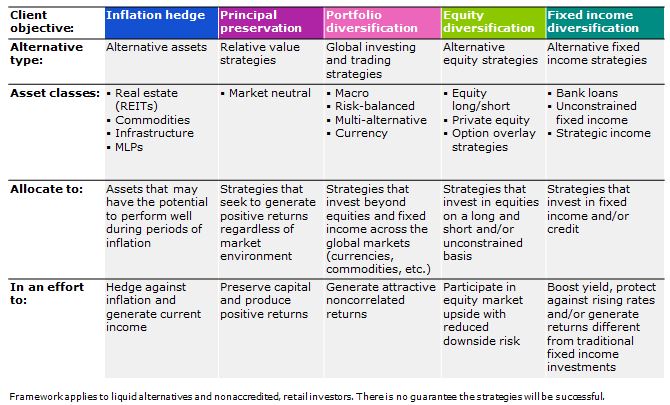

Before I delve into the details, I wanted to note that I’m evaluating performance across the various categories used in Invesco’s alternatives framework, as shown below.

Let’s now examine the performance of alternatives against the backdrop of today’s volatile markets:

Alternative assets — Alternative assets are long-only investments in assets other than stocks and bonds. Common examples include REITs (real estate investment trusts), infrastructure, MLPs (master limited partnerships) and commodities. Alternative assets are considered “risk assets,” and experienced negative performance during the first six weeks of the year. However, they have rebounded strongly since that time and, on a year-to-date basis, have outperformed equities.1

Invesco offers a full range of alternative asset funds: Invesco Global Real Estate Fund, Invesco Global Real Estate Income Fund, Invesco Real Estate Fund, Invesco Global Infrastructure Fund, Invesco MLP Fund and Invesco Balanced-Risk Commodity Strategy Fund.

Relative value strategies — For this category, I’m going to focus on market neutral strategies, which can potentially generate return regardless of the general movements of the markets. As discussed in my last blog, I believe market neutral strategies can be valuable for investors, especially given my belief about equities facing lower returns and higher volatility. Market neutral as a category is more or less flat for the year.2 With that said, market neutral is a strategy whose performance is highly dependent on a manager’s stock selection. Because of this, results can vary widely from manager to manager.

Invesco offers two market neutral funds: Invesco All Cap Market Neutral Fund and Invesco Global Market Neutral Fund.

Global investing and trading strategies — For this category, I’m going to focus on global macro strategies, which invest on a long and short basis across the global equity, fixed income, currency, commodity and derivative markets. I believe global macro funds are attractive because of their ability to invest on an unconstrained, opportunistic basis. As a whole, this strategy3 is up slightly on a year-to-date basis. As with relative value, this strategy is also highly dependent on the manager, and performance varies widely from manager to manager.

Invesco offers two global macro funds: Invesco Global Targeted Returns Fund and Invesco Global Markets Strategy Fund.

Alternative equity strategies — For this category, I’m going to focus on long/short equity. This strategy combines both long and short equity positions in a portfolio, while typically being net long to stocks. I believe long/short equity is attractive because it has shown the ability to limit downside relative to equities, while retaining its ability to participate in a rising equity market.4 Funds following this strategy performed5 as I would have expected, outperforming equities during the “risk off” period when equities sold off and underperforming during the “risk on” period in which equities rebounded.

Invesco offers two long/short equity funds: Invesco Long/Short Equity Fund and Invesco Macro Long/Short Fund.

Alternative fixed income strategies — For this category, I want to look at two different strategies, unconstrained bond and bank loans:

Unconstrained bond funds — They have the freedom to invest on a long and short basis across the entire fixed income universe. Conceptually, I believe unconstrained bond funds are attractive because of their ability to invest opportunistically and ability to positon the portfolio, attempting to take advantage of a rising interest rate environment. This strategy is highly manager dependent, and performance can vary widely by manager. As of April 30, 2016, this strategy6 has generated a positive return but trails the Barclays US Aggregate Bond Index.

Invesco Unconstrained Bond Fund is an example of this strategy.

Bank loans — This asset class consists of pools of senior secured loans made to non-investment grade companies. Bank loans are fully collateralized, reside at the top of the capital structure and can offer attractive yield, which is appealing to many investors in a low rate environment. As you would expect, performance of bank loans is often correlated with the current economic environment, as a favorable environment makes it more likely loans will be repaid, while a difficult environment can cause an increase in default risk. Given this characteristic, it’s not surprising that bank loans experienced negative performance during the “risk off” portion of the year, before rebounding strongly during the “risk on” period that followed. Bank loans are now up over 3%, according to the Morningstar Bank Loan category.

Invesco offers two bank loan mutual funds: Invesco Senior Loan Fund and Invesco Floating Rate Fund.

For more information about alternatives

1. To learn more about Invesco’s alternative strategies, please visit invesco.com/alternatives.

2. You can also read previous blogs from Walter Davis, and ask Walter your questions about alternatives with our Ask the Expert feature.

3. And, learn why it’s time to say goodbye 60/40 and to consider alternatives as more of your core.

1 Alternative assets represented by the FTSE NAREIT All Equity REIT Index and the Bloomberg Commodity Index. Equities represented by the S&P 500 Index. The FTSE NAREIT All Equity REIT Index is up 4.89% year-to-date through April 30, 2016, the Bloomberg Commodity Index is up 8.86% and the S&P 500 Index is up 1.74%.

2 As measured by the Credit Suisse Equity Market Neutral Index.

3 As measured by the HFRX Macro/CTA Index.

4 For example, in the bear market of 2008, the S&P 500 Index lost 37.00%, while the BarclayHedge Long/Short Index lost much less: 11.88%. In the up year of 2013, when the S&P 500 Index gained 32.39%, the BarclayHedge Long/Short Index participated in some of those gains, earning 13.85%.

5 As measured by the Morningstar Long/Short Equity category.

6 As measured by the Morningstar Nontraditional Bond category.

Important information

The CBOE Volatility Index® (VIX®) is a key measure of market expectations of near-term volatility conveyed by S&P 500 stock index option prices. VIX is the ticker symbol for the Chicago Board Options Exchange (CBOE) Volatility Index, which shows the market’s expectation of 30-day volatility.

The BarclayHedge Long/Short Index includes funds that employ a directional strategy involving equity-oriented investing on both the long and short sides of the market.

The Barclays US Aggregate Bond Index is an unmanaged index considered representative of the US investment grade, fixed-rate bond market.

The FTSE NAREIT All Equity REIT Index is an unmanaged index considered representative of US REITs.

The Bloomberg Commodity Index is an unmanaged index designed to be a highly liquid and diversified benchmark for the commodity future market.

The Credit Suisse Equity Market Neutral Index is an asset-weighted hedge fund index covering the equity market neutral sector.

The HFRX Macro/CTA Index is constructed using a UCITS III-compliant methodology that is based on defined and predetermined rules and objective criteria to select and rebalance components to maximize representation of the hedge fund universe.

The Morningstar Long/Short Equity category contains funds that will shift their exposure to long and short positions depending on their macro outlook or the opportunities they uncover through bottom-up research.

The Morningstar Nontraditional Bond category contains funds that pursue strategies divergent in one or more ways from conventional practice in the broader bond-fund universe.

The S&P 500 Index is an unmanaged index considered representative of the US stock market.

Past performance cannot guarantee future results. An investment cannot be made in an index.

Certain indexes reflect performance of hedge funds, not of retail investment strategies, and are used for illustrative purposes only solely as points of reference in evaluating alternative investment strategies.

Hedge funds are typically aggressively managed portfolios of investments for high net worth investors that use advanced investment strategies such as leverage, long, short and derivative positions with the goal of generating high returns (either in an absolute sense or over a specified market benchmark). Hedge fund managers have less restriction on their investment methodologies than mutual fund managers, and hedge funds are less regulated and therefore offer less investor protection than mutual funds. Mutual funds are more transparent with regard to disclosure of underlying holdings and have lower fees than hedge funds.

Short sales may cause an investor to repurchase a security at a higher price, causing a loss. As there is no limit on how much the price of the security can increase, exposure to potential loss is unlimited.

Most senior loans are made to corporations with below investment grade credit ratings and are subject to significant credit, valuation and liquidity risk. The value of the collateral securing a loan may not be sufficient to cover the amount owed, may be found invalid or may be used to pay other outstanding obligations of the borrower under applicable law. There is also the risk that the collateral may be difficult to liquidate, or that a majority of the collateral may be illiquid.

Fixed income investments are subject to credit risk of the issuer and the effects of changing interest rates. Interest rate risk refers to the risk that bond prices generally fall as interest rates rise and vice versa. An issuer may be unable to meet interest and/or principal payments, thereby causing its instruments to decrease in value and lowering the issuer’s credit rating.

The risks of investing in securities of foreign issuers can include fluctuations in foreign currencies, political and economic instability, and foreign taxation issues.

Alternative products typically hold more nontraditional investments and employ more complex trading strategies, including hedging and leveraging through derivatives, short selling and opportunistic strategies that change with market conditions. Investors considering alternatives should be aware of their unique characteristics and additional risks from the strategies they use. Like all investments, performance will fluctuate. You can lose money.

The information provided is for educational purposes only and does not constitute a recommendation of the suitability of any investment strategy for a particular investor. Invesco does not provide tax advice. The tax information contained herein is general and is not exhaustive by nature. Federal and state tax laws are complex and constantly changing. Investors should always consult their own legal or tax professional for information concerning their individual situation. The opinions expressed are those of the authors, are based on current market conditions and are subject to change without notice. These opinions may differ from those of other Invesco investment professionals.

All data provided by Invesco unless otherwise noted.

Invesco Distributors, Inc. is the US distributor for Invesco Ltd.’s retail products and collective trust funds. Invesco Advisers, Inc. and other affiliated investment advisers mentioned provide investment advisory services and do not sell securities. Invesco Unit Investment Trusts are distributed by the sponsor, Invesco Capital Markets, Inc., and broker-dealers including Invesco Distributors, Inc. Each entity is an indirect, wholly owned subsidiary of Invesco Ltd. PowerShares® is a registered trademark of Invesco PowerShares Capital Management LLC, investment adviser. Invesco PowerShares Capital Management LLC (Invesco PowerShares) and Invesco Distributors, Inc., ETF distributor, are indirect, wholly owned subsidiaries of Invesco Ltd.

©2016 Invesco Ltd. All rights reserved.

2016 alternatives performance: How are they doing so far? by Invesco