As we have mentioned in our recent pieces, investors are very conscious of the seen risks (especially exogenous risks) in the investment markets. Under the assumption that the seen risks are accurate and well known, let’s look at a few of the unseen risks in the stock and bond markets over the next two to three years which could frustrate investors.

- Investment markets may be built for an endlessly anemic economic recovery in the U.S. and interest rates are expected to stay low ad infinitum.

As a 36-year observer of the U.S. stock and bond market, I have witnessed the two lowest points of enthusiasm for U.S. economic growth in 1980-1982 and 2008-2016. In the early 1980’s, it was virtually impossible to see the cycle of double-digit inflation and sky-high interest rates breaking. The break in U.S. inflation from 11% in 1981 to below 4% in the mid-1980s and the drop in long-term Treasury Bonds from 15% to 7% by early 1987, were unseen. Today, it is hard to find an economist or stock market strategist who foresees a growth spurt in U.S. real gross domestic product (GDP). The implications are numerous, but we will cover two which affect our portfolio.

First, interest rates should move higher if we see growth rates above 3% in real GDP. If it happens in a swift way, this could lead to quick misery for bond investors who have lengthened maturities. We believe investors have exposed themselves to an unseen risk to obtain a small amount of additional yield. Market strategist Ray Devoe once said, “There has been more money lost stretching for yield than at the point of a gun!” This unseen risk could trigger large capital losses for investors who bought U.S. bonds as an alternative to negative rates in places like Germany and Japan.

Second, companies with great balance sheets and free-cash-flow could gain the historically normal benefit (long-term equity outperformance) from providing their own capital. Heavily indebted, lower-quality companies, especially in capital-intensive industries, should see profit margins decline at the hand of higher interest rates. The unseen risk of rising interest rates should give investors caution if they are looking at a poor balance sheet company. From an optimistic standpoint, if banks stick to lending to those who pay back their loans, the interest rate spreads would be refreshed by this unseen risk and insurance companies could find some yield for their investment portfolios.

- Computer science and software engineering backgrounds are an almost certain road to financial success for college graduates.

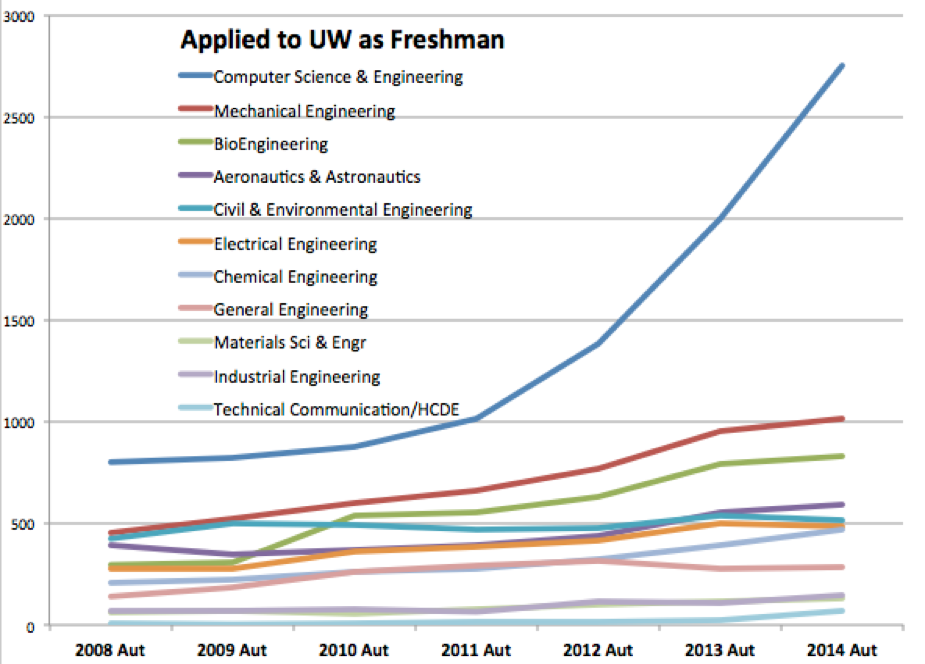

In May of 2014, Charlie Munger said, “Competition is the enemy of competence!” Computer science is arguably the most popular college major in Washington state, and possibly the rest of the country as well. The following comes from a recent article from GeekWire:1

“The chart above tells quite a story. That blue line — the one that looks like a hockey stick — shows how interest in computer science from freshmen at the University of Washington in Seattle has skyrocketed since 2010 compared with other engineering fields.”

“There were more than 850 students in UW’s introductory programming class last quarter. [...] Total enrollment in the past year was 2,700.”

“The UW is not alone. Countless other U.S. universities, from Harvard to Stanford to the University of Michigan, are seeing similar demand for computer science degrees.”1

Economics teaches us about the law of diminishing returns. Here is how one economics dictionary defines the theory:2

“A concept in economics that if one factor of production (number of workers, for example) is increased while other factors (machines and workspace, for example) are held constant, the output per unit of the variable factor will eventually diminish.”

This is the unseen risk of the boom in computer science degrees for both the individuals pursuing them and the vast array of technology companies hiring them to compete with each other. Bill Gates, Paul Allen, Steve Jobs and Steve Wozniak did not even have a college degree when they formed Microsoft and Apple. Munger would say that they had total competence from the lack of competition! The writer, Malcolm Gladwell, would say that they got their ten thousand hours in on the computer before everyone else did. The benefit of getting into computer science could be diminishing very quickly under Munger’s theory and the risk goes unseen, masked by the boom in technology and the huge gains in the most popular technology stocks.

When tech companies with strong revenue growth and very little in profits see their shares rocking and rolling, young people are very motivated to get in on the industry action. The unseen risk of capital destruction has followed historically, when a big part of the stock market’s capitalization gets tied up in the most glamorous stocks. One of the telltale signs has been young people craving a piece of the action. When oil was $115 per barrel a few years ago and the Bakken shale fields were booming, colleges offering a geological engineering degree were buried with applications. The unseen risk is being played out via the current oil price of $42 per barrel and layoffs which are rampant in the oil business. It would be amazingly frustrating to U.S. investors if the shares of today’s glam tech stocks do poorly, because the possibility of it, on an across the board basis, is unseen.

- Passive indexes have dominated most stock-picking methodologies and will do so forever.

We’ve seen estimates that 52% of the dollars invested in large-cap U.S. stocks are held in passive index vehicles. The index advantage is simple, seen and well documented. You get the market return (if you stay put) at a low cost by owning all the stocks in the S&P 500 on a capitalization-weighted basis. However, the risk in the index is currently unseen, because the index is aligned by its weightings and practices very low turnover (less than 5% per year over the last twenty years). Technology stocks are well over 20% of the S&P 500 Index and other than during the tech bubble are at the highest sector weighting and the biggest spread to the second largest sector as they have been since 1990. Historically, the index is at its worst when a prolonged era of success automatically allows proportional dominance from sectors which leave index investors with an unseen risk.3

It is not hard to figure out how to beat the index from a historical standpoint. Academic studies show that the cheap stocks in the index outperform the index over one, three, five and even seven-year time frames. Also, companies which fit certain quality characteristics, like strong balance sheets, sustainably high profits and low earnings volatility have proven to be long-duration winners. This has equated to our three main tenets of investing: 1) Valuation matters dearly; 2) We want to own businesses for a long time; 3) To do this we must own high quality businesses.

The most consistent unseen risk for index investors would be very poor performance in its largest sectors, and/or spectacular performance from industries which are very under represented. A negative feedback loop like this is what happened when the tech bubble broke in early 2000 and what happened to energy investments in 1981 and 2015. As an example, coming out of the bottom of the 2007-2009 bear market, banks were a very small part of the Dow Jones Industrial Average and restrained its results relative to the S&P 500 in 2009, when financials came storming back from extremely depressed price levels. If blue-collar trade-workers and the industries they work for make great money in a booming economy the next ten years, they are under-represented in the S&P 500 Index. If trades people out-earn those with a computer science degree, the unseen risk in technology stocks and the index will come to the U.S. stock market.

Warm Regards,

William Smead

1 Source: GeekWire, Analysis: The exploding demand for computer science education, and why America needs to keep up, http://www.geekwire.com/2014/analysis-examining-computer-science-education-explosion/

2 Source: Business Dictionary, http://www.businessdictionary.com/definition/law-of-diminishing-returns.html#ixzz4FcZ1rAWG

3 Source: Siblis Research, S&P 500: Sector Weightings, http://siblisresearch.com/data/sp-500-sector-weightings/

The information contained in this missive represents Smead Capital Management's opinions, and should not be construed as personalized or individualized investment advice and are subject to change. Past performance is no guarantee of future results. Bill Smead, CIO and CEO, wrote this article. It should not be assumed that investing in any securities mentioned above will or will not be profitable. Portfolio composition is subject to change at any time and references to specific securities, industries and sectors in this letter are not recommendations to purchase or sell any particular security. Current and future portfolio holdings are subject to risk. In preparing this document, SCM has relied upon and assumed, without independent verification, the accuracy and completeness of all information available from public sources. A list of all recommendations made by Smead Capital Management within the past twelve-month period is available upon request.

© 2016 Smead Capital Management, Inc. All rights reserved.

This Missive and others are available at www.smeadcap.com

Follow us on Twitter @SmeadCap