No. We are not going to talk about Donald Trump. There are plenty of other disappointments to occupy ourselves with. Chief among these was the hesitant, half-a$$ stimulus package Japan put together in July. Like a bride in a pre-arranged marriage, Kuroda did the minimum to get Abe off his back. The market wanted a lot more because the match-maker, our own Ben Bernanke, stoked high expectations for helicopter money after his private meetings with both Abe and Kuroda. In the end, only a drone showed up.

Abe tried to leverage his surprising win in the Upper House election by promising a new fiscal stimulus that turned out to be a lot more fluff than stuff. The double disappointments only served to reinforce the loss of faith in Japan’s policy efficacy. Make no mistake, doubt about the success of Abenomics has been there for quite some time. Chart 1 shows a dramatic change in the market perception of the BoJ’s policy since the start of Abenomics. The market put a lot of faith in the BoJ between 2012 and 2015, evidenced by a weaker yen and lower Japanese bond yields. But since 2015, the relationship between the yen and Japanese bond yields has flipped to the good old Japanese way where the deflationary mindset drives the yen stronger and bond yields lower.

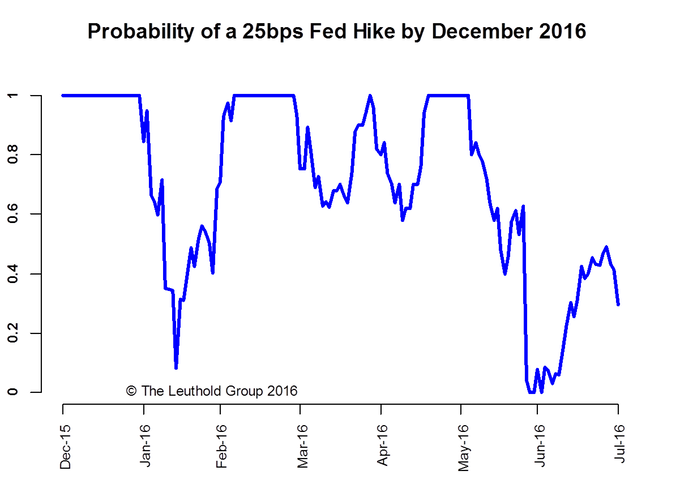

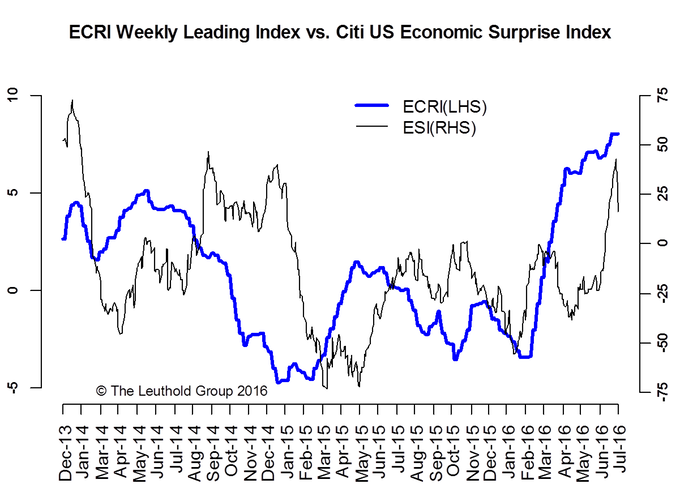

To be fair, the BoJ is not the only central bank that suffers from credibility issues. The Fed has changed its tone just about every other month this year and, along with external risk events (like Brexit) and frequent data hiccups, the market pricing of a December rate hike has changed dramatically over the last few months (Chart 2). The probability of a rate hike this year now sits around 35% and this is truly remarkable considering that the S&P 500 just made a new all-time high and overall U.S. macro-economic data has just had the best streak in a year. In fact, July was the first month since early 2015 that the Citi U.S. Economic Surprise Index (ESI) was significantly above zero (Chart 3).

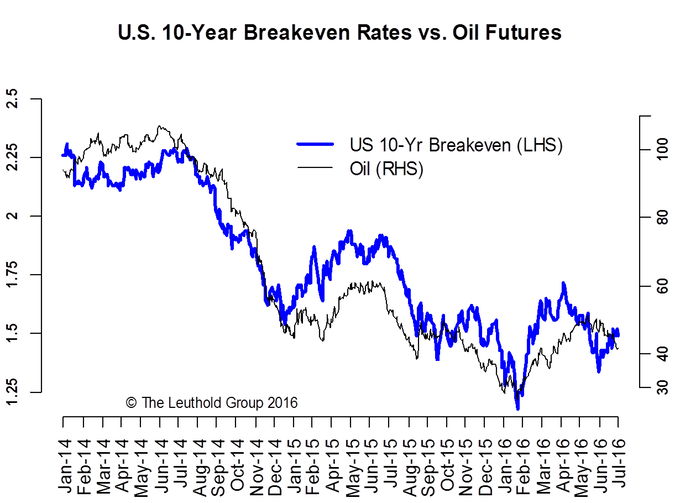

Having said that, the big miss in the latest Q2 GDP numbers has snapped the uptrend in the ESI index. On top of that, recent weakness in oil prices started to bring back memories of 2015. The 20% drop in oil prices so far has not negatively impacted oil-sensitive assets like credits, emerging markets or inflation break-even rates (Chart 4). But we believe a pain threshold will likely be crossed fairly soon if oil goes down further from here. In other words, there will always be more things for the Fed to worry about and more reasons to keep the rate hike on hold.

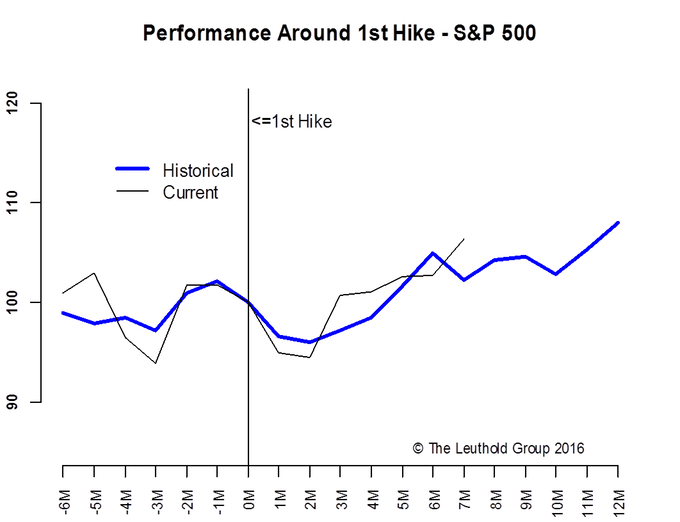

The market’s skepticism about the Fed’s ability to raise rates partly reflects the lack of significant inflationary pressures, which explains why bond yields stay so stubbornly low. It also reflects the Fed’s unwillingness to rock the boat before the presidential election in November. So we find ourselves in the twilight period where the impact of a rate hike might be waning (simply because the last hike and the next potential hike are equally far away), while the potential election-year impact might be gaining more influence. To see which one has been a more important driver so far, we thought it would be helpful to compare market patterns around 1st rate hikes with our time-cycle composites (an average of the annual seasonal pattern, the presidential election cycle and the decennial pattern).

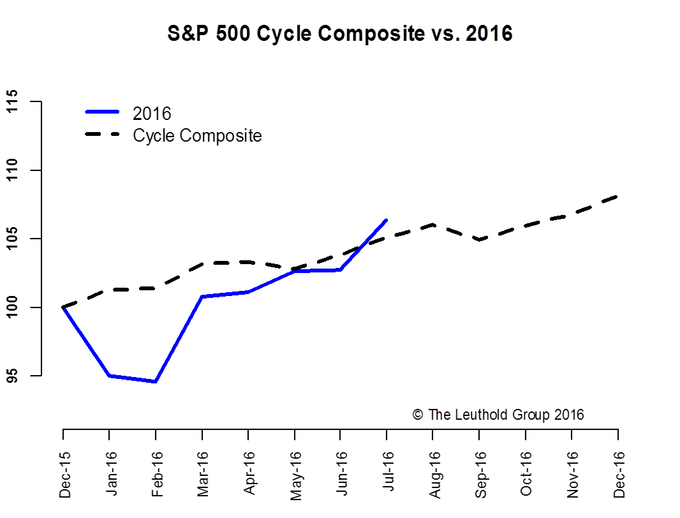

When it comes to the stock market, Fed policy has so far trumped the election-year cycle. Chart 5 shows an uncanny similarity between current S&P 500 performance and the historical pattern around the first rate hike. On the other hand, the S&P 500 index deviated from the time-cycle composite early this year but has since closed the gap. Both patterns for the rest of the year show a bit more volatility in the near term, followed by a year-end rally (Chart 6). Obviously, this implies that the rest of 2016 will conform to the typical pattern, which has not been the case so far this year.

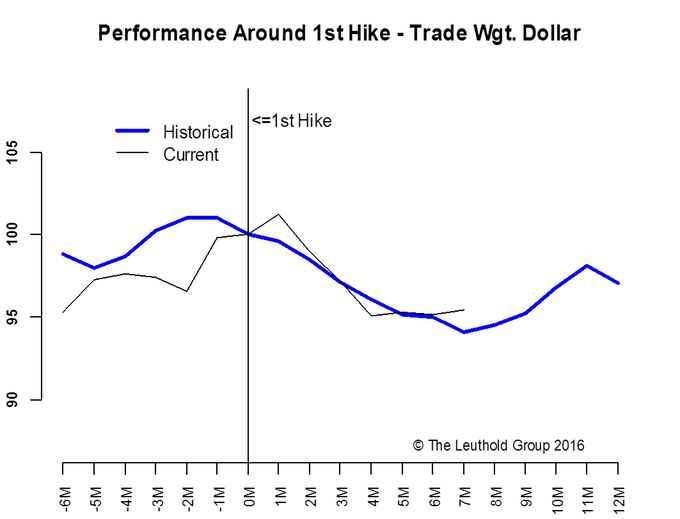

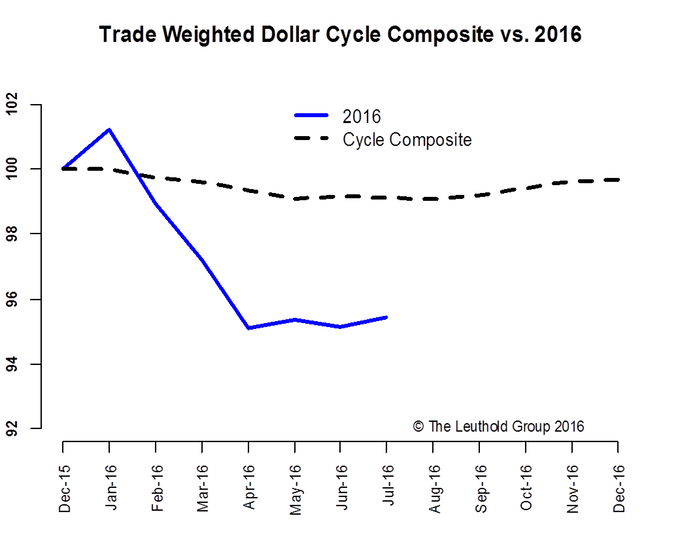

Another market in the crosshairs of Fed policy and election politics is the U.S. dollar. Both central bank policies and politics (especially with Trump’s “America First” rhetoric) have wide-ranging impacts on the dollar but so far central bank policies have mattered much more than election politics. Chart 7 shows that the dollar has been tracking the historical pattern around the first rate hike very well so far, while Chart 8 shows a big difference between the dollar movement this year and its time-cycle pattern. However, both seem to suggest a moderately higher level at year end. Obviously, with scant support from the BoJ and the ECB, and the rate-hike probability at only 35%, a lot has to break right for the dollar to go higher.

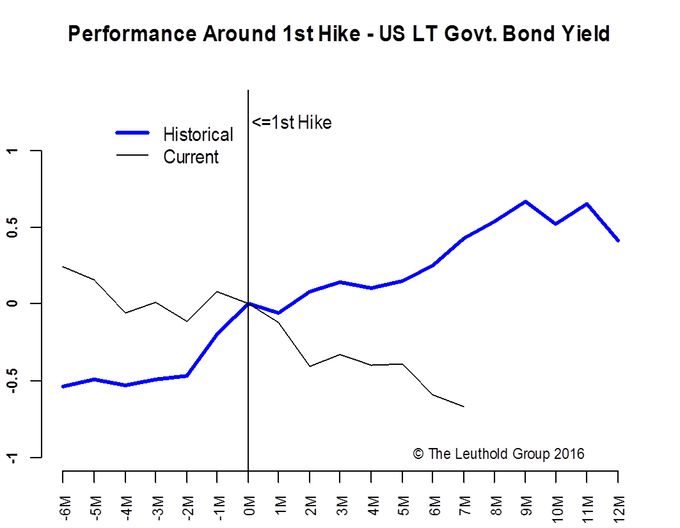

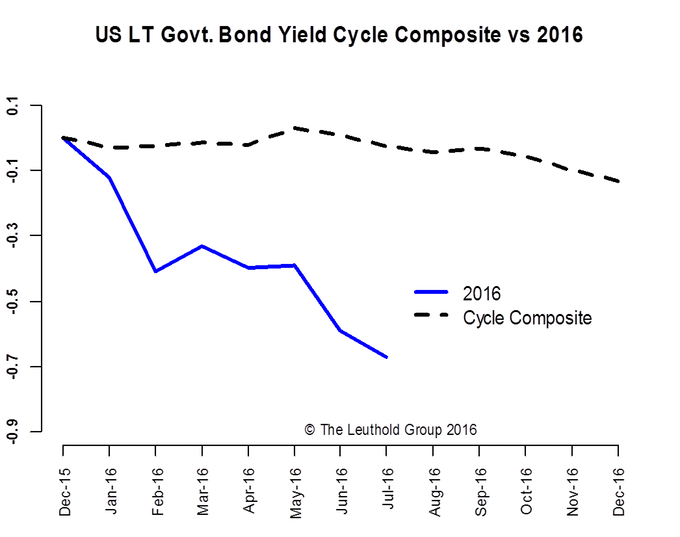

Now, the perennial head-scratcher—a.k.a. the long-term bond yield—lives up to its reputation again. There is no resemblance whatsoever to either pattern (Charts 9 & 10). It’s safe to say global bonds are in an unprecedented regime with one-third of global sovereign debt in negative-yield territory and price-insensitive buyers (central banks) sucking up $180 billion in bonds every month. The supply-demand dynamics completely overwhelmed other fundamental aspects of bond investment and, with the BoE joining the easing party, there seems to be no end in sight at this point.

© Leuthold Weeden Capital Management