After five decades of influencing global oil prices, the Organization of the Petroleum Exporting Countries (OPEC) has lost its ability to act in a coordinated manner, in my view. This sets the stage for the US to become the world’s “swing producer” — the region that can most easily loosen or tighten its flow of oil in response to changing global demand.

Let’s take a look at how the industry got here, and what I expect to see going forward.

OPEC and oil prices: Not too high, not too low

OPEC was formed in 1960 to coordinate oil policies among its members. Today, there are 14 members: Algeria, Angola, Ecuador, Gabon, Indonesia, Iran, Iraq, Kuwait, Libya, Nigeria, Qatar, Saudi Arabia, United Arab Emirates and Venezuela.

Historically, OPEC has banded together to keep oil prices in its desired range — high enough to generate profits, but just low enough to keep out higher-cost producers in the US, Canada and elsewhere. In essence, OPEC set oil prices, and everyone else simply accepted them. But in recent years, two forces have worked together to disrupt OPEC’s modus operandi:

1. Saudi Arabia wants to keep production flowing.

Saudi Arabia — OPEC’s largest producer — has outlined a long-term agenda for economic growth. The Kingdom recently released a long-term plan to diversify its petroleum-focused economy into areas such as mining and tourism. In 2015, oil represented more than 70% of the government’s revenue, and leaders want to more than triple their economy’s nonoil revenue by 2020.1

But kick-starting new industries will take investment. Most likely, Saudi Arabia will need to generate as much oil revenue as possible today and direct that money into the development of these new industries — regardless of what that means for the rest of OPEC. From November 2014 to December 2015, while the price of oil fell by about 50%, OPEC’s production increased by 1.5 million barrels — fueled in large part by Saudi Arabia.2 The Kingdom’s desire to keep its wells flowing was reflected in OPEC’s recent failure to cap oil production during its June meeting in Vienna.

2. US shale plays have become competitive with OPEC

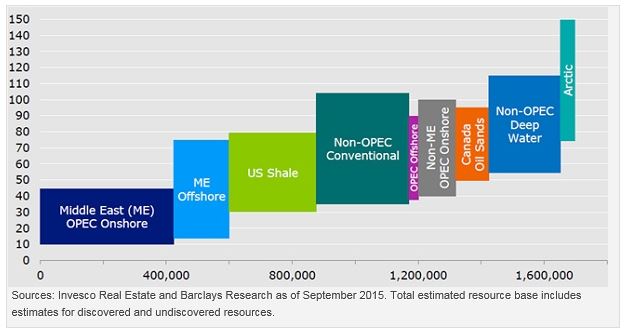

Technology has lowered the cost of US shale production to the point where it’s a viable competitor to OPEC, even at lower prices. The chart below shows how US shale compares with other major sources of oil. The width of the boxes measures the size of the estimated resource base, and the height illustrates the break-even oil price range needed to fund these projects.

As illustrated, onshore OPEC fields in the Middle East have the lowest break-even costs at $10 to $40 per barrel. US shale remains competitive in the higher part of that band, requiring an oil price of $30 to $80 per barrel to break even, depending on the project. Non-Middle Eastern OPEC projects actually have a higher break-even price than US shale, requiring $40 to $100 per barrel.

US shale projects are cost-competitive with most OPEC production

The horizontal axis represents the total estimated resource base (millions of barrels). The vertical axis represents the break-even oil price range ($).

The evolving role of the US

As an investor in global infrastructure and master limited partnerships, I see a lot to be excited about in the US energy space. Permits to drill in the Rockies have risen in early 2016, the Bakken shale play enjoyed relatively steady production throughout 2015, and production in the Permian Basin has actually increased dramatically since 2014.

Beyond the oil patch, the US has become a major exporter of propane and ethane and is poised to become a global force in liquefied natural gas (LNG), with 14 export terminals under construction and 11 more that have been proposed. Additionally, I expect the US to triple its natural gas exports to Mexico over the next 10 years via new pipelines.

Even with the recent commodity price correction, the US remains on the path of being a dominant global energy exporter, thanks in part to its relatively recent ability to stay cost-competitive with OPEC. I believe this trend should continue to provide investors with many opportunities across the energy and infrastructure spectrum.

1 Source: The Wall Street Journal, June 6, 2016, “Saudi Arabia approves plan to diversify economy”

2 Source: US Energy Information Administration as of January 2016

Important information

Businesses in the energy sector may be adversely affected by foreign, federal or state regulations governing energy production, distribution and sale as well as supply-and-demand for energy resources. Short-term volatility in energy prices may cause share price fluctuations.

The information provided is for educational purposes only and does not constitute a recommendation of the suitability of any investment strategy for a particular investor. Invesco does not provide tax advice. The tax information contained herein is general and is not exhaustive by nature. Federal and state tax laws are complex and constantly changing. Investors should always consult their own legal or tax professional for information concerning their individual situation. The opinions expressed are those of the authors, are based on current market conditions and are subject to change without notice. These opinions may differ from those of other Invesco investment professionals.

All data provided by Invesco unless otherwise noted.

Invesco Distributors, Inc. is the US distributor for Invesco Ltd.’s retail products and collective trust funds. Invesco Advisers, Inc. and other affiliated investment advisers mentioned provide investment advisory services and do not sell securities. Invesco Unit Investment Trusts are distributed by the sponsor, Invesco Capital Markets, Inc., and broker-dealers, including Invesco Distributors, Inc. PowerShares® is a registered trademark of Invesco PowerShares Capital Management LLC (Invesco PowerShares). Each entity is an indirect, wholly owned subsidiary of Invesco Ltd.

©2016 Invesco Ltd. All rights reserved.

Is oil patch influence swinging toward the US? by Invesco