During the ‘Death Throws” of Apartheid in South Africa in the early 90s a common term came about - Third Force or Third Rail.

A seemingly invisible violent faction emerged during political protests to cause havoc and destruction and then mysteriously disappeared.

The big question was who was this Third Force? Who did they answer to? And who was funding them?

In the fullness of time … and there is always a fullness of time ... the truth emerged.

The Third Force was a clandestine network of security and ex-security force operatives of the Apartheid Government arming factions of the Zulu nation to subterfuge and disrupt the ANC’s march to power.

The animosity between the proud Zulu nation and other indigenous nations of South Africa is well documented and precedes colonial times by hundreds of years.

It seems that a Third Rail can be found in a lot of situations, sometimes violent other times not. Always with the goal of manipulating events from behind the curtains.

Democratic National Committee

Take for example the recent revelations of the Democratic National Committee or DNC:

In a real twist of irony, the nefarious shadow deeds of the DNC - influencing the choice of the Democratic Nominee (the DNC is supposed to remain neutral in this matter) - was revealed by an equal but opposite shadow from the murky world of WikiLeaks! Apparently, per Wikileaks themselves there is more to come on that …

Central Banking

In the financial markets we often feel as if the network of Central Banks acts as an invisible force … not always transparent and not always accountable!

We note that a bubble tends to be invisible to those inside it. And in our estimation the seven-year suppression of interest rates has caused one of the biggest bubbles of all by forcing investors to seek income from instruments other than traditional bonds.

In our 2016 market forecast we said this would be the year (finally) for higher rates

Boy!

That one sure looks like a bust right now.

Rates have moved steadily lower during the first 7 months of 2016 as global growth estimates have fallen and Q2 GDP numbers came in lower than expected.

As the world became familiar with negative interest rates another bullish refrain was the relative yield advantage of US Treasuries over foreign Sovereigns. [GS: Taking currency hedging costs into account we now think that relative advantage is over!]

All the while CPI has been coming in above expectations driven primarily by healthcare and rents. And quite possibly if it wasn’t for BREXIT the Fed may have already raised rates.

Is the Fed itching to raise rates before inflations laps onshore or is it merely lip service?

You will recall the last rate rise in December 2015 caused the markets to have a fit so we are fairly confident in saying the entire financial world is now priced at or near a 0.25% global risk free rate.

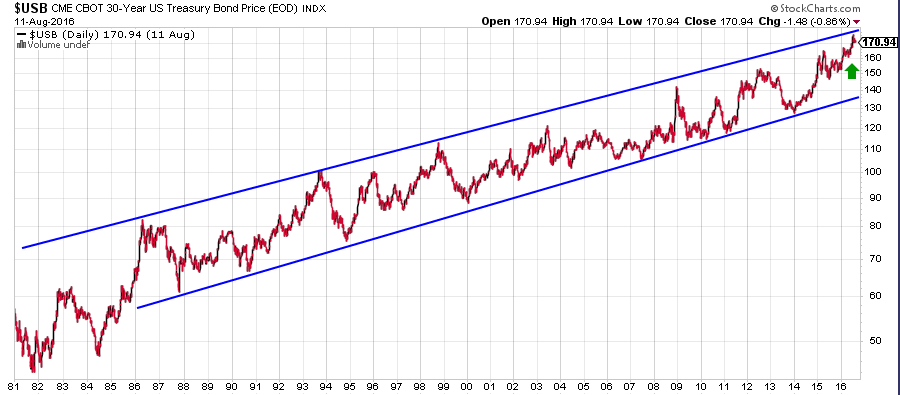

Our prediction of higher rates was primarily based on the price channel of the 30-yr below.

We said there was no need for a secular bear market to occur but merely a reversal from the channel top to the bottom in the normal course of a market inhaling and exhaling. As serous students of the markets would correctly point out, previous Bond secular bear markets, interest rates, simply don’t reverse higher. They form a base at low levels for years and years - perhaps even decades before they begin the long winding course higher.

Figure 1 - 30 Year US Bond Price Channel (lower price equals higher rates)

In addition to uncomfortably high(er) CPI numbers, perhaps the elephant in the room conspiring for higher rates would be Pension Funds.

It seems as if a crisis is brewing here because of their inability to generate returns high enough to cover future liabilities:

WSJ 07-26-16 “Pension Returns Slump, Squeezing States and Cities Long-term returns for U.S. public pensions are expected to drop to the lowest levels ever recorded. The dip is intensifying a national debate over whether states and cities can continue to afford pension obligations, as the soaring costs are squeezing budgets across the U.S. ‘Many states and local governments may be facing difficult choices if investment returns remain low’, said Keith Brainard, research director at the National Association of State Retirement Administrators. ‘The money has to come from somewhere.” --- GS: low Bond returns

And …

Cal Coast News July 25, 2016 - “CalPERS earned a return on its investments of just .6 percent in the last fiscal year, marking the state retirement fund’s worst performance since 2009.”

As with most bubbles this one will also end badly and many investors will find that the term’ Bond substitute’ is not exactly what it was purported to be especially when challenged in a court of law.

When may this occur?

Again we have been forecasting higher rates for most of this year. And perhaps the turning point is occurring now. Or perhaps the Fed will wait until after the elections in November when it may be more politically palatable to raise.

We wait to see what emerges from the shadows!

---

Greg Silberman is the Chief Investment Officer of Atlanta Capital Group Investment Management [ACGIM]. Atlanta Capital Group Investment Management specializes in creating custom private market solutions for RIA/Family Office clients.

Advisory Services offered through Atlanta Capital Group Investment Management.

Nothing in this article should be interpreted as a recommendation to buy any security. Please conduct your own due diligence.