It seems as if every day brings another article discussing how much difficulty hedge funds are experiencing — be it poor performance, redemptions or both. Despite the challenges at hedge funds, a number of strategies and funds in the alternatives space overall are performing well so far this year.

Before diving into the performance of alternatives, I’d like to provide a short refresher on how we at Invesco define these investments. Alternatives invest in things other than publicly traded, long-only equities and fixed income securities. We separate the alternatives universe into two baskets: alternative asset classes and alternative investment strategies.

Alternative asset classes defined

Alternative asset classes comprise assets other than stocks and bonds. Investments in real estate (direct investments or real estate investment trusts [REITs]), commodities, infrastructure and master limited partnerships (MLPs) are all examples of alternative asset classes. Given that alternative asset managers primarily take long-only exposure across a specific asset class, these investments frequently have a high market exposure to the underlying asset class. As a result, the performance of the underlying asset class often drives returns.

Alternative investment strategies defined

Alternative investment strategies are investments in which the fund manager is given a high degree of flexibility with how to invest. For example, the manager often has the ability to trade across multiple markets and asset classes, including stocks, bonds, currencies and commodities. The manager is also afforded the ability to short markets (i.e., establish positions that profit from an investment declining in value). Strategies such as global macro, equity long/short, market neutral, managed futures, banks loans and unconstrained fixed income are all examples of alternative strategies.

Alternatives have generated strong returns in 2016

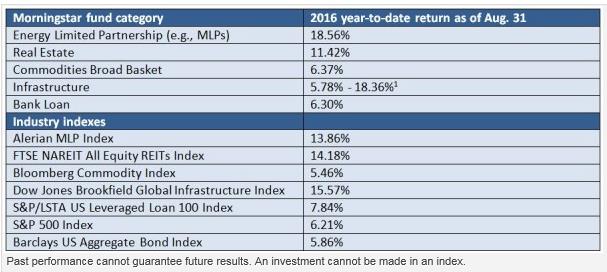

While there are a wide variety of indexes available that seek to measure the performance of alternatives, I’d like to focus on the Morningstar fund category returns, as they are easily viewed and show the performance of widely available mutual funds. A look at the fund category returns below reveals that, through the end of August, a number of alternative categories have generated strong returns in 2016.

As the above table illustrates, several alternative asset classes have been a standout in 2016, providing strong returns well above the S&P 500 Index. And for some asset classes, such as MLPs, commodities and infrastructure, the gains achieved in 2016 follow losses incurred in 2015. Other assets, such as real estate, have remained solid, as the asset class (represented by the FTSE NAREIT All Equity REITs Index) has generated strong returns from Jan. 1, 2009, through Aug. 31, 2016.

Given that funds that invest in alternative asset classes typically have a high exposure to the underlying asset classes, it’s not surprising that funds that invest in alternative asset classes (as defined by the Morningstar categories above) have generated returns that reflect the strong performance of the underlying asset classes thus far in 2016.

Why consider alternatives?

Alternative asset classes have generated equity-like returns with equity-like levels of volatility,2 while offering diversification to traditional equity investments. Additionally, certain alternative asset classes, such as MLPs, infrastructure and certain real estate funds, may provide investors with attractive levels of current income. As a result, investors often use alternative asset classes as a potential source of returns and much-needed yield in the current low yield environment.

For example, bank loans have provided yield this year in addition to competitive returns. In addition to generating a year-to-date return of 6.30%, bank loans currently have a yield of 5.25%.3

Bank loans are pools of senior secured loans made to non-investment grade companies. They are popular because they are fully collateralized, sit at the top of the capital structure and potentially offer attractive yield. The performance of bank loans can tend to track the economic environment: A favorable economic environment makes it more likely loans will be repaid, while a difficult economic environment can cause an increase in default risk.

As a whole, alternative investment strategies are lagging thus far

While alternative assets have been standouts, several alternative strategies are having an uneventful year:

The performance numbers for alternative strategies look lackluster on the surface. However, there are nuances to the category that deserve further examination. For example, manager selection has a strong impact on the returns achieved. Because alternative investment strategies may vary in their return and risk objectives and managers utilize their own unique investment approaches, returns may vary widely across managers. Therefore, simply looking at broad categories, as we do above, is only useful in getting a sense for how the strategy has performed as a whole.

In my view, a better way to gauge the performance of alternative investment strategies is to look at the returns of the individual funds that make up the various Morningstar categories for alternatives. Through this lens, investors will be able to see that some managers have generated returns well above the category average, while others have generated returns well below the average. For this reason, I believe investors need to look beyond the broad categories when evaluating performance and focus on the performance of specific managers.

1 The Morningstar category return was not available. The returns shown represent the range of returns for the funds tracked by Morningstar for its Infrastructure category.

2 From January 1997 through December 2015, the alternative assets category (as defined by a 75% allocation to FTSE NAREIT All Equity REIT Index and a 25% allocation to Bloomberg Commodity Index) had an annualized return of 7.73% with 17.01% standard deviation. That compares with an annualized return of 7.46% and a standard deviation of 15.52% for the S&P 500 Index. The 75%/25% split reflects Invesco’s belief that investors tend to invest in strategies with which they are more familiar.

3 Yield to maturity of S&P/LSTA US Leveraged Loan 100 Index as of Aug. 31, 2016.

Important information

The Alerian MLP Index is a composite of the 50 most prominent energy master limited partnerships calculated by Standard & Poor’s using a float-adjusted market capitalization methodology.

The Barclays US Aggregate Bond Index is an unmanaged index considered representative of the US investment-grade, fixed-rate bond market.

The Bloomberg Commodity Index is a broadly diversified commodity price index.

The Dow Jones Brookfield Global Infrastructure Index measures the stock performance of companies that exhibit strong infrastructure characteristics.

The FTSE NAREIT All Equity REITs Index is an unmanaged index considered representative of US REITs.

The S&P 500® Index is an unmanaged index considered representative of the US stock market.

The S&P/LSTA US Leveraged Loan 100 Index is representative of the performance of the largest facilities in the leveraged loan market.

Yield to maturity is the rate of return anticipated on a bond if it is held until the end of its lifetime.

Hedge funds are typically aggressively managed portfolios of investments for high net worth investors that use advanced investment strategies such as leverage, long, short and derivative positions with the goal of generating high returns (either in an absolute sense or over a specified market benchmark). Hedge fund managers have less restriction on their investment methodologies than mutual fund managers, and hedge funds are less regulated and therefore offer less investor protection than mutual funds. Mutual funds are more transparent with regard to disclosure of underlying holdings and have lower fees than hedge funds.

Alternative products typically hold more nontraditional investments and employ more complex trading strategies, including hedging and leveraging through derivatives, short selling and opportunistic strategies that change with market conditions. Investors considering alternatives should be aware of their unique characteristics and additional risks from the strategies they use. Like all investments, performance will fluctuate. You can lose money.

Fixed income investments are subject to credit risk of the issuer and the effects of changing interest rates. Interest rate risk refers to the risk that bond prices generally fall as interest rates rise and vice versa. An issuer may be unable to meet interest and/or principal payments, thereby causing its instruments to decrease in value and lowering the issuer’s credit rating.

Stock and other equity securities values fluctuate in response to activities specific to the company as well as general market, economic and political conditions.

Most MLPs operate in the energy sector and are subject to the risks generally applicable to companies in that sector, including commodity-pricing risk, supply-and-demand risk, depletion risk and exploration risk. MLPs are also subject the risk that regulatory or legislative changes could eliminate the tax benefits enjoyed by MLPs which could have a negative impact on the after-tax income available for distribution by the MLPs and/or the value of the portfolio’s investments.

Investments in real estate related instruments may be affected by economic, legal, or environmental factors that affect property values, rents or occupancies of real estate. Real estate companies, including REITs or similar structures, tend to be small and mid-cap companies and their shares may be more volatile and less liquid.

Commodities may subject an investor to greater volatility than traditional securities such as stocks and bonds and can fluctuate significantly based on weather, political, tax, and other regulatory and market developments.

Investment in infrastructure-related companies may be subject to high interest costs in connection with capital construction programs, costs associated with environmental and other regulations, the effects of economic slowdown and surplus capacity, the effects of energy conservation policies, governmental regulation and other factors.

Most senior loans (or bank loans) are made to corporations with below-investment grade credit ratings and are subject to significant credit, valuation and liquidity risk. The value of the collateral securing a loan may not be sufficient to cover the amount owed, may be found invalid or may be used to pay other outstanding obligations of the borrower under applicable law. There is also the risk that the collateral may be difficult to liquidate, or that a majority of the collateral may be illiquid.

Short sales may cause an investor to repurchase a security at a higher price, causing a loss. As there is no limit on how much the price of the security can increase, exposure to potential loss is unlimited.

The information provided is for educational purposes only and does not constitute a recommendation of the suitability of any investment strategy for a particular investor. Invesco does not provide tax advice. The tax information contained herein is general and is not exhaustive by nature. Federal and state tax laws are complex and constantly changing. Investors should always consult their own legal or tax professional for information concerning their individual situation. The opinions expressed are those of the authors, are based on current market conditions and are subject to change without notice. These opinions may differ from those of other Invesco investment professionals.

All data provided by Invesco unless otherwise noted.

Invesco Distributors, Inc. is the US distributor for Invesco Ltd.’s retail products and collective trust funds. Invesco Advisers, Inc. and other affiliated investment advisers mentioned provide investment advisory services and do not sell securities. Invesco Unit Investment Trusts are distributed by the sponsor, Invesco Capital Markets, Inc., and broker-dealers including Invesco Distributors, Inc. Each entity is an indirect, wholly owned subsidiary of Invesco Ltd. PowerShares® is a registered trademark of Invesco PowerShares Capital Management LLC, investment adviser. Invesco PowerShares Capital Management LLC (Invesco PowerShares) and Invesco Distributors, Inc., ETF distributor, are indirect, wholly owned subsidiaries of Invesco Ltd.

©2016 Invesco Ltd. All rights reserved.

Alternative assets have impressed in 2016 by Invesco