In recent months, questions about equity market valuations have flooded my desk. The rising price-to-earnings (P/E) ratio for the S&P 500 Index and the run-up in equity prices seem to have shaken investor confidence in future returns. With this in mind, it is worth considering equity valuations from a historical perspective.

A historical look at equity valuations shows wide variation

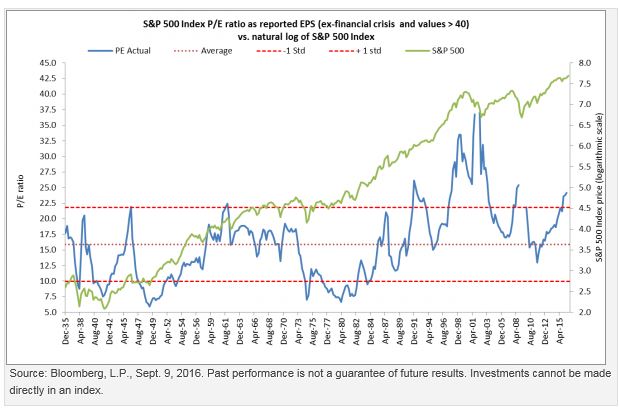

A look back in time suggests that P/E ratios have varied widely over the past 80 years. This can be seen in the graphic below, which displays the trailing P/E ratio for the S&P 500 Index between December 1935 and June 2016, overlaid with the logged value of the S&P 500 Index across the same period. (The S&P 500 Index uses a logarithmic scale so that price movements over time can be seen more clearly, while the 1990s tech bubble and 2008 financial crisis are excluded as outlier events.)

This graphic illustrates a few key points:

- Since 1935, the P/E ratio for the S&P 500 Index has averaged 15.9, with a standard deviation of 5.9. At writing, 97.8% of S&P 500 companies had reported earnings for the June 2016 quarter. The mean P/E ratio was 24.2 and elevated relative to history.1

- There appears to be some tendency for P/E ratios to revert to mean, but this reversion has been less clear since the early 1980s, and the S&P 500 Index has not seen its P/E ratio drop below 10 since around 1982.3 There are a number of potential explanations for this, including behavioral changes, advancing technology and a declining interest rate environment.

- P/E ratios tend to rise and fall with the market. Put another way, bull markets tend to see rising and high P/E ratios and bear markets tend to see falling and low P/E ratios.

The effect of low interest rates on stock valuations

Beyond the cyclical nature of valuations, considering P/E ratios through the lens of Treasury yields offers another perspective.

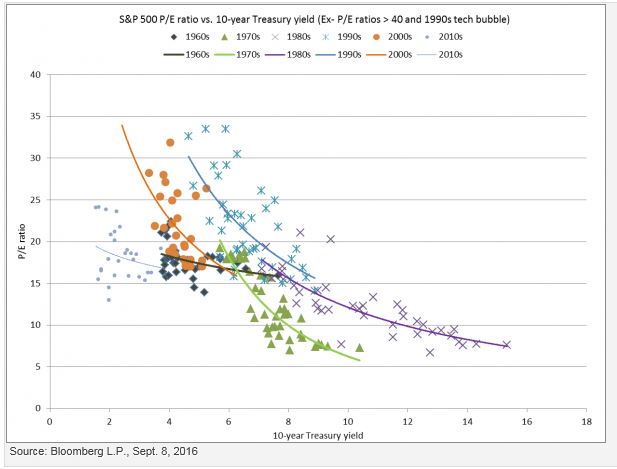

Historically, there has been an inverse relationship between the 10-year Treasury yield and the S&P 500’s P/E ratio. This relationship is not altogether surprising, since the value of a stock is based in part on the discounted value of earnings. As a result, interest (discount) rates tend to affect valuations. Based on simple discounting math, an investor would pay more for $1 of earnings when interest rates are 2.5% than when interest rates are 10%. The lower the rate, the higher the present value.

The graphic below examines this relationship in more detail, plotting P/E ratios against 10-year Treasury yields by decade, from 1960 to the present.

What can we learn from this graphic?

- Clearly, lower yields have tended to lift P/E ratios, although the relationship has varied by decade. During the 1970s and 1980s, the relationship was clear. In fact, the 10-year Treasury yield explained 73% of the variation in P/E ratios during the 1970s, and explained 70% of the variation during the 1980s.2 By contrast, the 10-year Treasury yield explained only 16% of the variation in P/E ratios during the 1960s.2 More recently, quantitative easing has distorted the relationship.

- Given today’s historically low yields, P/E ratios are not abnormally high, in my view. Based on past history, a case could even be made that P/E ratios could be higher. While past performance can’t guarantee future results, today’s mean P/E ratio of roughly 24 would have been consistent with a much higher interest rate in the 1990s, or even in the 1970s. Just look at where a 3% Treasury yield would intersect the blue line that defines the 1990s!

Stocks may seem expensive at the moment, but valuations seem less troubling when taking into account interest rates. Clearly, low interest rates have tended to buoy valuations. But there are also other forces at work. The sharp drop in energy and commodity prices in 2015 weighed on corporate profits. In my view, the stock market may be rationalizing this as a transient event, while expecting more normalized profits in the future. Put another way, the market may be expecting earnings to catch up to stock prices.

The value factor may be a good way to navigate current valuations

Investors concerned that rising interest rates may compress future valuations may wish to consider the value factor. By definition, value stocks tend to be inexpensively priced. Value is typically determined by financial statement analysis through metrics like price-to-earnings, price-to-sales or price-to-book ratios. While the potential benefits of the value factor are best evaluated over full market cycles, value-oriented shares can be influenced by market and economic conditions over shorter periods. Value has historically performed well in rising rate environments, which can be consistent with periods of strong economic growth. As a result, value stocks may offer lower P/E ratios than the general market and may benefit if interest rates rise. For example, the S&P 500 Enhanced Value Index now offers a P/E ratio of 11.6 — well below today’s average P/E ratios.3

PowerShares offers three value ETFs: The PowerShares Dynamic Large Cap Value Portfolio (PWV), PowerShares S&P 500 Value Portfolio (SPVU) and the PowerShares Russell Top 200 Pure Value Portfolio (PXLV).

1 Source: Standard & Poor’s, Sept. 8, 2016

2 Sources: Standard & Poor’s and the Federal Reserve Bank, Sept. 8, 2016

3 Source: Bloomberg L.P., Sept. 8, 2016

Important information

The S&P 500 Enhanced Value Index is designed to measure the performance of the top 100 stocks in the S&P 500 Index with attractive valuations based on “value scores” calculated using three fundamental measures: book value-to-price, earnings-to-price, and sales-to-price.

The S&P 500 Index is an unmanaged index considered representative of the US stock market.

A logarithmic scale is a nonlinear scale used when there is a large range of quantities. Each step on the scale is a multiple of the preceding step.

Price-to-book ratio is the market price of a stock divided by the book value per share.

Price-to-earnings ratio, also called multiple, measures a stock’s valuation by dividing its share price by its earnings per share.

Price-to-sales ratio is a valuation metric calculated by dividing a company’s market capitalization by its total sales over a 12-month period.

Standard deviation measures a portfolio’s range of total returns and identifies the spread of a portfolio’s short-term fluctuations.

A mean is the arithmetic average of a set of numbers or distribution.

Valuation is how the market measures the worth of a company or investment.

Typically, security classifications used in calculating allocation tables are as of the last trading day of the previous month.

There are risks involved with investing in ETFs, including possible loss of money. Shares are not actively managed and are subject to risks similar to those of stocks, including those regarding short selling and margin maintenance requirements. Ordinary brokerage commissions apply. The fund’s return may not match the return of the underlying index. The fund is subject to certain other risks. Please see the current prospectus for more information regarding the risk associated with an investment in the fund.

A value style of investing is subject to the risk that the valuations never improve or that the returns will trail other styles of investing or the overall stock markets.

Investments focused in a particular industry or sector are subject to greater risk, and are more greatly impacted by market volatility, than more diversified investments.

Investing in securities of large-cap companies may involve less risk than is customarily associated with investing in stocks of smaller companies.

The fund may engage in frequent trading of its portfolio securities in connection with the rebalancing or adjustment of the underlying index.

The fund is non-diversified and may experience greater volatility than a more diversified investment.

The information provided is for educational purposes only and does not constitute a recommendation of the suitability of any investment strategy for a particular investor. Invesco does not provide tax advice. The tax information contained herein is general and is not exhaustive by nature. Federal and state tax laws are complex and constantly changing. Investors should always consult their own legal or tax professional for information concerning their individual situation. The opinions expressed are those of the authors, are based on current market conditions and are subject to change without notice. These opinions may differ from those of other Invesco investment professionals.

All data provided by Invesco unless otherwise noted.

Invesco Distributors, Inc. is the US distributor for Invesco Ltd.’s retail products and collective trust funds. Invesco Advisers, Inc. and other affiliated investment advisers mentioned provide investment advisory services and do not sell securities. Invesco Unit Investment Trusts are distributed by the sponsor, Invesco Capital Markets, Inc., and broker-dealers including Invesco Distributors, Inc. Each entity is an indirect, wholly owned subsidiary of Invesco Ltd. PowerShares® is a registered trademark of Invesco PowerShares Capital Management LLC, investment adviser. Invesco PowerShares Capital Management LLC (Invesco PowerShares) and Invesco Distributors, Inc., ETF distributor, are indirect, wholly owned subsidiaries of Invesco Ltd.

©2016 Invesco Ltd. All rights reserved.

Stock valuations are elevated, but are current prices unprecedented? by Invesco