Key Points

▪ The negative feedback loop that dominated financial markets earlier this year has faded and reversed.

▪ There are a number of potential downside risks for equities, but we expect the positive factors will win out over time.

Market Trends Have Reversed for the Better

Early in 2016, financial markets were dominated by a negative feedback loop. Chinese economic conditions were deteriorating, which drove fears of global deflation. Oil prices fell as a result, which put downward pressure on credit markets, the banking system and the broader global economy. Those trends have recently started to reverse. Confidence in the global economy is growing, oil prices are rising and stabilizing, worries about Chinese currency devaluation are receding and credit markets appear healthier.

Global financial markets now appear in better condition than they did a few months ago. U.S. stock prices are approaching their cyclical highs and credit spreads have been narrowing.1 Investors remain jittery, however, and are focused on a number of near-term risks, including Federal Reserve policy, uncertain earnings and an unstable geopolitical backdrop.

Key Variables for Financial Markets

So what are the factors that are likely to determine the future direction of markets? We point to the following key variables:

1. The Global Economy: The world has proven to be quite resilient to shocks over the past few years, and we expect growth to improve modestly this next year. Should global manufacturing improve (and we expect it will), it would go a long way toward promoting better growth.

2. China: Authorities face a difficult task as they need to rebalance their economy while promoting growth. The stronger U.S. dollar is pressuring the Chinese economy, but we do not anticipate a hard landing.

3. The Federal Reserve: Given the more hawkish tone the Fed has recently adopted, the odds of a rate hike in June or July have risen. Fed action has the potential to trigger volatility in oil prices, the dollar and equity markets. But we do not believe disruptions will be overly significant.

4. Oil Prices: Production levels will likely remain high. We are not expecting to see cuts from OPEC, and U.S. production may drift higher over the coming year.1 We think oil prices will remain range bound, but the risk of another rout in prices cannot be ruled out.

5. Credit Spreads: Many fear that the U.S. credit cycle is in the late stages, which has triggered on-and-off selling pressure for high yield debt. We believe credit conditions are improving and high yield markets continue to look attractive, which would be a positive sign for the economy and equities.

6. Corporate Earnings: Earnings have been in a year-long decline. We think headwinds are fading, but investors need to see evidence that earnings results can turn positive. We are seeing forward guidance turn positive in key sectors such as industrials,1 and we expect better earnings results in the second half of this year.

7. Politics: There are a number of geopolitical events that could rattle financial markets, including the referendum on the U.K. leaving the European Union and the upcoming U.S. elections. High levels of uncertainty are a negative for risk assets, and the political backdrop is anything but certain.

Equity Markets May Be Poised for Outperformance

On balance, we see more positives than negatives for equity markets. A number of potential downside risks exist, with the two most prominent being questions over Fed policy and the rising value of the dollar. These factors could weigh on stock prices in the near term, particularly given uncertainty over global economic growth and corporate earnings.

Nevertheless, we have a positive long-term outlook for equities and believe they will outperform bonds and cash over the next six to twelve months. Should we see a price breakout to the upside, that would be a clear bullish sign, and could lead investors to believe that the downtrend evident over the past year has faded.

It would be a mistake to discount the risks to equities, but we believe it might be a bigger mistake to discount the positives.

1 Source: MRB Partners

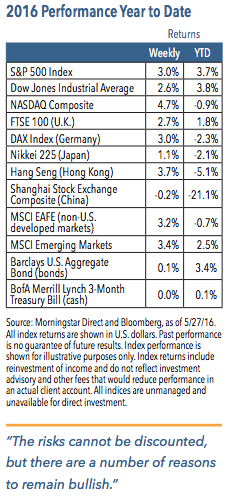

The S&P 500 Index is a capitalization-weighted index of 500 stocks designed to measure the performance of the broad domestic economy. The Dow Jones Industrial Average is a price-weighted average of 30 significant stocks traded on the New York Stock Exchange and the Nasdaq. The Nasdaq Composite is a stock market index of the common stocks and similar securities listed on the NASDAQ stock market. FTSE 100 Index is a capitalization-weighted index of the 100 most highly capitalized companies traded on the London Stock Exchange. Deutsche Borse AG German Stock Index (DAX Index) is a total return index of 30 selected German blue chip stocks traded on the Frankfurt Stock Exchange. Nikkei 225 Index is a price-weighted average of 225 top-rated Japanese companies listed in the First Section of the Tokyo Stock Exchange. Hong Kong Hang Seng Index is a free-float capitalization-weighted index of selection of companies from the Stock Exchange of Hong Kong. Shanghai Stock Exchange Composite is a capitalization-weighted index that tracks the daily price performance of all A-shares and B-shares listed on the Shanghai Stock Exchange. MSCI EAFE Index is a free float-adjusted market capitalization weighted index designed to measure developed market equity performance, excluding the U.S. and Canada. The MSCI Emerging Markets Index is a free float-adjusted market capitalization index that is designed to measure equity market performance of emerging markets. Barclays U.S. Aggregate Bond Index covers the U.S. investment grade fixed rate bond market. The BofA Merrill Lynch 3-Month U.S. Treasury Bill Index is an unmanaged market index of U.S. Treasury securities maturing in 90 days that assumes reinvestment of all income.

RISKS AND OTHER IMPORTANT CONSIDERATIONS

The views and opinions expressed are for informational and educational purposes only as of the date of writing and may change at any time based on market or other conditions and may not come to pass. This material is not intended to be relied upon as investment advice or recommendations, does not constitute a solicitation to buy or sell securities and should not be considered specific legal, investment or tax advice. The information provided does not take into account the specific objectives, financial situation, or particular needs of any specific person. All investments carry a certain degree of risk and there is no assurance that an investment will provide positive performance over any period of time. Equity investments are subject to market risk or the risk that stocks will decline in response to such factors as adverse company news or industry developments or a general economic decline. Debt or fixed income securities are subject to market risk, credit risk, interest rate risk, call risk, tax risk, political and economic risk, and income risk. As interest rates rise, bond prices fall. Noninvestment-grade bonds involve heightened credit risk, liquidity risk, and potential for default. Foreign investing involves additional risks, including currency fluctuation, political and economic instability, lack of liquidity and differing legal and accounting standards. These risks are magnified in emerging markets. Past performance is no guarantee of future results.

CFA® and Chartered Financial Analyst® are registered trademarks owned by CFA Institute.

Nuveen Asset Management, LLC is a registered investment adviser and an affiliate of Nuveen Investments, Inc.

©2016 Nuveen Investments, Inc. All rights reserved.