Editor’s Note: The following insight comes from Korea Investment Management – a leading adding asset manager in South Korea – and continues a series of posts intended to introduce South Korea as an investment destination.

Over our previous writings on AlphaBaskets, we have covered the reasons why the services sector's growth potential exceeds that of manufacturing and why consumer sectors are better positioned than industrials. This is not a temporary phase, but a structural change as Korea evolves into a developed economy.

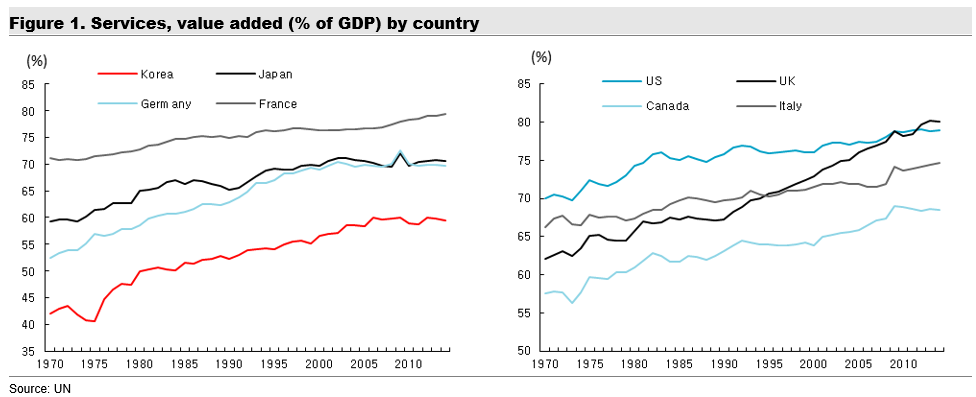

A review of G7 countries, the leading developed markets (DMs) confirms this type of de-industrialization as the weighting of manufacturing declines gradually. Even in Japan and Germany, which have relatively high manufacturing weightings among G7 countries, the weighting of services to total GDP has been trending gradually upward. During 1970-2014, the weightings of services in Japan and Germany have climbed by 22.2% and 20.1%, respectively.

In Korea, the services weighting increased 18.2% from 41.2% in 1970 to 59.4% in 2014. However, this is still relatively low compared to the current services weighting in the global economy of 66.0% and the average G7 weighting of more than 70%. Accordingly, the weighting of the Korean services sector should continue to rise going forward.

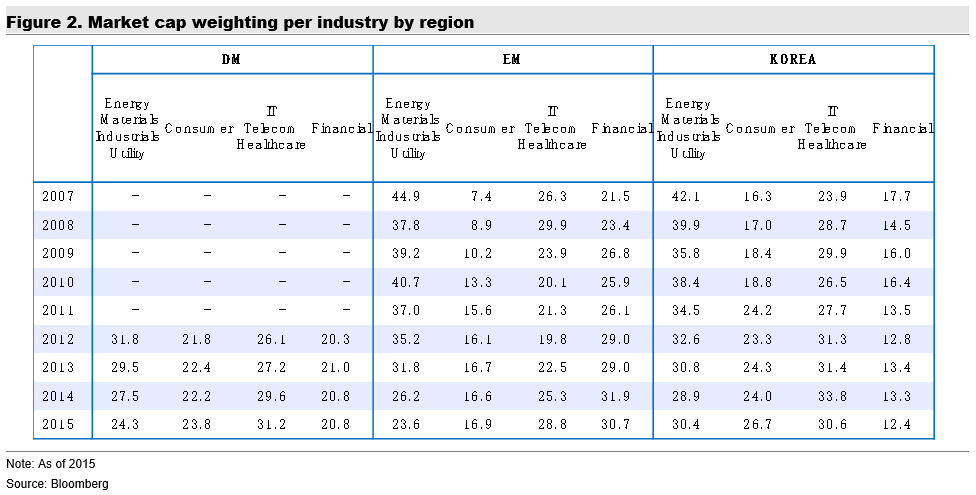

And, these structural changes are being quickly reflected in stock markets. In DMs, the market caps of consumer staples, IT, communications and healthcare are relatively high compared to that of emerging markets (EMs). Of note, Korea’s market cap breakdown is similar to that of DMs. Specifically, the market cap weighting of industrial-related manufacturing is 24.3% in DMs, while the combined weighting of consumer staples, IT, telecommunications and healthcare is close to 55%. In EMs, industrials account for 23.6% of the market while consumer plays comprise 45.7%. In Korea, industrial comprise 30.4% and consumer goods 53.7%.

Korea’s manufacturing sector has been recognized globally for its competitiveness and it accounts for most of total value added. And, traditional Korean manufacturers are shifting towards “smart manufacturing” that combines manufacturing with ICT and manufacturing companies are trying to secure new growth by entering service markets.

Given the high R&D spending, robust IT infrastructure and human resources, this structural shift should progress smoothly in Korea. In fact, many Korean companies are rapidly adopting and localizing new innovations and services from DMs to secure new earnings streams and growth drivers.

On the other hand, amid the ongoing global glut in industrial-related manufacturing, corporate profit growth continues to erode. And, the manufacturing oversupply is unlikely to be resolved over the near term. Given the growing risk of an economic hard-landing in China, the government will likely have to adjust the pace of restructuring the local manufacturing industry.

With the slow global economic growth, policy makers in major countries will likely continue economic stimulus efforts. And, the effects of these measures should be more apparent in consumer goods and services, which face relatively milder oversupply problems. Amid these conditions, Korea is favorably positioned as its capital market structure is more advanced than other EMs.

The information, statements, views, and opinions included in this publication are based on sources (both internal and external sources) considered to be reliable, but no representation or warranty, express or implied, is made as to their accuracy, completeness or correctness. Such information, statements, views and opinions are expressed as of the date of publication, are subject to change without further notice and do not constitute a solicitation for the purchase or sale of any investment referenced in the publication.