2Q 2016 Outlook How Long Will Markets Continue This Wild Ride?

Markets have taken investors on a wild ride in 2016, with conflicting messages about expectations for economic growth and inflation. Through April, the S&P 500 Index had returned just more than 3%, erasing its 10% correction at the start of the year. Since a trough on Feb. 11, global and domestic equities have largely followed suit and rebounded to the levels of fourth-quarter 2015. The 10-year U.S. Treasury yield hit a low for the year so far of 1.66% on that date, but ended April around 1.83% — although not without its own choppiness. The CBOE Volatility Index spiked in January and February, fell off in March and early April and then showed rising volatility again at the end of April. In our view, this has become a speculative market.

Markets and growth

We have added to the gold bullion position in the Fund, based on our assessment of the current environment. We think the violent market fluctuations are evidence of continued global growth concerns and an eventual increase in money printing. That’s what we see as the likely response by central banks to the extended period of low — and now negative — interest rates around the globe. Such a response also reflects an appreciation for the amount of leverage – or the debt used to finance asset growth – built up in the world’s economy since the global financial crisis. (See Chart 1.) In our view, the world is trying to solve a debt problem with more debt. Ultimately, we don’t think that will work.

The markets’ gyrations also may be a response to conflicting signals from the U.S. Federal Reserve (Fed). The Fed in December 2015 increased short-term interest rates by 25 basis points after seven years at zero, but left uncertainty about the timing of additional rate hikes because of acknowledged risks to the global economy.

To be sure, the U.S. economy is performing better than most other developed markets. In Japan, the yen rallied during most of the first quarter and ended April at its strongest level since fourth-quarter 2014. This result was despite the Bank of Japan moving to a negative interest rate policy in January in order to weaken the currency. The move has negative implications for the economy as it makes the country less competitive.

Similarly, the euro has moved off its lows of November 2015 and onto a higher trajectory this year. This move came as the European Central Bank (ECB) continued to cut rates in March and expand its quantitative easing (QE) facility, although it kept rates unchanged in April.

Given its more dovish tone along with recent mixed economic data, we don’t believe the Fed will hike interest rates again until at least the fourth quarter. Under that circumstance, we don’t think the U.S. dollar can strengthen much from current levels versus developed-market currencies. The dollar has been under pressure most of this year and could continue to weaken against the yen. Upcoming events in continental Europe, including the ECB's QE expansion, and the June referendum in the U.K. on withdrawing from the European Union (Brexit) could send both the euro and pound lower versus the dollar this summer. In emerging markets, the dollar has been broadly weaker. This has been particularly true versus the Brazilian real. The dollar was 15% lower versus the real through April.

Then there's China

Questions remain about China’s growth prospects. However, its economic data have strengthened recently in response to policy changes to stimulate investment in housing and certain areas within infrastructure. Commodity prices and related equities have taken the cue. The People’s Bank of China has aggressively added liquidity to the banking system and credit availability has begun to accelerate. That is in part a response to expansion of the sovereign balance sheet and new incentives to fund and pursue infrastructure projects. Despite what is widely seen as the mistake of 2009 — a credit-driven buildup in manufacturing capacity that caused a dramatic increase in the ratio of debt to gross domestic product (GDP) — China is moving down a similar path (its declarations to the contrary notwithstanding) to reignite growth.

This is occurring even though credit growth has outpaced growth in nominal GDP since the global financial crisis, leaving the country with a highly indebted corporate sector and mounting stress in the banking system. (See Chart 2.) Perhaps the strength of the yuan and low commodity costs will create the right environment to harness large pools of private and public savings and convert them into GDP growth.

China’s net debt is $25 trillion, significantly greater than other emerging market countries and 50% higher than one year ago. Many of the materials, energy, and industrials (MEI) stocks that had been under pressure for the last year moved higher in anticipation of China’s massive investment. This rally broadened to other sectors in the markets and the push higher ensued.

Time will tell how successful these latest stimulus measures will be, but early indicators in China suggest some traction: fixed asset investment starts (excluding property) spiked in February; property starts increased; total financing (social financing, local government bonds, sovereign bonds) grew more than 15% year over year, with broader measures registering much stronger growth; March auto sales increased 10%; and heavy truck and excavator sales picked up sharply. The market appears torn over both the magnitude and duration of this latest stimulus push. We are torn as well, but believe China can affect policy through the calendar year if it pushes the right buttons.

Our portfolio approach

The Fund has been underweight the MEI space, as the pullback in emerging-market demand and a buildup in inventories has pressured these groups for more than 18 months. The stocks of companies in these sectors have seen a bounce since the start of the year and particularly since China’s stimulus announcement in mid-February. China’s stimulus measures eventually will end, but that could take some time. Until then, we have added to areas within the MEI sectors on the expectation that they may be undervalued; these include mining, energy exploration & production (E&P) companies, and materials.

The Fund is overweight the health care sector and that group has some well-known macro challenges. We believe 2016 will continue to be challenging for the sector, given the political environment and worries about inflation in drug prices. Some of the compression in multiples this year has related to incomplete or cancelled deal activity. The most notable in the quarter occurred when the deal between Pfizer and Allergan was cancelled. Both are portfolio holdings.*

Despite this setback, we think mergers and acquisitions (M&A) remain a viable way for companies to improve their growth prospects, especially before another innovation cycle gets underway. Since topline growth is difficult to come by, we think there is potential within health care for companies with robust product pipelines, attractive valuations or M&A prospects that can offer attractive returns over the next two to three years.

The “connected world” also remains a focus in the Fund. We look for names that overlap with other sectors as the reliance on cheaper, faster technology in the form of robotics and connectivity permeates autos, health care, infrastructure and other industries. The trend of disruptive technology in retail and via the internet shows no signs of abating. We have added to these areas on price pullbacks.

Facing the headwinds

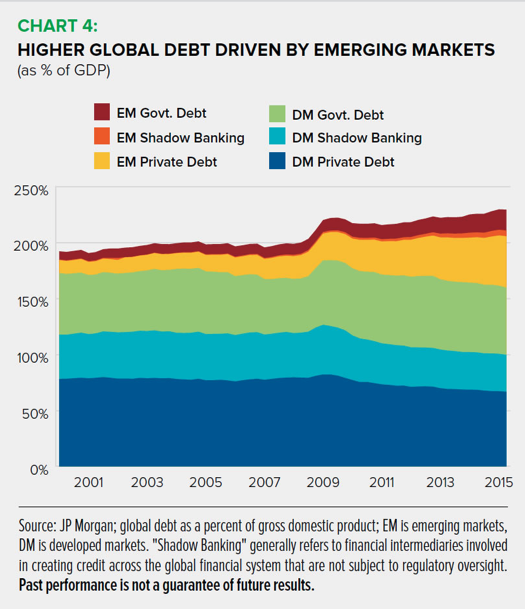

It is impossible to fully know the amount of leverage accumulated in the global financial system, although we know the growth has been massive in emerging market balance sheets – corporates and sovereigns alike. The multiple growth scares over the last year typically gain potency in a highly leveraged, low-growth world. One thing is clear: The fundamental issues facing the global economy have not been solved. We think the ongoing trends of slower growth and rising debt will continue to magnify the effects of slight changes in the markets’ assumptions for global growth. (See Charts 3 and 4.)

We also believe that these headwinds mean growth will be challenged for all global industries and companies. As such, we remain focused on where in the world we think growth will occur. Many of our holdings from last year remain core holdings in 2016. Our highest conviction names fall into the secular — or long-term — growth category with strong balance sheets that offer optionality of share repurchases, dividends, or acquisitions, along with certain cyclical energy companies.

*Pfizer, Inc., 1.32%, and Allergan plc, 1.53% of net assets as of 03/31/2016.

Past performance is not a guarantee of future results.The opinions expressed are those of the Fund’s portfolio managers and are not meant as investment advice or to predict or project the future performance of any investment product. The opinions are current through May 2016 and are subject to change due to market conditions or other factors.

Risk factors:The value of the Fund’s shares will change, and you could lose money on your investment. The Fund may allocate from 0 to 100% of its assets between stocks, bonds and short-term instruments of issuers around the globe, as well as investments in precious metals and investments with exposure to various foreign securities. International investing involves additional risks, including currency fluctuations, political or economic conditions affecting the foreign country, and differences in accounting standards and foreign regulations. These risks are magnified in emerging markets. Fixed-income securities are subject to interest-rate risk and, as such, the net asset value of the Fund may fall as interest rates rise. Investing in high-income securities may carry a greater risk of nonpayment of interest or principal than higher-rated bonds. The Fund may focus its investments in certain regions or industries, thereby increasing its potential vulnerability to market volatility. The Fund may seek to hedge market risk on various securities, increase exposure to various markets, manage exposure to various foreign currencies, precious metals and various markets, and seek to hedge certain event risks on positions held by the Fund via the use of derivative instruments. Such investments involve additional risks, as the fluctuations in the values of the derivatives may not correlate perfectly with the overall securities markets or with the underlying asset from which the derivative’s value is derived. Investing in commodities is generally considered speculative because of the significant potential for investment loss due to cyclical economic conditions, sudden political events, and adverse international monetary policies. Markets for commodities are likely to be volatile and the Fund may pay more to store and accurately value its commodity holdings than it does with the Fund’s other holdings. These and other risks are more fully described in the Fund’s prospectus. Not all funds or fund classes may be offered at all broker/dealers.

The S&P 500 Index is an unmanaged index that generally represents the U.S. stock market. The CBOE Volatility Index is a key measure of market expectations of near-term volatility conveyed by S&P 500 stock index option prices. It is not possible to invest directly in an index.

IVY INVESTMENTS℠ refers to the financial services offered by Ivy Distributors, Inc., a FINRA member broker dealer and the distributor of IVY FUNDS® mutual funds, and those financial services offered by its affiliates.

Before investing, investors should consider carefully the investment objectives, risks, charges and expenses of a mutual fund. This and other important information is contained in the prospectus and summary prospectus, which may be obtained at www.ivyinvestments.com or from a financial advisor. Read it carefully before investing.