An Investment Only a Mother Could Love: The Case for Natural Resource Equities

Executive Summary

■ We believe the prices of many commodities will rise in the decades to come due to growing demand and the finite supply of cheap resources.

■ Public equities are a great way to invest in commodities and allow investors to:

■ Gain commodity exposure in a cheap, liquid manner

■ Harvest the equity risk premium

■ Avoid negative yields associated with rolling some futures contracts

■ Resource equities provide diversification relative to the broad equity market, and the diversification benefits increase over longer time horizons.

■ Resource equities have not only protected against inflation historically, but have actually significantly increased purchasing power in most inflationary periods.

■ Due to the uncertainty surrounding, and the volatility of, commodity prices, many investors avoid resource equities. Hence, commodity producers tend to trade at a discount, and they have outperformed the broad market historically.

■ While resource equities are volatile and exhibit significant drawdowns in the short term, over longer periods of time, resource equities have actually been remarkably safe investments.

■ By some valuation metrics, resource equities have looked extremely cheap throughout 2015 and the first half of 2016, and that may bode well for future returns.

■ Given the difficulty in predicting commodity prices, the low valuation levels of the past year and a half may be unjustified.

■ Despite all of this, investors generally don’t have much exposure to resource equities. Typically, they don’t have large specific allocations to resource equities, and the broad market indices don’t provide much exposure to the commodity producers. The S&P 500’s exposure to energy and metals companies has dropped by more than 50% over the last few years, and the same is true of the MSCI All Country World Index. Those investing with a value bias may be particularly underexposed to resource equities, as value managers tend to be especially averse to the risks posed by commodity investing.

Introduction

Jeremy has written extensively about the long-term prospects for natural resources,1 but there are advantages to commodity investing beyond potential commodity price appreciation, including diversification and inflation protection. Resource equities are a great way to gain commodity exposure, while also accessing the equity risk premium. Given their somewhat hybrid nature, with one foot in the equity market and the other foot in the commodity market, resource equities display some unusual characteristics; over various timeframes, resource equities may move more with equities or more with commodities and can look more or less risky than the broad market. Perhaps due to their quirky nature, resource equities are generally unloved and possibly misunderstood. However, we believe that resource equities present a compelling investment opportunity, both strategically and tactically, and that long-term investors could benefit from larger allocations to these assets.

Why Access Commodity Exposure via the Public Equity Market?

The equity risk premium is critical

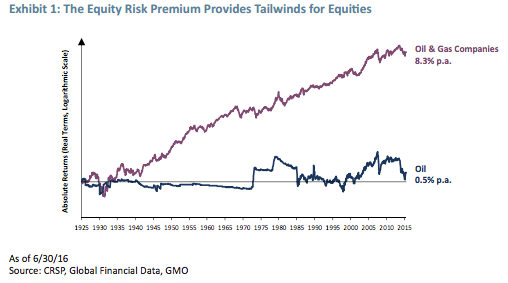

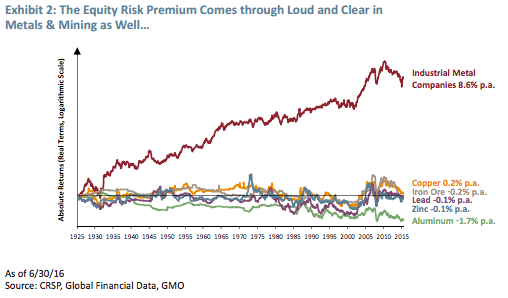

The equity risk premium is the main reason for preferring the equity markets to other means of gaining commodity exposure. Exhibit 1 shows that while oil prices have risen just slightly in real terms since the 1920s, oil and gas companies have generated real returns of more than 8% per year. That’s a pretty healthy equity risk premium. The industrial metal miners have similarly outperformed the underlying metals (see Exhibit 2). The public equity market has clearly been far superior to direct commodity investment historically, and that’s not even taking into account the storage and transportation costs, perishability issues, etc., associated with direct commodity investment.

The problem with commodity futures

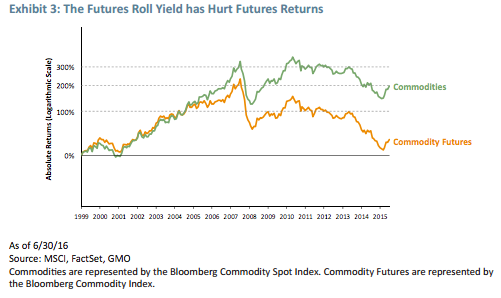

Many investors look to the futures market for their commodity exposure. However, futures investors contend with the futures roll yield when they sell out of an expiring contract and roll into a longerdated contract. When futures curves are in contango, or upward sloping, there’s a drag associated with selling out of the cheaper near-term contracts and buying the more expensive longer-dated contracts. “Sell low, buy high” is generally not a sound investment practice, and it turns out it hasn’t worked out well for investors in the commodity futures market over the past decade or so. Since 2000, commodities, as represented by the Bloomberg Commodity Spot Index, have gone up by almost 200%. However, this is a theoretical return reflecting the return you would have received if you could have bought commodities at spot prices without incurring the costs associated with dealing with the physical commodities. The investable index, the Bloomberg Commodity Index, covers the same basket of commodities and is implemented via the futures market. As Exhibit 3 shows, investing via the futures ate away at almost the entire commodity return.

Additional benefits to equities

The equity risk premium and futures roll yield are the two main factors that push us toward equities, but there are other additional benefits to equities as well. Public equities tend to be liquid and cheap to trade, and the public equity market offers a diverse set of business models that offer exposure to natural resources. Furthermore, the ability to value and select stocks within resource equities can yield additional returns.

What about private equity?

Private equity shares many of the benefits of its public brethren and seems like a reasonable alternative if you like fees and illiquidity…but we don’t! Complicating matters, all privates are not created equal; it can be difficult and time-consuming to identify the few private equity managers who really add value, and often the good ones are closed to new investment. Locking capital up at high fees with managers who generally don’t add real value gives us pause, especially given the transparency issues involved with private investment. And while complacency regarding liquidity may be normal in a world where central banks are doing everything they can to support asset prices, one need only look back to 2008 for a reminder of how important liquidity can be when you really need it. At the very least, public resource equities seem like a great complement to a private equity program and, in our view, public equities should make up the core of a resources allocation.

The Strategic Case for Investing in Resource Equities

Commodities have long been of interest to investors due to two important benefits: diversification and inflation protection. We will briefly examine whether investors in resource equities have experienced these benefits and review other potential strategic benefits of investing in commodity-linked equities.

Diversification

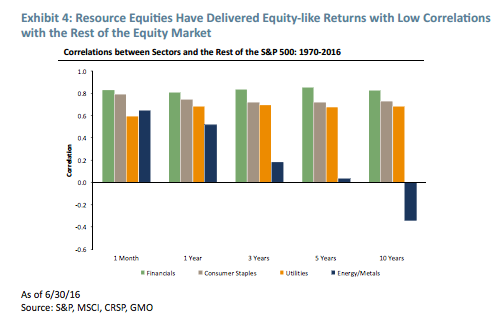

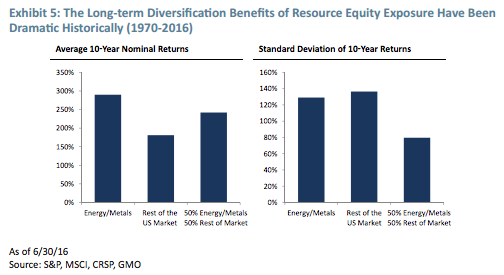

Let’s start by looking at whether investing in resource equities has provided diversification benefits. Exhibit 4 shows the correlations between various sectors and the rest of the market over varying timeframes.2 Looking at correlations of monthly returns, annual returns, etc., all the way out to 10- year return correlations can provide some insight into how sectors move with the broad market over various time periods. All four sectors examined here have been highly correlated with the rest of the market on a monthly basis. However, while Financials, Consumer Staples, and Utilities have maintained these high correlations over longer periods of time, the correlations for a basket of energy and metals companies with the rest of the market are very low by the time you look at 3- to 5-year returns, and the 10-year correlations have actually gone negative! There aren’t enough non-overlapping 10-year periods for the 10-year correlations to be statistically significant, but we believe there is intuition for the negative correlations: Rising resource prices are a drag on the rest of the economy, whereas falling resource prices are a boon for the economy.

Think about the implications of this for a moment. Here’s an investment that delivers equity-like returns with low to negative correlations with the broad equity market over long periods of time. Hedge fund investors generally accept lower-than-equity returns in order to gain access to uncorrelated returns, so getting equity returns with low to negative correlations should be very exciting. In fact, it’s not obvious that you need to know anything else in order to get excited about investing in commodity producers.

To illustrate the impact of these diversification benefits, let’s consider the long-term returns of a monthly rebalanced portfolio comprised of 50% energy and metals companies and 50% the rest of the US market (see Exhibit 5). Note that the standard deviation of the 10-year returns for a blended 50/50 portfolio is dramatically lower than either of the individual components.3 This is the beauty of diversification: Historically, investors have been able to boost returns and significantly reduce long-term volatility by adding resource equity exposure to their equity portfolios.

Inflation protection

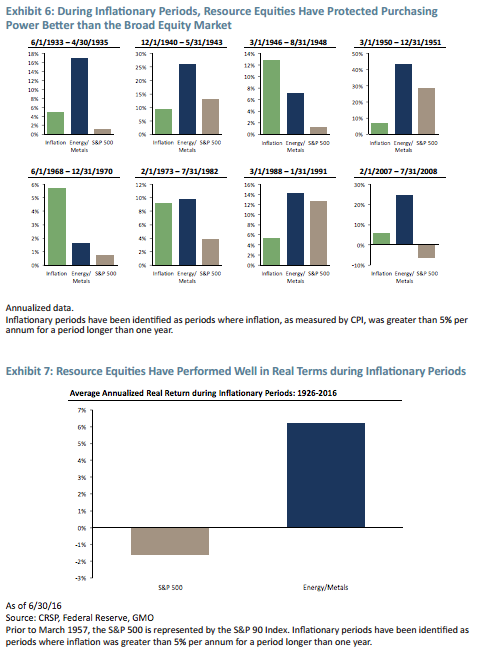

Inflation protection is another highly desirable trait for an investment, so let’s look at how resource equities have fared during inflationary environments. In the US, we’ve identified eight periods of time where inflation, as measured by CPI, was more than 5% per year for a period of one year or longer. In those inflationary periods, a basket of energy and metals companies kept up with or beat inflation six out of eight times, and in all eight periods the commodity producers outperformed the S&P 500 (see Exhibit 6). In fact, the commodity producers delivered real returns of more than 6% per year on average during these inflationary periods, as compared to a destruction of purchasing power of around 1.6% per year for the S&P 500 (see Exhibit 7).

We believe unexpected inflation risk is one of the two big risks that long-term investors face, along with depression risk. Historically, resource equities have not only protected against inflation, but have actually dramatically increased purchasing power during inflationary periods. As such, one might expect people to pay up for the inflation protection, just as hedge fund investors pay up for diversification by accepting lower expected returns. However, resource equities provide both diversification and inflation protection, and it turns out they can typically be bought at a discount.

Resource equities typically trade at a discount

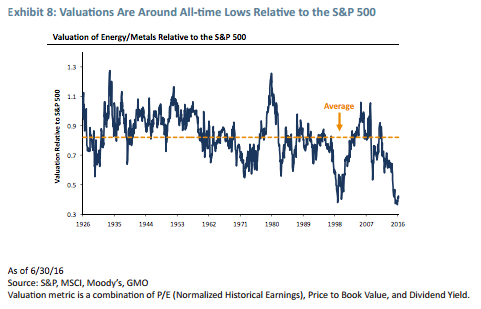

Based on a composite valuation metric composed of price to normalized earnings, price to book value, and dividend yield, commodity producers have traded at around a 20% discount to the S&P 500 on average since the 1920s (see Exhibit 8). Rather than focusing on the benefits of resource equities, investors are understandably uncomfortable with the wild, unpredictable swings of the industry, driven by over-/underinvestment cycles, supply disruptions, and unexpected changes in demand, among other factors. For those with relatively short timeframes, the boom/bust nature of commodity investing can be untenable. From its peak in April 2011, the MSCI ACWI Commodity Producers Index fell 54% through its trough in January of this year; and this in an equity market that was up almost 15%! With huge swings like that in the offing, our old friend career risk looms front and center. It’s not hard to see why professional investors worried about their livelihoods would be reluctant to play this game.

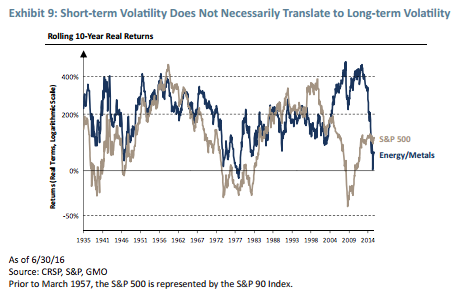

However, for investors willing to weather the shorter-term storms, resource equities have actually been remarkably safe investments. Over 10-year periods, the real returns for resource equities have been surprisingly stable (see Exhibit 9). Commodity producers have almost never delivered negative real returns over a 10-year period, and when they have, the losses of purchasing power have been minimal. This is an impressive enough finding in and of itself, but when compared to the stalwart S&P 500, it’s rather astonishing. The S&P 500 has gone down in real terms over many 10-year periods, often by large amounts; our unloved basket of energy and metals companies has actually been a much safer long-term investment.

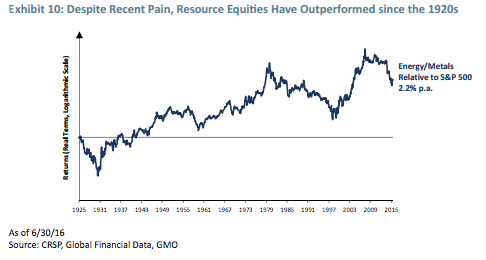

Long-term investors should always be on the lookout for opportunities where tolerating short-term underperformance enables long-term outperformance, and this is perhaps such an opportunity. As Exhibit 10 shows, our energy and metals basket has outperformed the broad market by more than 2% per annum over the past 90 years or so, even after the historic commodity collapse of the last few years. The ability to buy commodity producers at a discount due to their short-term riskiness may be yet another attractive feature of resource equity investing.

The Tactical Case for Investing in Resource Equities

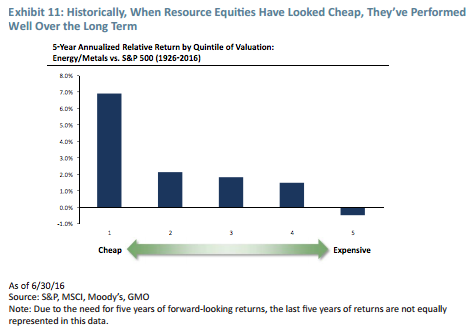

Given the uncertainty in the direction and level of commodity prices, especially in the short to medium term, the tactical case for investing in resource equities will never seem as strong as the strategic case. Yet, valuation levels for our basket of energy and metals companies relative to the S&P 500 have gotten to historic lows in recent months, at least by some valuation metrics4 (see Exhibit 8). The valuation metrics in the composite valuation used for Exhibit 8 (price to normalized earnings, price to book value, and dividend yield) are obviously imperfect, but it is interesting nonetheless to look at how resource stocks have performed historically at varying levels of valuation. When valuations relative to the market have been in the cheapest quintile of history, the commodity producers have outperformed the broad market by almost 7% per annum over the next five years on average (see Exhibit 11). Given that valuations continue to hover around all-time lows, at this time resource equities are firmly entrenched in the cheapest quintile of history relative to the broad market.

Whenever a group of securities trades near all-time lows, there will be a lot of bearishness. In recent months, the outlook for commodity prices has been decidedly bearish with many suggesting that oil could fall as low as $20/barrel or that iron ore and copper will stagnate for many years to come. If this bearish sentiment is justified, then the commodity producers are not as cheap as our valuation metrics would indicate. Thus, it’s important to think about how much insight people really have regarding the future of commodity prices.

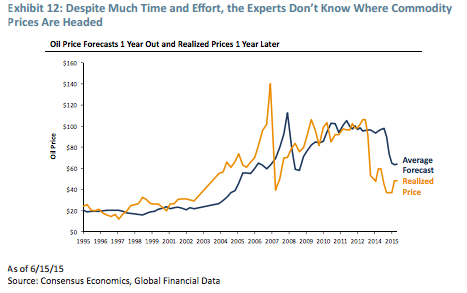

As one way of testing the ability to predict commodity prices, let’s look at oil forecast efficacy historically. Exhibit 12 shows the average one-year oil forecast from leading commodity analysts compared with the realized oil prices one year later. On average, the forecasts ended up being more than 30% off from realized prices. In fact, the experts got the direction right only a little better than half the time. We wanted to look at whether some analysts have been better or worse than others, so we ranked analyst forecasts for each period and ran rank correlations of each time period against all other time periods. If some analysts had been consistently better at forecasting oil prices than others, we would have expected to see at least modestly positive correlations. However, it turns out that the average rank correlation has effectively been zero (technically, 0.025). In other words, the experts were all equally bad at forecasting oil prices.

One-year forecasts are pretty short-term though. Have the expert forecasts been any better for longer periods of time? We only have access to longer-term forecasts for oil starting in 2011, so we can at least anecdotally look at the efficacy of somewhat longer-term forecasts. With oil at $91 in October 2011, the average forecast from 14 industry experts for the end of 2015 was $106; the minimum forecast was $88, and the maximum forecast was $137. At the end of 2015, oil checked in at $37 per barrel, far below even the most pessimistic forecast. And we’ve seen similar forecasting accuracy for copper, iron ore, and other commodities. One could reasonably conclude that even the experts have no idea where commodity prices are headed.

Given the difficulty in predicting commodity prices, it’s fair to wonder whether the bearishness surrounding this space in recent months is justified. In a world where the bearish sentiment surrounding commodities may be either unjustified or just outright wrong, the current valuations should at least get your attention.

A Quick Note on Agriculture

The shrewd reader may have noticed that we have completely ignored agriculture throughout this paper. This is due purely to the relatively short and sparse data set available for studying agricultural companies. In recent years, however, a variety of new entrants to the agricultural public equity scene have given investors some options. Nowadays, in addition to some traditional farming plays, the public equity markets offer diverse business models for gaining exposure to agriculture, including eco-chemical/seed companies, fertilizer companies, timber REITs, irrigation companies, and even fish farming plays.

It goes without saying that food is critically important and that feeding the fast-growing world population will be a challenge in the decades to come. Growing enough food will be complicated by soil erosion, a pernicious problem that becomes exponentially worse with heavy rains and flooding, both of which are likely to become more commonplace as climate change continues its inexorable march. Increasingly common and severe droughts, also associated with the changing climate, will put further pressure on the ability to grow crops. Long story short, don’t neglect agriculture when investing in natural resources.

Allocating to Resource Equities

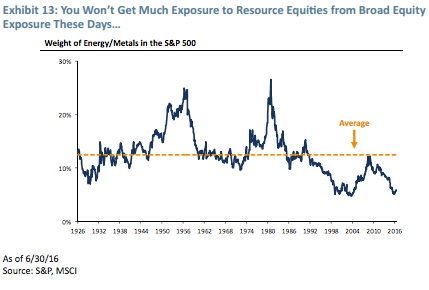

Despite the strong case for investing in resource equities, many investors rely on their broad equity exposure to gain access to commodity producers. This may have been a more effective strategy in the past when commodity producers made up a larger portion of the global equity market. However, after the collapse in commodity prices over the past few years, commodity producers, typically almost 13% of the S&P 500, have dropped to around 5% (see Exhibit 13). Similarly, the MSCI All Country World Index’s exposure to energy and metals companies has dropped by more than 50% over the last few years. And those with a value bias to their portfolios may not even have as much as the broad indices, as many value managers are averse to investing in companies with large exogenous risks like commodity price risk. The group of highly respected value managers that we track has generally been significantly underweight the commodity producers.5

Some investors gain additional exposure to commodities as part of their allocations to real assets. However, allocations to real assets are generally rather small, typically ranging from 5% to 15% of the overall portfolio, and real estate, infrastructure, etc., usually eat up a significant chunk of the real asset program. In light of the case we have made in this paper, it seems reasonable to conclude that a more substantial allocation to resource equities would be prudent for long-term investors seeking strong returns, diversification, and inflation protection.

Conclusions

We believe the case for investing in resource equities is compelling. Historically, investors in resource equities have enjoyed strong returns, along with diversification and inflation protection benefits. Investors in resource equities also gain exposure to global growth and potential commodity price appreciation. From a more tactical perspective, valuations have been hovering around historic lows relative to the broad market, and when resource equities have been cheap relative to the broad market historically, they’ve performed quite well going forward. Yet, investors are still wary of investing in commodity producers due to the commodity price risk and the always uncertain commodity outlook. Long-term investors willing to tolerate that shorter-term risk should strongly consider whether they have allocated enough to this exciting and unloved segment of the market.

1 Including, but not limited to, “Living Beyond Our Means: Entering the Age of Limitations,” “Initial Report: Running Out Of Resources,” “Time to Wake Up: Days of Abundant Resources and Falling Prices Are Over Forever,” “The Race of Our Lives,” “The Beginning of the End of the Fossil Fuel Revolution (From Golden Goose to Cooked Goose),” and “Always Cry Over Spilt Milk.”

2 Note that many of the exhibits in this paper start in the 1920s, whereas Exhibits 4 and 5 start in 1970. Oil prices were largely fixed in the decades leading up to the 1973 oil crisis driven by the OPEC embargo. Correlations and volatilities covering time periods where oil prices were fixed don’t seem particularly relevant to the world we live in today.

3 It’s also interesting to note that the basket of energy and metals companies actually displays a lower standard deviation of 10-year returns than the rest of the market, despite delivering monthly volatility more than 30% higher than the rest of the market over the same period.

4 Absolute valuation levels for the energy/metals basket have also reached historic lows in recent months on the same valuation metric.

5 Over the past decade, our basket of respected value managers has had approximately half as much exposure to commodity producers as the broad equity market on average.

Lucas White is a member of GMO’s Focused Equity team. Previously at GMO, he served in other capacities, including portfolio management for the Global Equity team and leadership of strategic firm-wide initiatives. Prior to joining GMO in 2006, he worked as a programmer and analyst for Standish Mellon Asset Management. Mr. White earned his B.A. in Economics and Psychology from Duke University. He is a CFA charterholder.

Jeremy Grantham co-founded GMO in 1977 and is a member of GMO’s Asset Allocation team, serving as the firm’s chief investment strategist. Prior to GMO’s founding, Mr. Grantham was co-founder of Batterymarch Financial Management in 1969 where he recommended commercial indexing in 1971, one of several claims to being first. He began his investment career as an economist with Royal Dutch Shell. He is a member of the GMO Board of Directors and has also served on the investment boards of several non-profit organizations. He earned his undergraduate degree from the University of Sheffield (U.K.) and an MBA from Harvard Business School.

Disclaimer: The views expressed are the views of Lucas White and Jeremy Grantham through the period ending September 2016, and are subject to change at any time based on market and other conditions. This is not an offer or solicitation for the purchase or sale of any security and should not be construed as such. References to specific securities and issuers are for illustrative purposes only and are not intended to be, and should not be interpreted as, recommendations to purchase or sell such securities.

Copyright © 2016 by GMO LLC. All rights reserved.

© GMO