Since the end of the financial crisis, management teams have aggressively bought back company stock. Buybacks have slowed from recent peak levels but activity remains robust. We think the practice can be shareholder friendly, but believe not all share repurchases are equal. While stock buybacks can be a key component of a balanced capital allocation strategy, it is important to know how purchases are being funded.

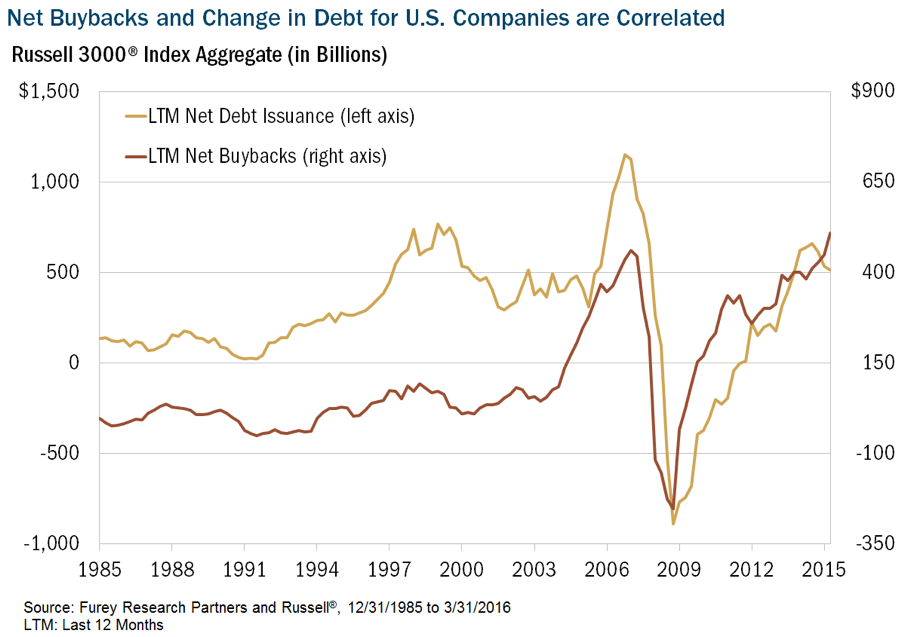

Over the past six-plus years, many CEOs have relied on the use of debt to buy back company stock. The move is appealing for executives, because it can boost results by reducing the number of shares that have a claim on earnings. However, it’s not necessarily appealing to value investors like us who want to see low debt levels.

In spring, we were encouraged by a growing weariness toward the practice as companies with the most debt lagged the broader benchmark and were among the worst performers. But as the prospect of near-term higher rates has fizzled, so too has caution from investors toward leverage. With the threat of higher rates seemingly off the table for now, management teams have gone back to this old trick. We think it is short-sighted and prefer seeing share buybacks that are funded by free cash flow. Our reasons are two-fold: 1) it can unnecessarily add financial risk to company balance sheets, and 2) it paints a distorted picture of a company’s financial results.

Disclosure:

Past performance does not guarantee future results.

The statements and opinions expressed in this article are those of the presenter(s). Any discussion of investments and investment strategies represents the presenter’s views as of the date created and are subject to change without notice. The opinions expressed are for general information only and are not intended to provide specific advice or recommendations for any individual. Any forecasts may not prove to be true. Economic predictions are based on estimates and are subject to change.

Investing involves risk, including the potential loss of principal. There is no guarantee that a particular investment strategy will be successful. Value investments are subject to the risk their intrinsic value may not be recognized by the broad market.

Definitions: Free Cash Flow: is the amount of cash a company has after expenses, debt service, capital expenditures, and dividends. The higher the free cash flow, the stronger the company’s balance sheet. Net Debt: is a metric that shows a company's overall debt situation by netting the value of a company's liabilities and debts with its cash and other similar liquid assets. Russell 3000® Index: is a market capitalization weighted equity index maintained by the Russell Investment Group that seeks to be a benchmark of the entire U.S. stock market and encompasses the 3,000 largest U.S.-traded stocks, in which the underlying companies are all incorporated in the U.S. All indices are unmanaged. It is not possible to invest directly in an index.

Russell Investment Group is the source and owner of the trademarks, service marks and copyrights related to the Russell Indexes. Russell® is a trademark of Russell Investment Group.

CFA® is a registered trademark owned by the CFA Institute.

©2016 Heartland Advisors

2016360