A nation was stunned and its people devastated. The question of how it all happened is sure to linger for years to come. They all thought they had this one in the bag but that’s how the wrong kind of history is made: the most highly-paid soccer team in the world (England) was knocked out of the Euro Cup tournament in June by an Iceland team that was managed by a part-time dentist. Just like that. All mash and no bangers, all Posh and no spice, all Mickey Blue Eyes and no James Bond.

We wish we could be just as light-hearted about the other exit the Brits experienced during the same week. After all those years of bracing for Grexit, we end up getting Brexit. Just like a modern marriage (or family), the ones you love don’t want to stay and the ones you don’t want never leave. Isn’t it ironic? By now, everyone knows Brexit is a big deal but nobody knows how it’s going to play out. Despite the uncertainties surrounding all the possible paths Brexit might take, and the significant differences in the macro backdrop, we think our best guide is still the 1992 U.K. exit from the European Exchange Rate Mechanism (ERM).

The ERM was a managed floating exchange-rate system where each country’s currency was allowed to fluctuate within pre-specified bands. The Deutsche mark became the de facto reserve currency which meant Germany’s monetary policy was likely to be transmitted to the other member countries via currency pegs. The German Reunification in 1990 prompted huge government spending and fueled an acceleration in inflation. The German central bank responded by raising interest rates which strengthened the mark. The tightening effect spread through the currency pegs and made life very difficult for other countries like the U.K. and Italy, which were already reeling from their own economic problems. Convinced that the U.K. would not be able to keep the pound within the ERM band, speculators attacked the pound and, by the end of September 16, 1992, the U.K. was forced to exit from the ERM.

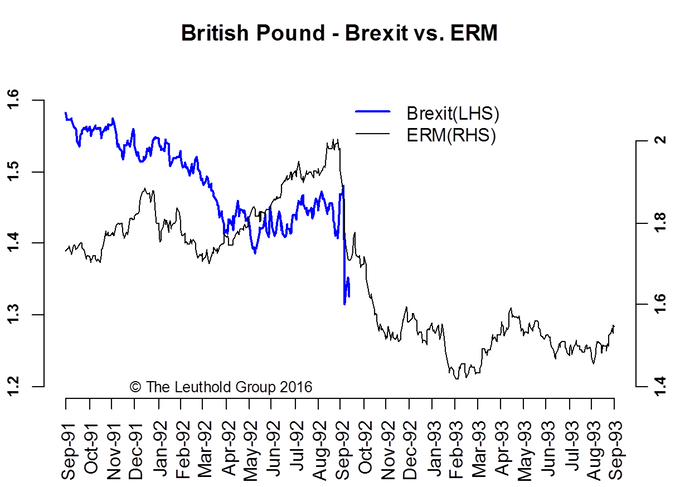

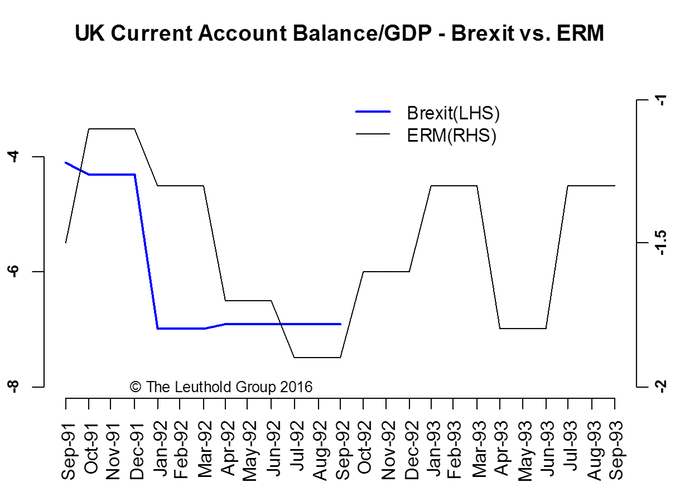

While the ERM exit was practically forced upon the U.K., Brexit is very much a self-inflicted wound. The initial market reaction was nonetheless similar with big drops in the pound in both cases (Chart 1). However, we think the pound is now fundamentally weaker than it was in 1992 as the U.K.’s current account deficit is now much bigger, at over 7% of GDP (highest among G10) versus 2% in 1992 (Chart 2). On the plus side, the pound is at a much cheaper level now than it was right before the ERM exit (close to 2). This could limit the downside going forward. Overall, we think the market action of the pound is consistent with an event of this magnitude and there is probably more room on the downside.

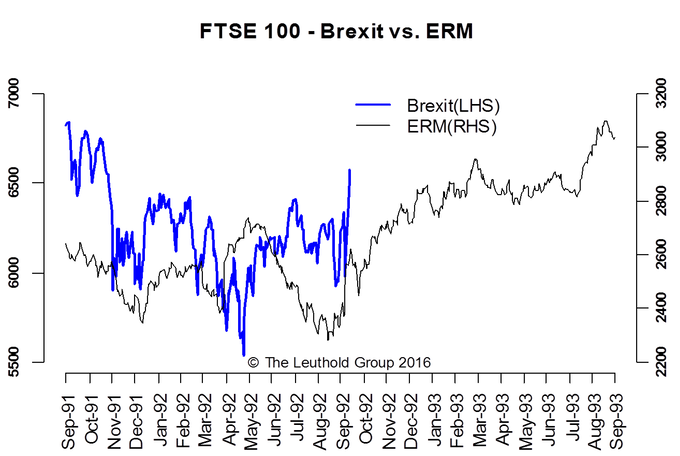

The sharp sell-off in U.K. stocks after the Brexit result was not a surprise, but the subsequent rally back above the pre-referendum level was a head-scratcher for many investors. A comparison with the market action around the ERM exit suggests there is more similarity than dissimilarity (Chart 3). The FTSE 100 index ended higher a week after the ERM exit and went on to even higher levels 12 months later. The market’s resilience seemed to support the “leave” camp’s claim that the negative impact of Brexit was vastly exaggerated by the “remain” camp.

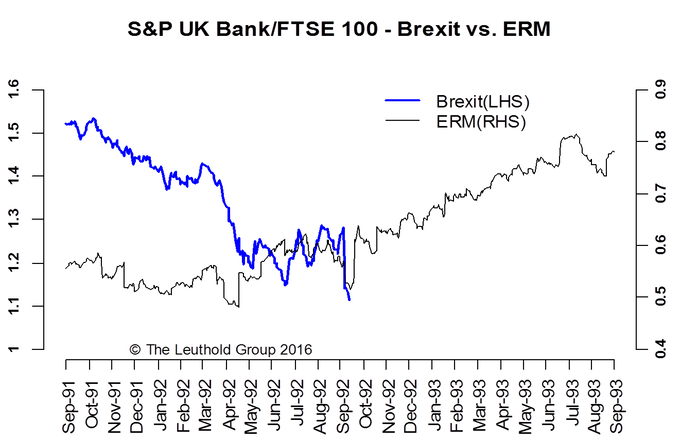

We think it’s way too early to draw any conclusion on this. One thing that dampens our enthusiasm about the rally in U.K. stocks is the lack of participation by U.K. bank stocks. We have long stressed the importance of bank stocks in gauging the durability of rallies and Chart 4 shows U.K. bank stocks made a new relative strength low while the FTSE 100 recovered all its losses. This was not the case in 1992: U.K. bank stocks never made a new relative strength low after the ERM exit.

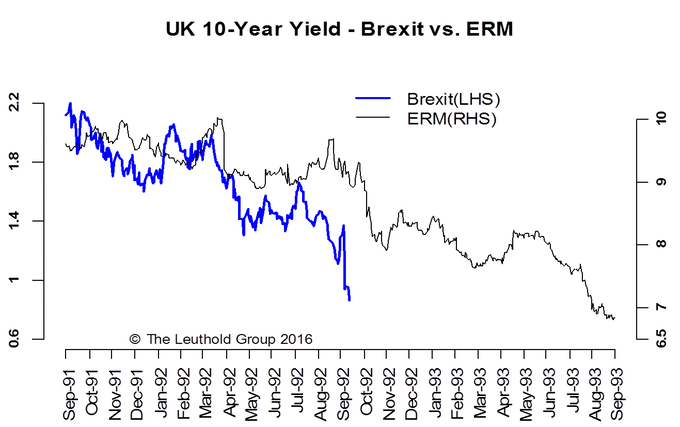

Apart from that, most U.K. assets (stocks, bonds, and properties) are more expensive now than they were back in 1992 and this makes the current situation more vulnerable to shocks. Nowhere is the valuation difference more obvious than in Gilts. The U.K. 10-year bond yield is currently below 80 bps while it was around 9% in 1992 (Chart 5). The fall in bond yield is consistent with the ERM experience as the market is trying to price in a higher likelihood of a U.K. recession and a much lower trajectory for long-term growth and inflation expectations. The picture for most developed bond markets looks the same—global bond yields made new all-time lows in June!

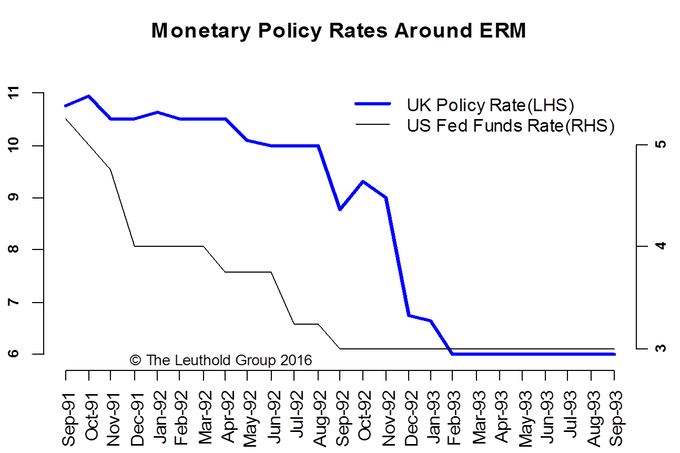

Much lower Gilt yields and a weaker pound also imply monetary stimulus is on the way. Indeed, the BoE already sent a strong signal for further accommodative policies this summer. The BoE policy actions after the ERM exit were very similar, with a string of aggressive rate cuts bringing the short-term rate down from 10% to 6% (Chart 6). The Fed, on the other hand, was near the end of its easing cycle in 1992 and still far away from a new tightening cycle. So the overall global policy picture was accommodative.

Right now, the biggest problem is not the easy policy stance, but the efficacy of the policy moves. At a meager 50 bps, the current U.K. policy rate doesn’t offer much room for rate cuts. With the market perception of negative rates and more QEs having turned negative, the critical question here is what else the central banks can do to stop a contagion when it happens.

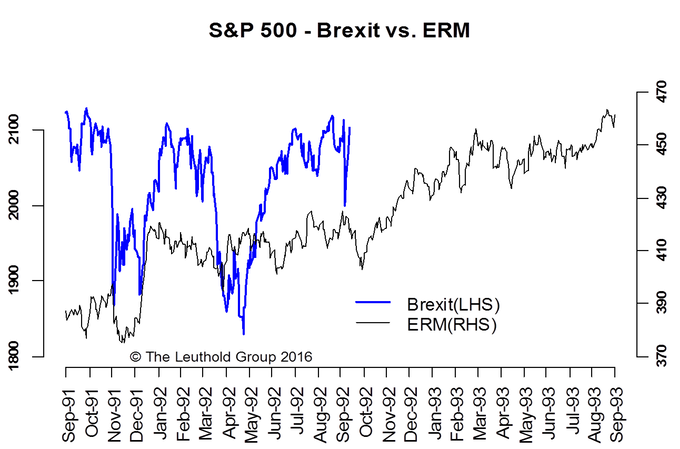

There are at least two kinds of contagion. The first one is market contagion, which seems to be contained so far. The ERM exit experience appeared to suggest that Brexit could be just another European issue and the rest of the world would be just fine. The S&P 500 was largely unaffected by the U.K.’s ERM exit and so far it has proven to be quite resilient after Brexit (Chart 7). But when we look at the macro context, the difference is quite clear. 1992 was at the start of a long bull market and a strong economic recovery. We are not in such an enviable phase of the cycle right now. More importantly, with global bond yields near double digits in 1992, there was plenty of fire power for central banks to provide support and stop contagion. Now, central banks are running out of options and the risk of policy back-firing is greater than ever. We believe bank stocks will likely bear the brunt of central bank policy errors and be the channel of market contagion. As we mentioned before, they are clearly under stress right now.

The other kind of contagion is political contagion, which is far more complicated. With the Euro-skeptic movement gaining momentum in several major European countries’ (France, Germany and the Netherlands) upcoming elections, the existential issue of the Euro-zone will certainly surface again. That is where Brexit poses more risk for the Euro-zone than for the U.K.

So the bottom line is: while post-Brexit market reactions have so far suggested a benign ERM-like experience, this is not the time to be complacent. The lack of central bank ammunition and the severe stress in bank stocks make the current situation quite vulnerable.