Talking Points:

- Despite recent strength, emerging markets (EM) appear to have room to run.

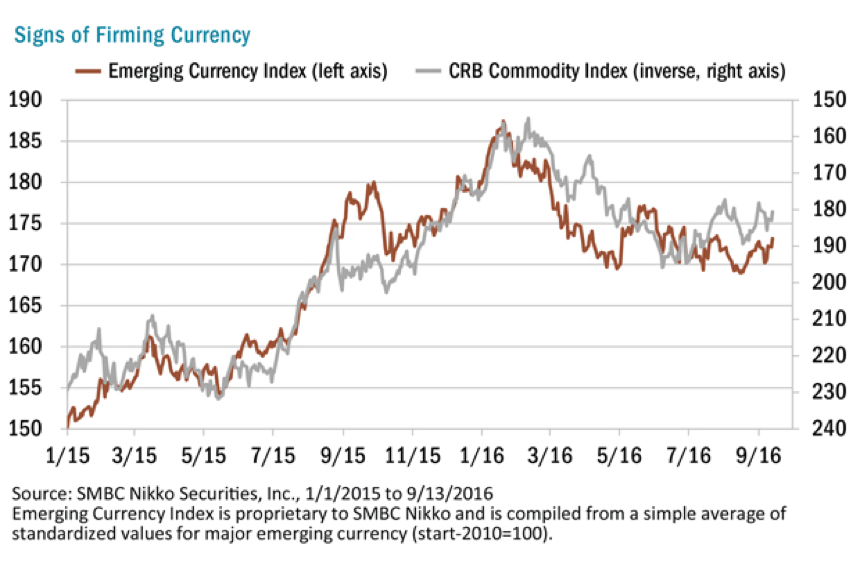

- Stable currencies should boost growth.

- EM economies are diverse and no longer driven by commodities.

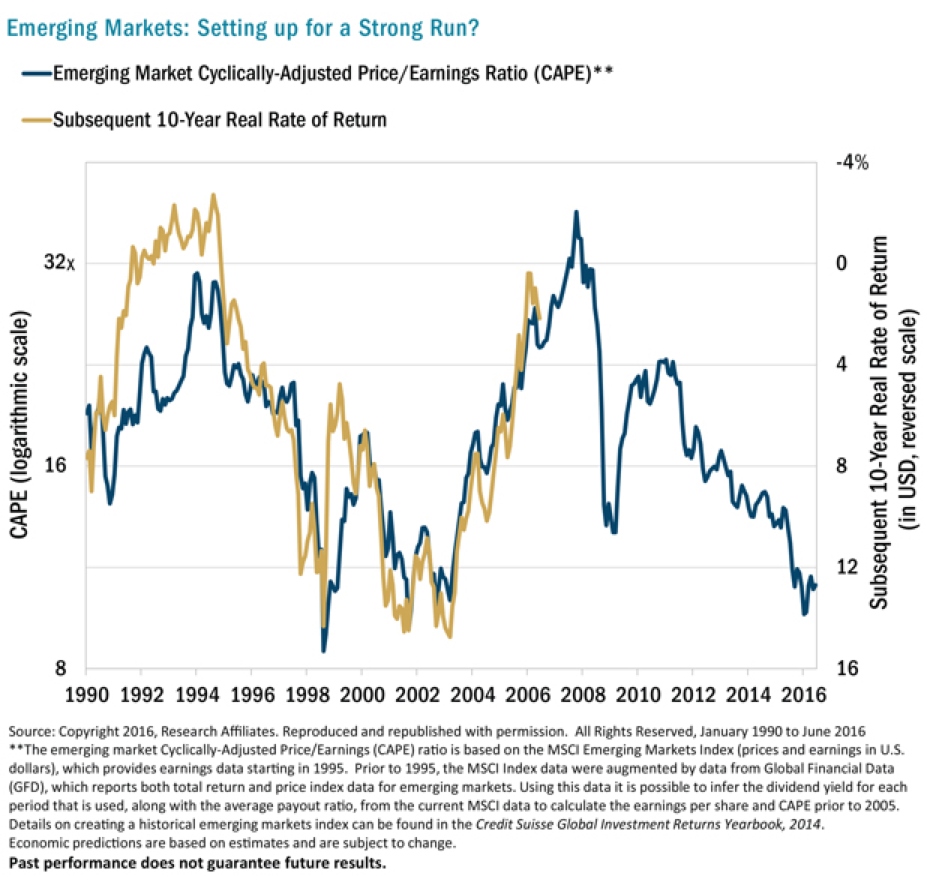

- In our opinion, valuations continue to create opportunities in the near– and long–term.

Enduring Markets

Potential rate hikes in the U.S., tepid growth of developed economies, and a fragile energy market have led to doubts about the staying power of this year’s surge by EM equities. We believe this view overlooks stabilizing local currencies, differentiation among national economies, the long–term potential of developing regions, and continued attractive valuations.

A look at the recent past may explain why some are hesitant to embrace the recent strong returns among EM names.

Much of 2015’s poor performance was tied to weakening local currencies. Among the hardest hit were energy producing countries that faced a one–two punch of lower crude prices and higher debt servicing costs. Brazil highlights the challenge. During 2015, the Real was off more than 45% versus the U.S. dollar. At the same time, oil, the country’s third largest export, remained well below historic averages. The combination was painful for investors with the major Brazilian market down 13.3% in local terms and nearly 42% on a dollar–denominated basis. The country appears to have turned a corner and the free fall has abated even as crude prices remain volatile.

Brazil’s steady currency has been a boon for investors. The Real has firmed and many investors also sense that its Finance Minister has room to step in to quell inflation. The benign situation has led to greater interest in the region and the Bovespa—Brazil’s primary stock exchange—is up 37% in local denomination and 67% in U.S. dollar returns through the first eight months of the year. We believe other emerging countries will continue to benefit from a similar dynamic.

Stabilization is a growing theme in developing markets and has shown signs of resiliency. As the chart shows, EM currencies weakened significantly in 2015 on fears of U.S. rate tightening. However, when expectations of higher rates ticked up in spring, the reaction was muted. Stronger local currencies can keep inflation in check and provide more flexibility for policy makers to spur growth domestically.

Beyond the BRICs

Skeptics of current EM strength note that mature markets are laboring under a low– or no–growth environment. As a result, commodity demand could remain sluggish and upside potential for exporters may be limited. We acknowledge growth in developed markets is tepid, yet believe the strength of local consumers in budding regions is being overlooked.

Exporters Brazil, Russia, India, and China (BRIC) remain dominant among emerging economies, but opportunities are widespread and less driven by commodity producers. For example, Stock Spirits Group PLC (STCK LN), a leading branded spirits player in Eastern and Central Europe, is a top 10 holding in our portfolio and has been a significant contributor as it has been able to maintain margins in a highly competitive space. The company is indicative of our EM exposure, which is diversified among sectors and lacks direct Energy exposure.

As currency erosion subsides, the chart illustrates how consumers from Thailand to Indonesia are showing early signs of opening their wallets. While the uptick in spending may not make a meaningful impact to economic data, the increased sales can be significant at the company level and should benefit active stock pickers.

A Long–Term Case

Recent strength aside, we have long been constructive on emerging markets due to a combination of population growth and improved standards of living. In developing economies, the middle class is growing rapidly.

More young adults are moving to cities, entering the industrial work force, earning higher wages—and enjoying access to an array of consumer goods and services. The world’s middle class population numbered 1.8 billion in 2009.* By 2030, it’s estimated to rise to almost 4.9 billion—a 160% increase in just 21 years.* As this development progresses, the number of middle class consumers will expand dramatically, increasing their share of total global spending.