KEY TAKEAWAYS

- Thursday’s “Brexit” vote, during which the U.K. will vote to stay or leave the EU, has had considerable impact on the markets recently.

- The pattern from similar recent votes suggests that the chances of the U.K. staying are greater than the polls suggest.

- The EU and U.K. are significant trading partners; should there be a leave vote, the long process for leaving the EU means that any impact on the economy will be months or years in the future.

This week’s vote in the United Kingdom (U.K.) on remaining in the European Union (EU) could have significant implications for both parties. Polling data suggest that the vote will be very close, though historically, in similar situations people vote retain the status quo in greater proportions than the polling suggests. There is no set process should the U.K. decide to leave; the process will require negotiation with the EU and internally in the U.K. The trade and financial connections between the U.K. and the EU are complex and significant to both parties. Although the U.K. runs a deficit on trade of goods with the EU, it has a large surplus in trade of services globally and is the EU’s primary financial services hub. Though the market impact of a “leave” vote would be immediate, actual changes in trade and trade policy would take place over months and years.

WHAT is the timetable related to the Brexit vote?

On Thursday, June 23, 2016, citizens from the U.K. (England, Scotland, Wales, and Northern Ireland) will vote on whether to leave or remain in the EU. The results should be known by early Friday morning (June 24), and at least by the market open on Friday morning in the U.S. The financial markets would clearly breathe a sigh of relief in the event of a “remain” vote. However, this may not permanently settle the issue. A significant number of Britons will vote to leave the EU, but the movement would have very little political standing. Prime Minister David Cameron has staked his political career on the U.K. remaining in the EU. Maybe it will resurface periodically, as the other independence movements do, but a “remain” vote will likely close the issue for the next few years.

If the vote is to leave, the political and economic ramifications will create more uncertainty. Within the EU, the process is governed by Article 50 of the Treaty of Lisbon that created the current EU structure in 2009. The Article is just 260 words, effectively saying that there will be negotiations between the parties that can take up to two years. The complication arises because the negotiations would take place with the U.K. government, which is currently led by someone who has opposed the leave vote in the first place. It is quite likely that a new government would have to be installed in the U.K. before meaningful progress could be made.

Recent Votes on Independence

There have been two relatively recent votes on independence: Scotland’s attempt to leave the U.K. in September 2014, and the Quebec vote on secession from Canada in 1995 (this may not be recent by common terms, but these votes are so rare we believe it is worth including). In both cases, polling data immediately before the vote proved suspect. In both cases, the final vote for the status quo (staying in the current political configuration) was nearly 6% higher than polls predicted. In the case of Quebec, the polls predicted a “leave” vote, while the final vote was a narrow “stay.” In Scotland, the vote to remain in the U.K. was over 10% greater, compared to a 4% expected margin of victory that was expected. We also examined the data related to the Catalonian independence movements from Spain. In this case, polling data favoring independence was correct. However, in Spain the votes were non-binding and actual voter turnout was below 40%.

HOW IMPORTANT IS EUROPE TO THE U.K.?

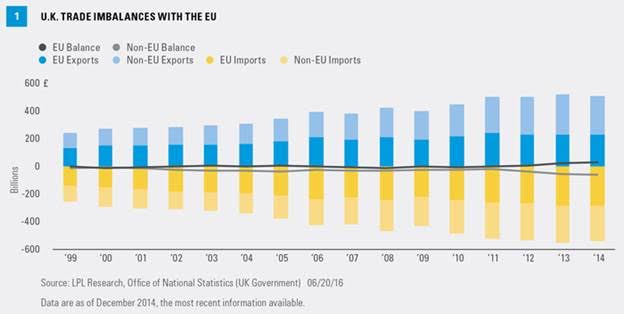

A major issue in the Brexit vote is the impact on trade in goods and services. Figure 1 provides an overview of the U.K.’s total trading relations. A few trends have been impacting U.K. opinion on relations with EU. For example, while U.K. imports from the EU have been increasing since the Great Recession, exports to the EU have been stagnant. The trade picture with the rest of the world is more balanced, with the U.K. running a modest trade surplus with the rest of the world. Politicians in the U.K. have been quick to highlight this rising trade deficit with the EU, suggesting that Europe is dragging the U.K. down.

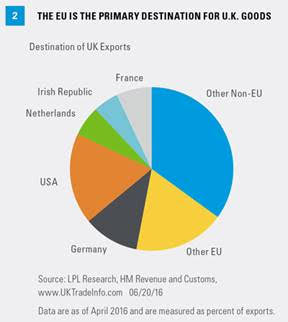

Some have claimed the EU needs the U.K. more than the U.K. needs the EU but Figures 2 and 3 suggest the opposite. U.K. exports to the EU represent 47% of its total exports, with Germany being the single largest destination for exports. It is much more difficult to determine trade within the EU broken out by country. The U.K. denominates trade in pounds, whereas the EU statistics are calculated using the euro. However, examining data from the European Commission shows a basic idea of the magnitude of trade [Figure 3]. Trade from the EU to the U.K. is only about 6.5% of total exports and 10.3% of total inter-European exports. Once again, Germany, at 13%, receives the bulk of European exports and 20.6% of total inter-European exports.

THE DEVIL IS ALWAYS IN THE DETAILS

It’s worth considering the U.K.’s trade relationships with the EU, regardless of the results of Thursday’s vote. There are two components to trading agreements: tariffs (taxes paid on goods at the border) and rules governing trade. Even without free trade zones like those within EU, tariffs on global trade have been steadily declining since the end of World War II. The average tariff on goods between the EU (including the U.K.) and the U.S., its largest trading partner, is 3%. However, it varies considerably by type of product; for example, average tariffs on agricultural products into the EU are 18%. Under the World Trade Organization (WTO), the EU would not be allowed to impose punitive tariffs on the U.K. goods.

Therefore, on its face, the worst case scenario for the U.K. is that its goods would be subject to the same tariff rates as other major countries. Those campaigning for a “leave” suggest that the U.K. will be able to negotiate even these tariffs away; Switzerland and Norway have broader access to EU markets while still remaining outside the formal framework. However, we know where the devil lies. One of the frustrating things for EU opponents is the volume of rules and regulations that membership entails. Given current low tariff rates, it is the negotiation of these rules that drives trade deals. Voting to leave would not eliminate the rules. First, should the U.K. seek to negotiate a separate trade deal (the Switzerland model), it would still be subject to trade rules and regulations. Furthermore, the EU would have every incentive to play hardball with the U.K. in any trade negotiations. After all, if the EU lets the U.K. retain some sort of preferred trading partner status, what is the incentive for other nations not to take the same tact and vote to leave?

The other reality is that the EU works by having each nation’s government formally adopt rules as part of its legal framework. Leaving the EU would not automatically remove these laws from U.K. law. Repealing them would require acts of Parliament and actions by the various U.K. government agencies. Even this is not certain. For example, there may be groups within the U.K. that agree with some of the rules required by the EU, and may advocate for their retention on their own merit, regardless of their EU origin. These might include groups focused on labor, environmental, and consumer protection. Either way, uncertainty—the enemy of markets and economic prosperity—would likely prevail, perhaps for years to come.

NO SERVICE PLEASE, WE’RE BRITISH

Services are also an important part of the trade picture, but trade in services is also much harder to calculate. With physical goods, it’s easy enough (at least conceptually) to count widgets as they cross the border. It is much more difficult to track business services across borders. Financial services in particular are important to the U.K., as London is the European headquarters for many major global banks. We discussed this issue, particularly the importance of “passporting” (the ability of a bank with a presence anywhere in the EU to operateeverywhere under equal terms) in last week’s Weekly Market Commentary, “Brexit: Should They Stay or Should They Go?”

We cannot calculate with any degree of reliability the U.K.’s trade surplus with the rest of the EU. However, we know that the U.K. runs a $135 billion dollar trade surplus in services, according the Organization of Economically Developed Countries (OECD). In contrast, Germany, which runs a surplus on goods with most countries, runs a global deficit in trade with services. Therefore, we can infer that the U.K. runs a significant service surplus with the rest of the EU, even though the exact numbers are unknown. This surplus in services helps pay for the U.K.’s deficit on trade it goods. It also provides fairly high paying jobs in banking, insurance, accounting, and other related services. However, this fact also highlights the divisions within the U.K. of more educated and more affluent people, based largely in the major cities, who are benefiting from trade, while traditional manufacturing jobs are perceived to be suffering from it.

CONCLUSION

The issues regarding how trade in both goods and services will be impacted are important factors into this week’s upcoming Brexit vote. Regardless of the outcome, the U.K. and the EU have a deep and calculated relationship. Should the U.K. vote to “leave,” that relationship will change, but it will not end.

IMPORTANT DISCLOSURES

The opinions voiced in this material are for general information only and are not intended to provide or be construed as providing specific investment advice or recommendations for your clients. All performance referenced is historical and is no guarantee of future results. Any economic forecasts set forth in the presentation may not develop as predicted and there can be no guarantee that strategies promoted will be successful.International investing involves special risks such as currency fluctuation and political instability and may not be suitable for all investors. All investing involves risk including loss of principal.

This research material has been prepared by LPL Financial.

To the extent you are receiving investment advice from a separately registered independent investment advisor, please note that LPL Financial is not an affiliate of and makes no representation with respect to such entity.

Not FDIC or NCUA/NCUSIF Insured | No Bank or Credit Union Guarantee | May Lose Value | Not Guaranteed by Any Government Agency | Not a Bank/Credit Union Deposit

RES 5540 0616 | Tracking #1- 508468 (Exp. 06/17)