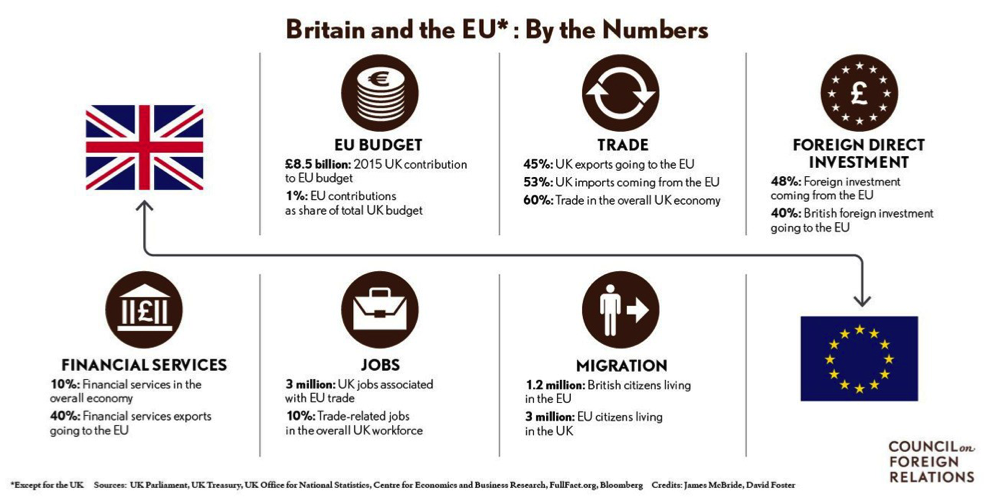

The second quarter of 2016 remained relatively quiet until June 24th when the citizens of the United Kingdom voted in a historic referendum to determine the country’s future within the European Union. The result: 52% of the population voted to leave while the remaining 48% voted to stay. The event, coined “Brexit”, sent shockwaves through the equity markets as the S&P 500® Index, the FTSE 100 and the ACWI ex-US fell -3.6%, -10.0% and -6.1% on June 24th respectively. Since then the markets have largely recovered in local terms, but does that indicate that the crisis has been averted? We will be the first to admit that we don’t know. It will take years for the United Kingdom to leave the European Union, and the truth is that the eventual outcome of Brexit is uncertain at best and unknowable at worst.

There are far too many connections between the United Kingdom and the European Union to discern how things may unfold. While it is natural to fear such uncertainty, we as investors must avoid succumbing to emotional decisions driven by fear. Naturally, it is turbulent times like these when we believe that a quantitative investment process rooted in a time-tested thesis, thoroughly examined across market and economic cycles, can help guide us into making prudent investment decisions. Emotion is often the enemy of long-term investment success, and correspondingly we divorce emotion from our investment decisions, which we believe will improve portfolio returns over time.

While we humans have no innate ability to predict the future, we believe examining some of the market’s major concerns is a useful exercise. Similar to other recent global panics, a major source of fear resides in the financial sector. The day after the vote, the MSCI Europe Financials Index fell -12.7% and was down -23.0% year-to-date at the end of the second quarter. This should come with little surprise considering London currently enjoys the number one spot on the Global Financial Centres Index. The Index is constructed through a combination of financial centre assessments and rankings of five instrumental factors: human capital, business environment, financial sector development, infrastructure, and reputational and general factors.

Source: 2016 Global Financial Centres Index 19, Published by the Z/Yen Group

It is difficult to foresee a situation where the United Kingdom exiting the European Union does not have a detrimental impact on the majority of the factors mentioned above. The resultant uncertainty puts further pressure on European Banks, many of which are still trying to recover from the 2008-09 Global Financial Crisis and the 2011 European Sovereign Debt Crisis. There will likely be tough choices ahead for many of these institutions as they navigate through more uncharted waters.

The United Kingdom’s largely domestic banks provide further insight into another of the market’s major concerns: the property market. Property prices in the United Kingdom have increased 20.4% in real terms over the past three years. In part, direct foreign investment from other countries in the European Union has driven these large price increases. If foreign direct investment begins to dry up it is a real possibility that housing prices could begin to head in the opposite direction. Investors have previously expressed concern over what seemed like unsustainable price increases and now Brexit has provided a catalyst for these investors to run for the exit.

The price movements of other property related assets supports this narrative. As of the end of the second quarter, the iShares UK Property UCITS ETF and the Bloomberg UK Homebuilder Index were down 14.91% and 32.34% respectively year-to-date. Adding to the panic, Standard Life Investments suspended trading in a £2.9 billion United Kingdom commercial real-estate fund as it was overwhelmed with redemption requests.

This brings us back to the most important question for U.S. based investors: how will this affect us? The primary risks at hand are that the United Kingdom’s exit could lead to the eventual breakup of the entire European Union, the entire United Kingdom, and/or that financial distress originating in Europe could spread through other developed economies. In an interconnected, global economy, these contagion risks are real but unlikely in anything short of extreme circumstances. A few market commentators have attempted to draw comparisons between this event and Bear Stearns closure of two hedge funds during the financial crisis in 2007. While it is too early to know for sure, we believe the fears of another global financial crisis unfolding are likely overdone. It is important to recognize these concerns but we caution against overreacting in light of the uncertainty. Remember, prior to Brexit the quarter was relatively calm. As a defensively oriented tactical manager, we believe our strategies can offer investors a certain peace of mind in uncertain markets. We will continue to monitor the situation vigilantly as it unfolds and make changes when our models deem them necessary. We thank you for your continued support and confidence in BCM.

Beaumont Capital Management [email protected] (844) 401-7699

investbcm.com

Disclosures:

Copyright © 2016 Beaumont Financial Partners, LLC. All rights reserved.

Past performance is no guarantee of future results. An investment cannot be made directly in an index. Index performance is shown on a gross basis. Strategy performance may be provided (as indicated) gross or net of the maximum applicable fee of 0.35% for the BCM Income Strategy and 0.50% for all other strategies. Actual composite net performance will vary due to the fees and expenses charged by the TAMP and Broker/dealer used, and other factors. For complete performance information, including fees and other expenses, investment minimums, etc. please contact your Regional Consultant or BCM at the number below.

This material is provided for informational purposes only and does not in any sense constitute a solicitation or offer for the purchase or sale of a specific security or other investment options, nor does it constitute investment advice for any person.

The material may contain forward or backward-looking statements regarding intent, beliefs regarding current or past expectations. The views expressed are also subject to change based on market and other conditions.

The information presented in this report is based on data obtained from third party sources. Although it is believed to be accurate, no representation or warranty is made as to its accuracy or completeness.

Diversification does not ensure a profit or guarantee against a loss. As with all investments, there are associated inherent risks including risk of principal. Stock markets, especially foreign markets, are volatile and can decline significantly in response to adverse issuer, political, regulatory, market, or economic developments. Sector investments concentrate in a particular industry and the investments’ performance could depend heavily on the performance of that industry and be more volatile than the performance of less concentrated investment options and the market as a whole. Foreign markets, particularly emerging markets, can be more volatile than U.S. markets due to increased political, regulatory, social or economic uncertainties. Fixed Income investments have exposure to credit, interest rate and inflation risk.

All BCM strategies invest only in long-only ETFs. ETFs are not typically actively managed, trade like stocks and are subject to investment volatility and the potential for loss. The principal amounts invested in ETFs are not protected, guaranteed or insured. An Exchange Traded Fund (ETF) is a security that tracks an index, a commodity or a basket of assets like an index fund, but trades like a stock on an exchange. ETFs experience price changes throughout the day as they are bought and sold.

The Beaumont Capital Management investment strategies may not be appropriate for everyone. Due to the periodic rebalancing nature of our strategies, they are not appropriate for those investors who need or desire monthly or quarterly withdrawals or who wish to make frequent deposits.

S&P 500, S&P Global ex-U.S. BMI, and SPDR are registered trademarks of Standard and Poor’s, a McGraw Hill company. MSCI is a registered trademark of MSCI INC. BlackRock is a registered trademark of BlackRock, Inc. DoubleLine® is a registered trademark of DoubleLine Capital LP.

The Standard & Poor's (S&P) 500® Index is an unmanaged index that tracks the performance of 500 widely held, large- capitalization U.S. stocks. The FTSE 100 Index is an index of the 100 companies listed on the London Stock Exchange with the highest market capitalization. The MSCI ACWI ex USA Index captures large- and mid-cap representation across 22 of 23 Developed Markets countries (excluding the US) and 23 Emerging Markets countries. The MSCI Europe Financials Index captures large- and mid-cap representation across 15 Developed Markets countries in Europe. All securities in the index are classified as members of the GICS financials sector. The Global Financial Centres Index (GFCI) was first published by the Z/Yen Group in March 2007. The aim of the GFCI is to examine the major financial centres globally in terms of competitiveness. The Bloomberg UK Homebuilder Index is comprised of homebuilders in the United Kingdom. This index is a modified market cap- weighted index, whose equities are capped at 15%. This index is a modified market cap-weighted index, whose equities are capped at 15%. The S&P Small-Cap 600 Index measures the small-cap segment of the U.S. equity market. The Barclay’s Capital Aggregate Bond Index, which used to be called the "Lehman Aggregate Bond Index," is a broad base index and is often used to represent investment grade bonds being traded in United States. The MSCI World ex USA Index captures large- and mid-cap representation across 22 of 23 Developed Markets countries--excluding the United States. The MSCI World Index captures large- and mid-cap representation across 23 Developed Markets countries. The S&P Global 1200 Index is an unmanaged index that tracks the performance of 1200 global stocks that make up 70% of the global stock market capitalization. The S&P Global ex-U.S. BMI Index is an unmanaged index that tracks the performance of 8000 all-capitalizations international stocks.

For Investment Professional use with clients, not for independent distribution. Please contact your Relationship Manager for more information or to address any questions that you may have.