KEY TAKEAWAYS

- The U.K.’s unexpected decision to leave the EU sent markets reeling on Friday.

- We believe the Brexit’s impacts on earnings and U.S. stocks may be limited; we maintain our 2016 year-end S&P 500 forecast for mid-single-digit returns.*

- However, uncertainty in Europe, seasonal weakness, and the U.S. presidential election may contribute to further volatility.

The United Kingdom’s (U.K.) unexpected decision to leave the European Union (EU) sent markets reeling on Friday (June 24, 2016). The S&P suffered a 3.6% decline, its worst day of 2016. But that loss was muted in comparison to the 8.6% drop in Europe’s EURO STOXX 50 Index—its biggest one-day loss in 30 years—or the nearly 9% drop in the British pound versus the U.S. dollar to a 31-year low. Investors fled to safe havens such as U.S. Treasuries, the U.S. dollar, and gold amid the political uncertainty. These moves were exaggerated by the unwinding of “remain” trades that were made in the days leading up to the vote, when global equities, European markets, and banks in particular, had risen.

Perhaps the most surprising market reaction was in the U.K. stock market. The FTSE 100 Index in the U.K. fell just 3% (in local currency), slightly outperforming U.S. stocks, and ended last week (June 20–24) up 2%, for its best week in the past 10. U.K. stocks likely benefited from the potential export boost from the weaker pound. Plus, these are global companies that generate most of their revenue outside of the U.K. In U.S. dollars, however, U.K. stocks suffered double-digit losses.

This week we look at the potential U.S. economic, earnings, and market implications of this historic event—the first reversal after many decades of European integration.

*Historically since WWII, the average annual gain on stocks has been 7-9%. Thus, our forecast is roughly in-line with average stock market growth. We forecast a mid-single digit gain, including dividends, for U.S. stocks in 2016 as measured by the S&P 500. This gain is derived from earnings per share (EPS) for S&P 500 companies assuming mid-to-high-single-digit earnings gains, and a largely stable price-to-earnings ratio. Earnings gains are supported by our expectation of improved global economic growth and stable profit margins in 2016.

Additional disclosure on page 1:

U.S. Treasuries, the U.S. dollar, and gold may be considered “safe haven” investments but do carry some degree of risk. Treasuries include interest rate, credit, and market risk. They are guaranteed by the U.S. government as to the timely payment of principal and interest and, if held to maturity, offer a fixed rate of return and fixed principal value. Precious metal (gold) investing involves greater fluctuation and potential for losses. The potential for fast price swings in currencies may result in significant volatility in an investor’s holdings.

POTENTIAL ECONOMIC IMPACT

As discussed in this week’s Weekly Economic Commentary, we expect minimal impact on the U.S. economy from the Brexit. Although the odds of a U.S. recession in the next 12–18 months may have risen slightly, we believe they remain well below 50%. The stronger dollar from tightening financial conditions will be a slight drag on U.S. exports, but exports only represent about 15% of U.S. gross domestic product (GDP), and the U.K. composes just a small fraction of that. Even the much larger EU, which will see some negative economic impact from breaking trading ties with the U.K., comprises just 17% of U.S. exports.

The wild card is how this vote affects other countries considering leaving the EU. Should other countries leave over time and the EU unravel (though not our view), the economic and financial market implications could be quite significant and resemble the European debt crisis in 2012. This political uncertainty could be with us for some time as negotiations between the U.K. and EU (which cannot begin until new British leadership is in place) may be very tough and could take more than the prescribed two years. Anti-integration leaders in several countries, including France, have already called for their own referenda.

POTENTIAL EARNINGS IMPACT

The Brexit will have some negative impact on corporate profits through a stronger U.S. dollar. But in the second quarter of 2016, the dollar should have a minimal impact on earnings despite the surge in the currency on Friday, June 24, 2016. The stronger dollar is putting some downward pressure on commodity prices, which will be a drag on energy and materials sector profits. We expect that tightening financial conditions, lower interest rates, and U.K. exposure will likely have some incremental negative impact on financial sector profits, which was reflected in that sector’s 5.4% drop on Friday, the worst among all S&P sectors.

The good news is most companies have minimal exposure to the U.K., and the U.S. dollar is little changed over the past year against the global basket of currencies that make up the U.S. Dollar Index. So although some companies may use the Brexit as an excuse for falling short of estimates, overall we would expect U.S. companies to surpass expectations for a mid-single-digit year-over-year decline (Thomson Reuters consensus estimates), which could help reassure some of the Brexit fears. Companies begin reporting in mid-July. Look for our second quarter 2016 earnings preview in the July 5, 2016 edition of the Weekly Market Commentary.

POTENTIAL MARKET IMPACT

Despite the uncertainty posed by the Brexit, we are sticking with our 2016 forecast for mid-single-digit S&P 500 total returns and ongoing volatility, as we wrote in ourOutlook 2016 publication. As of early trading Monday morning, June 27, the S&P 500 is down about 2% year to date, and just 1% including dividends.

The Brexit’s likely limited economic and earnings impact is the primary reason for our optimism. The likelihood that the Federal Reserve (Fed) hikes just once this year, not twice as we had previously anticipated, is also supportive. We continue to expect corporate earnings to rebound solidly in the second half of 2016 despite the Brexit impact. Stock market valuations remain reasonable, especially considering low interest rate levels. There are some encouraging technical signs, as we discuss below. Finally, in looking back at other big down days following periods of relatively modest volatility,1 stocks have generally fallen only marginally over the subsequent month and produced solid gains (median of 6%) over the subsequent three months.

But that does not mean we expect a smooth ride. Given the political uncertainty in Europe is likely to linger and other countries may follow the U.K., a correction (a 10% or more decline) is certainly possible. The summer is seasonally weak for stocks historically and the U.S. election still has the potential to cause volatility.

TECHNICAL ANALYSIS PERSPECTIVE

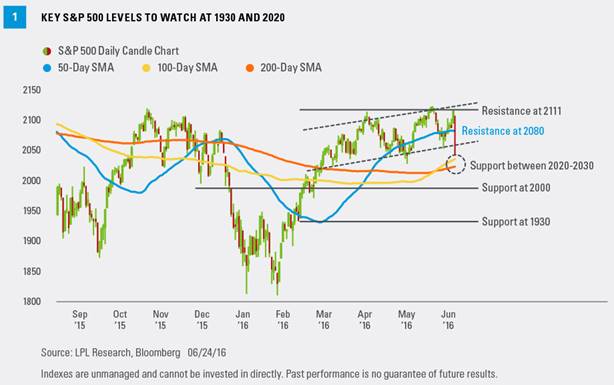

We asked our technical strategist David Tonaszuck to share his key technical support levels to watch for the S&P 500. The index’s daily price is in the process of breaking trend channel support at 2055. Below 2055, the next level of support is the area between 2020 (the 200-day simple moving average [SMA]) and 2030 (the 100-day SMA) [Figure 1]. A closing price below 2020 for five trading days increases the likelihood of a drop to the next support level at 1930, 9% below the all-time closing high on May 21, 2015.

For the optimists, the next bullish catalyst would be a closing price back above 2080 (the 50-day SMA), which would be an initial signal for a potentially aggressive buy on the dip opportunity.

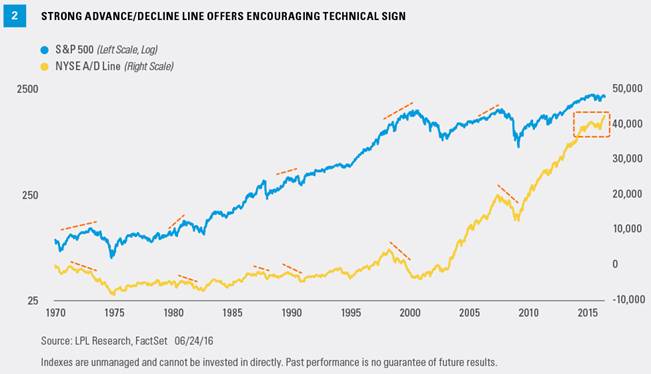

Market breadth, the number of stocks participating in a rally, currently offers an encouraging technical sign. We mentioned strong market breadth as a reason for optimism in last week’s Weekly Market Commentary. One of our favorite ways to measure market breadth is via advance/decline lines (A/D lines). A/D lines are computed daily by adding the number of securities in an index that are higher and subtracting the number that are lower. An upward-trending A/D line indicates broad participation and underlying strength, a good sign.

The New York Stock Exchange (NYSE) A/D line was actually higher last week, closing at a new weekly all-time high in the process. This indicator tends to lead actual price, so this new high could bode well for equities over the coming months. As Figure 2 shows, at all major market tops, the NYSE A/D line broke down in advance of the actual peak in equities. In other words, breadth provided a warning sign at every meaningful market peak. We consider the lack of a warning sign to be encouraging.

CONCLUSION

We know markets do not like uncertainty, and the U.K.’s vote to leave the EU has introduced new economic and political uncertainty that likely won’t go away quickly; but there are enough positives for this market to give us the confidence that 2016 can still be a positive year for U.S. stocks. We may be in for some more volatility, but long-term investors should stick to their plans. More tactical investors may want to consider a slightly more conservative stance in the near term until we have more clarity on the political landscape.

IMPORTANT DISCLOSURES

The opinions voiced in this material are for general information only and are not intended to provide specific advice or recommendations for any individual. To determine which investment(s) may be appropriate for you, consult your financial advisor prior to investing. All performance referenced is historical and is no guarantee of future results.

The economic forecasts set forth in the presentation may not develop as predicted and there can be no guarantee that strategies promoted will be successful.

Investing in stock includes numerous specific risks including: the fluctuation of dividend, loss of principal, and potential liquidity of the investment in a falling market.

International investing involves special risks such as currency fluctuation and political instability and may not be suitable for all investors.

All investing involves risk including loss of principal.

INDEX DESCRIPTIONS

The Standard & Poor’s 500 Index is a capitalization-weighted index of 500 stocks designed to measure performance of the broad domestic economy through changes in the aggregate market value of 500 stocks representing all major industries.

The USD Index measures the performance of the U.S. dollar against a basket of foreign currencies: EUR, JPY, GBP, CAD, CHF and SEK. The U.S. Dollar Index goes up when the dollar gains “strength” compared to other currencies.

The EURO STOXX 50 Index is a blue-chip index for the Eurozone, which covers 50 stocks from 12 Eurozone countries: Austria, Belgium, Finland, France, Germany, Greece, Ireland, Italy, Luxembourg, the Netherlands, Portugal, and Spain.The FTSE 100 is an index of blue-chip stocks on the London Stock Exchange.

1 Analysis of the past 11 occurrences of 3% drops in the S&P 500 after prior low-volatility periods, since 1987.