Part I - The Dollar Ascendant

When I was in elementary school, my family made regular trips to my parents’ birthplace of India. The journey would normally take us from our home in Iowa, to London, to Bombay (now Mumbai), and finally to Hyderabad. Upon arrival, we children would clamor for the local currency, rupees. These rupees were the key to making the summer trip tolerable: rupees purchased quantities of lassi, ice cream, and Indian fruit sodas. During our layover in Bombay, my father allowed us the luxury of room service. After the server made the delivery, he waited for the customary gratuity, and I realized that I had not a rupee on me. I reached into my pocket, but only found a crumpled dollar. I gave it to him with trepidation, but was relieved when he gladly accepted it. At the time, it struck me as odd that the US dollar, a foreign currency, would be accepted by a server thousands of miles away from the US. Now, many years later, that incident serves to remind me of the power and convenience of a reserve currency.1

Introduction

For years, pundits and market participants have stubbornly predicted the demise of the dollar as the premier reserve currency in the world.2 The dollar has defied all skeptics. Even as chatter from market participants has grown louder with every contemporary financial crisis, the demand for dollars has become nearly insatiable.3 First the yen, then the euro, were predicted to become reasonable alternatives to the dollar. Despite these predictions, the demand for dollars has only increased in global financial markets. The Chinese renminbi (RMB), whose roll-out as a new international currency was patiently planned by Beijing’s policymakers, has been listed recently as a long-term viable alternative to the current status quo. So what are the prospects for the RMB, current market turmoil aside? And what is the likely fate of the dollar? GMO’s Asset Allocation team examines these questions in a two-part series. The first part, the rise of the US dollar and the key drivers and conditions that allowed it to attain reserve currency status, is meant to lay the groundwork for reviewing whether a currency is on its way to the status of reserve. Part I also serves as a supplement to work already completed here at GMO by James Montier in his “Market Macro Myths: Debts, Deficits, and Delusions” white paper. Part II, to be published later this year, will examine RMB, as well as several other currencies, to determine their progress toward reserve currency status.

We posit:

■ That the dollar as a preferred currency of exchange, transaction, and store of value is unlikely to be displaced in the near to medium term.

■ For RMB to meet the same type of acceptability as the dollar, an enormous amount needs to be accomplished in the areas of sovereign issuance, bankruptcy law, trade, and collateral usage, as well as the establishment of long-term credibility.

■ We do not mean to say that the dollar’s reserve status will remain unchallenged forever. Indeed, a singular reserve currency, driven by a central bank that is focused on domestic inflation and unemployment, presents a number of challenges to global financial markets and trade. However, to date, the yen and the euro have not proven to be up to the task of competing with the US dollar for reserve currency status.

■ The historically high debt levels of the US are not an impediment to maintaining reserve status, as the country issues its debt in its own currency. Indeed, the scale and liquidity of the Treasury market is a necessary condition to maintaining its reserve currency status.

For all involved in bond and currency markets, the concept of “reserve currency” status is nearly metaphysical and very hard to define. In this white paper, we attempt to define the meaning of reserve currency, briefly look at the modern history of reserve currencies, and then identify the necessary conditions required to be considered a reserve currency. Furthermore, we will discuss implications of the reserve currency status for investors, market participants, and policymakers.

The cross of gold

At the end of the 19th and through most of the 20th century, the concept of a reserve currency lay firmly anchored in that currency’s convertibility into gold. A country’s gold holdings determined its ability to expand the money supply. The dominance of gold, and its limitations, led to the now-famous speech by William Jennings Bryan. He demanded that the ordinary citizenry not be “crucified on a cross of gold” and demanded the US return to “bimetallism,” or the additional use of silver. That decision may have allowed the growth of the monetary base in parallel with economic activity. While it would take another 80 years for the gold standard to be completely cast aside, gold retained its preeminence as the specie of nations.

At the time of Jennings’ speech in 1896, if a currency had any inherent value it was given that value in accordance with the weight of gold each unit of currency brought to the table.4 And for years, the unit of currency that dominated that equation was the British pound sterling. The size of the British Empire, the amount of trade that took place on its sea lanes, the financial sophistication of the City of London as a place to raise capital, and the commitment of Her Majesty’s Exchequer to convertibility helped ensure the pound’s role as the paper currency of preference until 1914.5 While other currencies, such as the French franc and the German mark might have been used for reserves, it is hard to believe that they were a more convenient currency than the pound when used for global trade.6

Today, the dollar is the only serious reserve currency in the world. While there are other useful, or “transactional,” currencies, the dollar remains the universally accepted version of modern-day specie for merchants, financial institutions, and sovereigns.

Just over a century ago, the dollar was a secondary currency relative to the dominance of the pound. While a number of reasons may be given for the pound’s demise versus the dollar’s rise, three key reasons include:

■ The formation of the Federal Reserve in 1913, in order to alleviate the sporadic financial crises that plagued the US financial system, such as the Panic of 1907 following the collapse of the Knickerbocker Trust. The Federal Reserve was meant to add elasticity to the national currency and to serve as a lender of last resort.7

■ The enhanced credibility of the US Treasury, achieved by Secretary William McAdoo during the summer of 1914, by maintaining dollar/gold convertibility upon the outbreak of war in Europe.8

■ The dominance of the US, as the largest creditor nation, at the Bretton Woods conference, where it was able to make dollars and gold virtually substitutable for each other. Great Britain, ably represented by John Maynard Keynes, simply did not have the bargaining power at the conference to preserve the pound’s preeminence.

But why was the dollar not the preferred currency prior to the summer of 1914? The answer is not a mystery. First, prior to the formation of the Federal Reserve, the US was prone to numerous financial crises. In addition, a mere 50 years before the start of WWI, the US had been embroiled in civil war; this was not an encouraging state of events, nor did it inspire confidence in international investors. Second, prior to the summer of 1914, there had been little or no reason to question or doubt the pound’s convertibility into gold. Simply put, the British government had not given the world a reason to seek a new preferred currency.

The formation of the Federal Reserve, and the Treasury’s enhanced credibility during the summer of 1914, made the US dollar a tolerable substitute for the pound. However, it was the third event, the decisions made at Bretton Woods, which finalized the role of the dollar as the world’s reserve fiat currency, turning the de facto relationships of the war into the de jour relationships codified in the international monetary system. The decisions at Bretton Woods codified the dollar as a near substitute for gold, acknowledging the reality that had taken place over the long years of war.

Starting from the 1960s onwards, US monetary liabilities held by foreigners began to exceed US holdings of gold.9 The paradox of being the world’s reserve currency required the US to supply the world with an adequate number of dollars. However, the more dollars it supplied the world, the more the US diminished its credibility regarding its ability to convert those dollars to gold on demand. This paradox is known as the Triffin paradox after Robert Triffin, who identified the problem in the 1960s. From 1965 onwards, in part for political reasons, France demanded its gold and the continuation of this “on-demand” conversion process precipitated in the ending of the gold standard in 1971. Coming off the gold standard, the dollar stayed the reserve currency. However, that did not occur without a substantial devaluation. Indeed, if one reads the minutes of the conference call of the FOMC in 1973, one can sense the palpable alarm among the participants regarding the dollar’s depreciation.10 Nevertheless, the dollar continued to be the world’s reserve currency for lack of any other substantial alternative.

Defining a reserve currency

“I know it when I see it…” uttered Justice Potter Stewart in the famous ruling of Jacobellis v Ohio.11 While that case involved possible conflict between the First Amendment and public decency laws, that particular phrase is illustrative of the ambiguity of the concept of a reserve currency. The line blurs between currencies that are considered “international” and those that are considered “reserve.” A reserve currency needs to be an international currency. An international currency requires that the currency be used in a significant portion of invoicing/trade transactions, and used in the financial markets. In other words, an international currency is really a transaction currency, one that is easily accepted by a number of market and trade participants. A reserve currency goes a level above that and becomes the currency of choice during flight-to-quality scenarios.

There are two necessary, but not sufficient, conditions for a currency to be considered an international or transactional currency, both of which are associated with capital account convertibility.

Condition #1 – A Trading and Invoice Currency. Trade and invoicing must take place in a currency for it to be considered international. Goods and services must be purchased with these currencies. The reason is obvious: Fiat money exists to facilitate some type of exchange between counterparties. A primary invoicing currency determines which currency is used when a good or service is exchanged between two countries.

As noted earlier, during much of the 18th and 19th centuries, the British pound was the world’s reserve currency. The power and expansiveness of the British Empire allowed the pound to be used for trade and invoicing in a convenient manner. The pound was also convertible into gold. A member state of the Empire needed the pound to purchase finished goods and materials produced in England. Raw materials were shipped to England, higher-valued finished products came back, and England financed the difference for her colonies.

The invoicing currency of tradeable goods is an important component of an internationalized currency. Grassman’s Law posits that goods are invoiced in the currency of the exporter. However, today, invoicing is usually determined by whether goods are destined for the US, in which case they are usually invoiced in dollars. This is one way in which the world acquires dollars. Yet why do countries still want dollars? My colleague Phil Pilkington would note that this is almost a “hangover” of Bretton Woods. The concept of hangover refers to the echoes of a codified system that made dollars the most convenient currency to hold in order to manage a nation-state’s liabilities. One can surmise that the countries require dollars for several reasons:

■ As a liquidity reserve or risk insurance (consistent with flight-to-quality or a specie that allows exchange rate management).

■ Mercantilist reasons, meaning that the accumulation of dollars is an output of creating an export-driven economy.

■ The requirement to purchase certain goods that are invoiced only in dollars (such as oil).

Condition #2 – A Liquid and Investable Currency. To invest in a currency, one actually needs a deep and liquid marketplace for securities.12 A short-term, high-quality securities market is critical to the development of an “investable currency.” There are several criteria for a currency to be considered “liquid.”

■ Short-term, high-quality commercial paper and bills market. The importance of this market cannot be overstated for the functioning of a reserve currency. It allows investors to purchase securities that they consider “cash-like” with limited credit risk. For banks, this market creates a liquid place to deposit cash as an alternative to depositing cash in a central bank account (remember, until recently, the commercial banks did not earn a return on their excess central bank deposits). For a central bank, self-liquidating notes offer the ability “to furnish an elastic currency, and to afford means of discounting commercial paper.”13 A high-quality commercial paper market, in conjunction with a functioning market for interbank lending, such as the fed funds market, allowed banks that were flush with reserves to lend to banks that needed more reserves.14

Commercial paper, where a lender has a predictable bankruptcy recovery process, has been a diverse and readily available place to hold cash that is not expected to change in value. A.O. Greef ’s magnum opus, The Commercial Paper House in the United States, provides an extraordinarily comprehensive overview of short-duration activities in US financial markets. Indeed, the development of an open market in commercial paper allowed bank reserves to move from parts of the country that were flush with reserves to parts of the country where reserves were scarce.15 Here the Federal Reserve served as a monetization agent, turning some of these short-term papers, such as bankers acceptance notes, into a liquid form of tender. This ability to convert high-quality paper into cash is a key part of a stable fractional reserve banking system.

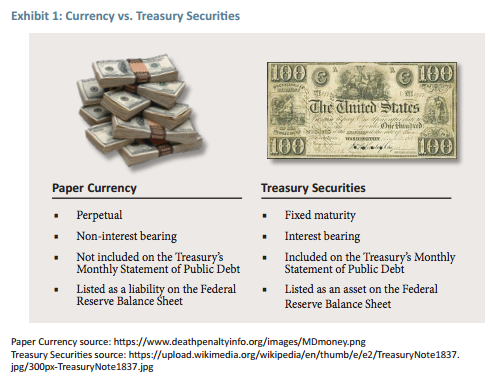

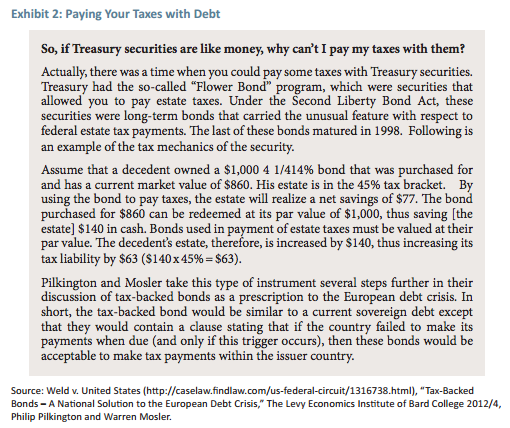

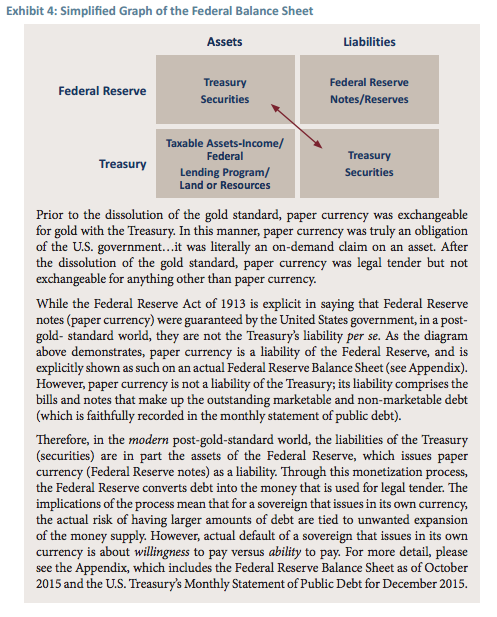

Both the commercial paper market and interbank lending markets had, of course, some credit risk to the issuer or borrower and may have increased wholesale funding risks.16 Treasury bills, on the other hand, serve as de facto cash: Bills, like cash, are a liability of the Federal government (please see Exhibit 1). Bills have little or no counterparty risk. Bills can be posted as collateral, they have little duration, and the securities are easily attainable and/or have a broadly predictable supply. For all intents and purposes, bills are considered money. Indeed, paper money, the very pieces of paper you have in your wallet, can be considered non-interest bearing perpetual debt (or debt with no maturity), while longer-dated Treasury coupon securities are discounted, interest bearing money (please see Exhibit 2). The Federal Reserve serves as the monetization entity that converts debt with a finite maturity (such as Treasury coupon and bill securities) into debt with perpetual maturity (paper currency or legal tender). The sale and purchase of Treasury securities was another method used by the Federal Reserve. Later, due to necessity, repo operations were added to the institutions toolkit.17 This brings about the interesting question that if Treasury securities (particularly bills) are like money, why can’t we pay our taxes with them? In fact, as Exhibit 2 shows, there was once a Treasury issuance that allowed such an arrangement.

■ A liquid and developed government yield curve. A well-built-out, risk-free curve will serve as a benchmark for liquid borrowing by private issuers. Some participants would argue that a liquid swaps curve would suffice, and they would point to the phenomena of negative swap spreads as an indication that swaps are now the preferred benchmarking vehicle due to their lower balance sheet costs relative to government cash securities. That perhaps may be true, but we argue that the development, and maintenance, of a swap curve is in part dependent on the price discovery provided by government securities.

■ An effective and tested bankruptcy code. The concept of “predictable outcomes” is required for a private credit market that is not backstopped by government guarantee. Private credit markets are more likely to flourish when there are more predictable outcomes in bankruptcy.

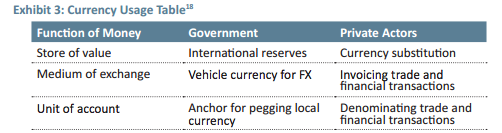

The functions of each actor represented in Exhibit 3 show the uses of an international currency.

Do credit ratings matter?

On the evening of Friday, August 5, 2011, I exited the Treasury Department, heading down the steps of the “Hamilton Entrance” accompanied by loud music from the rooftop party at the W Hotel across the street. The bass beat added a surreal background to the fact that Standard and Poor’s had just informed the Treasury that the AAA rating of the US was going to be downgraded, despite the best efforts of the Treasury. That weekend, Treasury staff and senior officials braced themselves for the possibility of an unforeseen risk in Treasury’s borrowing markets. Instead, on Monday, Treasury securities rallied hard as “risk” assets such as equities plummeted.

Often, observers of currency markets will make the claim that the highest credit quality, or credit rated, currencies will naturally evolve to become reserve currencies. So, do ratings really matter for the usage of an international currency? Empirically, ratings appear to matter very little, but the answer is more nuanced. It appears to matter very little as long as the country in question can issue debt in its own sovereign currency and has a relatively freely floating exchange rate. During the US debt ceiling debacle of 2011, the downgrade of the US by Standard and Poor’s sharply increased demand for US Treasury securities.19 During the debt ceiling crisis of 2013, investors differentiated between government securities that matured or paid coupons on the announced “drop dead” date and those that did not.

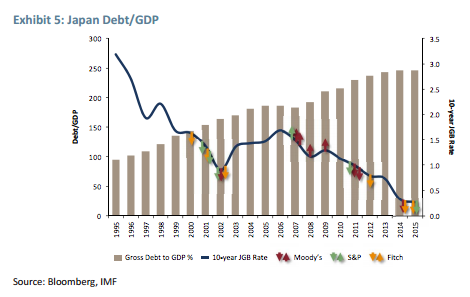

Japan provides another case in point. Rating agencies have steadily downgraded the ratings applied to the government of Japan. The world has waited for Japanese interest rates to rise, but they have simply moved lower. If there is one currency that competes with the US dollar for “flight to quality” type of safety features, it is the Japanese yen, which rallies during most “risk-off” episodes.

If government liabilities grow beyond a traditional debt management strategy, such countries can monetize their liabilities through their fiat currency. This is exactly what has happened at the Bank of Japan with its purchase program of JGBs. Despite Japan’s high debt levels, the concern now is that there are not enough JGBs available for the Bank of Japan to purchase. While this may have secondary market implications, this is not the classic definition of a default. Indeed, technically the Bank of Japan could simply cancel the debt assets it has purchased from the market. By doing so, it would have negative equity or a deferred asset.20 Some market participants have suggested that Japan undertake that step, and ease any concerns about the fiscal health of the government. This does not mean such a step is not without unintended consequences or possible political implications.21

To a central bank, a piece of its currency is a liability, while its assets are traditionally the debt of its issuer nation.22 For a sovereign government’s financing authority, its liabilities are the debt securities of its issuer government.23 I discuss this de facto relationship in Exhibit 4. Additionally, one can review the actual Federal Reserve balance sheet in the Appendix and note the red arrows. The important implication of this matter is that as long as that asset/liability relationship exists between the issuing financing authority and its central bank, then default is a political decision, not a financial decision. Other commentators state that the excess creation of money, through the debt monetization process, will lead to inflation. The prior scenario is only likely to occur when aggregate demand exceeds aggregate supply within an economy in some form.24 If demand is not doing so in some fashion, then you can again look to Japan where, despite massive Bank of Japan purchases of government securities, inflation is still extraordinarily low.

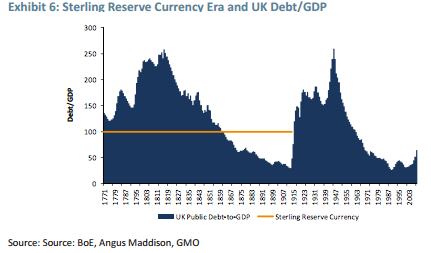

Exhibit 5 clearly shows the relationship (or lack thereof) between the JGB market and the Government of Japan’s credit rating. Exhibit 6 shows the relationship of sterling during its reserve currency period prior to World War I to overall UK government debt. The data presented is also relevant to our earlier point on page 8 regarding the necessity of a liquid and developed government yield curve.

How do we measure the demand for dollars?

There are three critical questions to answer in order to assess the current demand for dollars:

■ How useful is the currency in reserve financial infrastructure transactions (such as collateral for clearing houses)?

■ How much of that currency is held by reserve bank managers?

■ What happens to its relative demand during normal and extraordinary periods of capital market activity?

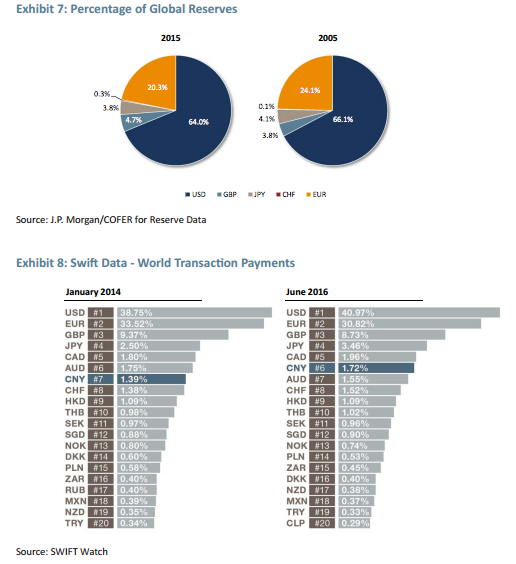

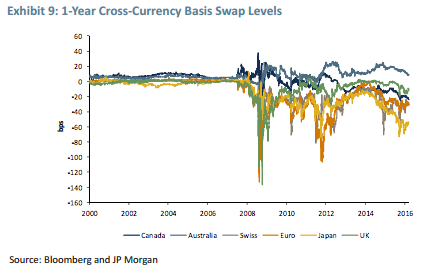

The first two questions can be partially answered by looking at the transaction data from SWIFT, as well as the IMF COFER data on reserve manager asset holdings. The first answers the question regarding the composition of reserve currency management assets (see Exhibit 7). The second is a proxy to show the usage of various currencies using bank wire transfer data (see Exhibit 8). Both data sets tell us the dollar remains king.

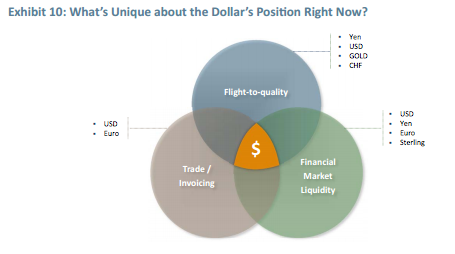

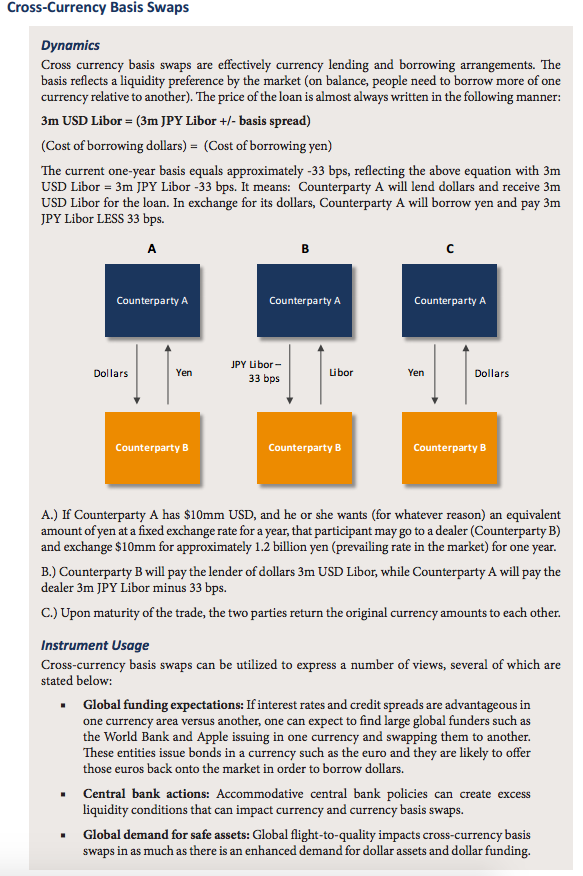

One market-based measure of the “shadow demand for dollars” is the cross-currency basis swap market.25 Cross-currency basis swaps are funding agreements, where two counterparties exchange notional amounts of currency for a pre-agreed amount of time and pay each other floating rates coupons (a detailed explanation of the instrument is included on the last page of the Appendix). It allows a market participant to access funding in a currency that he or she may not be able to access in the normal course of operations.

Exhibit 9 shows the cross-currency basis between US dollars and other large, major transactional currencies. The more negative the basis is, the stronger the bid for dollars. The chart shows, since the financial crisis, ongoing excess demand for US dollars. It also shows that the US dollar possesses a strong safe-haven quality. When fear increases in financial markets, demand for the US dollar also increases.

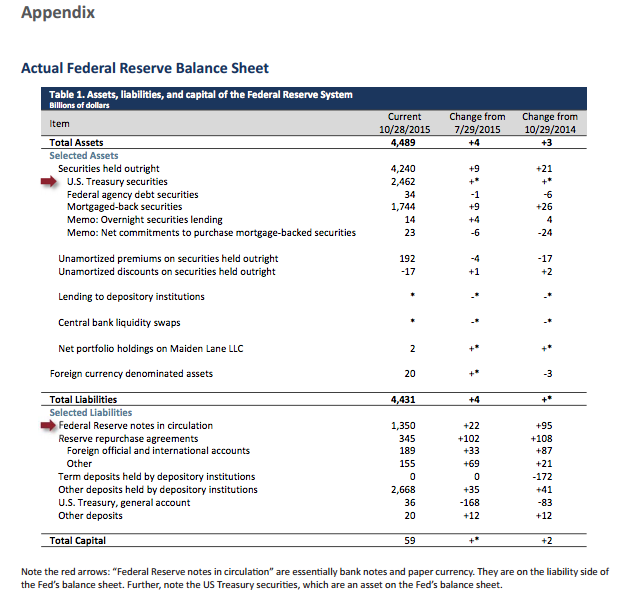

Despite excess demand for US dollars, US policymakers should not be complacent. The ability to have the preeminent reserve currency, without it being locked to a finite good such as gold, gives the US enormous advantages. For all intents and purposes, US dollars (and Treasuries) are gold (see Exhibit 10). As my colleague James Montier has suggested, the US is like Rumpelstiltskin spinning out gold at will. The current account deficits that the US runs most years mean that the world is willing to give the US goods and services for the privilege of owning pieces of paper (indeed as a friend noted, they are not even pieces of paper, they are electronic credits). As such, the US has an important opportunity to invest in long-term, prosperity-enhancing projects. In this light, the US should never endanger those opportunities by inflicting wounds upon itself, as was the case during the recent debt ceiling debacles.

However, others argue that the preponderance of the dollar is a core point of global financial instability. The IMF has suggested that a more multilateral currency framework, or enhanced use of SDRs (special drawing rights), would be beneficial to global financial stability, including utilizing the Fund to act as a lender of last resort to those requiring flight-to-quality liquidity.26 In short, if the dollar is the reserve currency of the world, how does the Federal Reserve set appropriate monetary policy for the US? It’s a question that is under debate during this current phase of Federal Reserve monetary policy tightening.

While there are a number of concerns regarding the world’s dependence on dollars, as noted in the IMF paper, US policymakers should remain cautious toward divergence away from the dollar. While currency regime changes appear to be generational, to date it has been hard to find an example where a change in the reserve currency status was not a zero sum game for the country that held that status.

Part II of this paper will address the growth and utility of RMB usage, the failure of other developed market currencies such as the yen and the euro to fully achieve dominant reserve currency status, and the odd development of alternative currencies such as bitcoin.

Amar Reganti is a member of GMO’s Asset Allocation team. Prior to joining GMO in 2015, he was the Deputy Director of the Office of Debt Management for the U.S. Department of the Treasury. Previously, he was a director and portfolio manager for investment grade credit at UBS Global Asset Management. Mr. Reganti earned his BA in Economics from Vassar College, his MS in European Political Economy from the London School of Economics, and his MBA from the University of Chicago Graduate School of Business.

Disclaimer: The views expressed are the views of Amar Reganti through the period ending September 2016, and are subject to change at any time based on market and other conditions. This is not an offer or solicitation for the purchase or sale of any security and should not be construed as such. References to specific securities and issuers are for illustrative purposes only and are not intended to be, and should not be interpreted as, recommendations to purchase or sell such securities.

Copyright © 2016 by GMO LLC. All rights reserved.

1 Others have used similar nostalgic cultural references to the dominance of the dollar. Barry Eichengreen, in his book Exorbitant Privilege: The Rise and Fall of the Dollar and the Future of the International Monetary System, does so in a far more urbane manner, citing the 1940s film The Counterfeiters. In fact, Mr. Eichengreen had a “taxi driver in New Delhi” experience that is similar to my childhood experience with room service in 1980s India.

2 In a tongue-in-cheek manner, we can refer to even some non-market participants: The Jay-Z video “Blue Magic” in 2007 was considered controversial because it featured a suitcase full of euros, a rebuke to the perceived weakness of the dollar.

3 Benjamin Cohen also has an excellent essay in Revue de la regulation on “The Demise of the Dollar,” which provides a great summary of the dollar’s enduring power.

4 But why gold? The assumption is that individuals considered the barter system awkward and, therefore, transferred a store of value into something that all parties agreed was valuable: precious metals. However, the economist Randall Wray in Understanding Modern Money argues that this is a naïve interpretation of the usage of gold. He states that the acceptance of any good/metal/piece of paper as a “currency” was due to the demands of taxation: If a king or government required you pay your taxes in gold…you needed to acquire gold through labor or trade or investment. This has an important implication for a reserve currency: You need it because there are certain liabilities that can be paid only in that currency.

5 http://www.telegraph.co.uk/news/1399693/A-history-of-sterling.html

6 Eichengreen (Tawney Lecture series) mentions these two currencies’ reserve growth prior to WWI as evidence of lesser use of the pound. However, one wonders if that might have had more to do with repeated geopolitical tensions rather than its use in international trade.

7 Kenneth D. Garbade, Birth of a Market, MIT Press, 2012, p. 24.

8 For an incredible account of the currency and monetary affairs during the summer of 1914, I highly recommend William Silber’s When Washington Shut Down Wall Street, Princeton University Press, 2007.

9 https://www.ecb.europa.eu/press/key/date/2011/html/sp111003.en.html

10 http://www.federalreserve.gov/monetarypolicy/files/fomcmod19730307.pdf

11 Jacobellis v. Ohio, 378 U.S. 184 (1964).

12 Jeffrey Frankel, “Internationalization of the RMB and Historical Precedents,” Journal of Economic Integration, 2012.

13 Garbade, Ibid., quotation from preamble of Federal Reserve Act of 1913.

14 What is the fed funds market? In its simplest form, it is the market wherein commercial banks lend each other unsecured funds for reserve purposes. The rate at which the lending takes place is the fed funds rate. For an excellent history of the market, review the Richmond Fed’s piece: https://www.richmondfed.org/~/media/.

15 E.E. Agger, “The Development of an Open Market for Commercial Paper,” The Annals of the American Academy of Political and Social Science Vol. 99, The Federal Reserve System-Its Purpose and Work (January 1922), pp. 209-217.

16 A risk that almost became unmanageable during the Global Financial Crisis.

17 Kenneth D. Garbade, “Repurchase Agreements as an Instrument of Monetary Policy at the Time of the Accord,” Federal Reserve Bank of New York Staff Reports, June 2016.

18 Frankel, Ibid.

19 The downgrade had other financial market consequences as well. Capital markets experienced carnage during the course of the week following S&P’s downgrade. The S&P 500 index declined and credit spreads widened. The downgrade punished investors in private sector markets at a time when economic conditions remained fragile. Such self-inflicted wounds could theoretically undermine the confidence in a currency’s reserve status.

20 For a more thorough and concise discussion of the Federal Reserve’s balance sheet, see Carpenter, Ihrig, Klee, Quinn and Boote’s “Federal Reserve’s Balance Sheet and Earnings: A Primer and Projections,” March 2015.

21 Indeed, Japan has a troubled political history in that regard, as can be learned by reading Richard Smethurst’s biography of Takahashi Korekiyo, Japan’s Finance Minister prior to World War II. This was a book recommended by James Aitken and I am finding it thoroughly enjoyable.

22 Carpenter, et al.

23 Which are dutifully reported on the Monthly Statement of Public Debt.

24 For a more thorough discussion of the matter, I strongly recommend James Montier’s piece “Market Macro Myths: Debts, Deficits, and Delusions,” available at www.gmo.com.

25 While there are a number of pieces on cross-currency basis swaps available, the two I found the most useful are the Barclays’ Marvin Barth piece the “Cross-currency basis: The shadow price of USD dominance,” and, as always, for anything financial market plumbing related, James Aitken’s insightful “Notes from a Small Island” June 16, 2016. Please see the Appendix for a more complete description of cross-currency basis swaps.

26 http://www.imf.org/external/np/pp/eng/2010/041310.pdf