Key Points

▪ Global monetary policy remains equity friendly, but policy is no longer sufficient to drive equity returns.

▪ We believe the global economy and corporate earnings should improve modestly, if unevenly.

▪ Equities should grind higher over the coming year, but selectivity is growing in importance.

The Monetary Policy Tailwind May Be Fading

During the height of the financial crisis, the Federal Reserve and other central banks stepped in to stave off complete global financial catastrophe. In the ensuing recovery, monetary policy has remained extremely accommodative and been largely responsible for an equity bull market that is nearly eight years old.

For now, monetary policy continues to be a driving force behind equity market performance. Policy alone, however, cannot produce a self-sustaining economic expansion or restore financial imbalances. Something needs to change.

Policymakers may have exhausted their playbooks by this time and are running out of ways to stimulate growth and provide financial stability, meaning the end of the easing era may soon be upon us. We do not expect imminent near-term shifts in global policy, and policy isn’t going to become equity unfriendly any time soon, but further significant gains in equity prices will require something else.

Economic and Earnings Growth Remain Critical

That something else is likely to be accelerated global economic growth and a corresponding earnings recovery.

Over the next year, we expect a gradual and broadly improving global growth trajectory, led by U.S. consumers and a revival in U.S. imports. The jobs market remains on track and incomes are rising, which should boost consumer spending. Summer retail sales were lackluster, but we expect better results ahead. Likewise, manufacturing data will likely improve. Outside of the United States, growth remains relatively weak. A revival in global trade would go a long way toward lifting global growth expectations.

At the same time, we anticipate that corporate earnings results should improve modestly. Given relatively soft growth and the oil/dollar headwind, corporate earnings struggled through most of 2015 and early 2016. We are starting to see a turnaround, however. After a long recession in earnings, S&P 500 earnings-pershare growth was up 1% in the second quarter, excluding energy.1 That’s a good sign and augers well for results in the coming quarters.

Looking ahead, we expect overall EPS growth to turn positive late this year or early in 2017 as the energy drag wanes. The still-sluggish economic environment, however, means that earnings will likely continue to struggle and remain uneven.

Equity Prices Should Grind Unevenly Higher

We remain mildly risk-on in our investment positioning, and expect equities and other risk assets to move higher over the next 12 months. A December Fed rate hike could spark some volatility, but shouldn’t derail the bull market as the Fed plans to proceed cautiously.

Central bank policy outside of the United States also bears watching. The Fed is the lone major central bank that is starting to shift to a tighter stance. Other global central banks remain firmly in easing mode, which should act as a partial anchor on Treasury yields. We think yields will likely rise as economic growth improves and as policy slowly starts to shift, but any advance should be gradual and not enough to act as a headwind for risk assets.

We understand investors’ desire to be cautious, given uneven economic growth and a host of geopolitical issues. We also acknowledge that equity prices are not as cheap as in recent years, making some investors reluctant to enter the markets. At the same time, we think equities look more attractive than bonds (particularly government bonds offering yields near historic lows) and cash, which is still offering close to 0% returns.

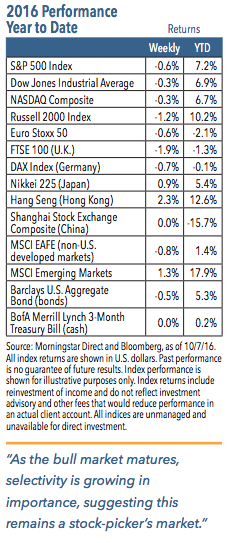

As the bull market matures, selectivity is growing in importance, suggesting this remains a stock-picker’s market and one that we believe will favor active management. In our view, there are a number of different elements investors should consider when building equity portfolios. First, they should focus on the sustainability (and, perhaps more important, growth potential) of dividends. We expect more dividend increases in the future, if and when earnings become more stable. More broadly, we also favor domestically sourced earnings, cyclicals over defensives, dividend growth over dividend yield, and companies generating unit growth and solid levels of free cash flow.

1 Source: BCA Research

The S&P 500 Index is a capitalization-weighted index of 500 stocks designed to measure the performance of the broad domestic economy. The Dow Jones Industrial Average is a price-weighted average of 30 significant stocks traded on the New York Stock Exchange and the Nasdaq. The Nasdaq Composite is a stock market index of the common stocks and similar securities listed on the NASDAQ stock market. The Russell 2000 Index measures the performance approximately 2,000 small cap companies in the Russell 3000 Index, which is made up of 3,000 of the biggest U.S. stocks. Euro Stoxx 50 is an index of 50 of the largest and most liquid stocks of companies in the eurozone. FTSE 100 Index is a capitalization-weighted index of the 100 most highly capitalized companies traded on the London Stock Exchange. Deutsche Borse AG German Stock Index (DAX Index) is a total return index of 30 selected German blue chip stocks traded on the Frankfurt Stock Exchange. Nikkei 225 Index is a price-weighted average of 225 top-rated Japanese companies listed in the First Section of the Tokyo Stock Exchange. Hong Kong Hang Seng Index is a free-float capitalization-weighted index of selection of companies from the Stock Exchange of Hong Kong. Shanghai Stock Exchange Composite is a capitalization-weighted index that tracks the daily price performance of all A-shares and B-shares listed on the Shanghai Stock Exchange. MSCI EAFE Index is a free float-adjusted market capitalization weighted index designed to measure developed market equity performance, excluding the U.S. and Canada. The MSCI Emerging Markets Index is a free float-adjusted market capitalization index that is designed to measure equity market performance of emerging markets. Barclays U.S. Aggregate Bond Index covers the U.S. investment grade fixed rate bond market. The BofA Merrill Lynch 3-Month U.S. Treasury Bill Index is an unmanaged market index of U.S. Treasury securities maturing in 90 days that assumes reinvestment of all income.

RISKS AND OTHER IMPORTANT CONSIDERATIONS

The views and opinions expressed are for informational and educational purposes only as of the date of writing and may change at any time based on market or other conditions and may not come to pass. This material is not intended to be relied upon as investment advice or recommendations, does not constitute a solicitation to buy or sell securities and should not be considered specific legal, investment or tax advice. The information provided does not take into account the specific objectives, financial situation, or particular needs of any specific person. All investments carry a certain degree of risk and there is no assurance that an investment will provide positive performance over any period of time. Equity investments are subject to market risk or the risk that stocks will decline in response to such factors as adverse company news or industry developments or a general economic decline. Debt or fixed income securities are subject to market risk, credit risk, interest rate risk, call risk, tax risk, political and economic risk, and income risk. As interest rates rise, bond prices fall. Non-investment-grade bonds involve heightened credit risk, liquidity risk, and potential for default. Foreign investing involves additional risks, including currency fluctuation, political and economic instability, lack of liquidity and differing legal and accounting standards. These risks are magnified in emerging markets. Past performance is no guarantee of future results.

CFA® and Chartered Financial Analyst® are registered trademarks owned by CFA Institute.

Nuveen Asset Management, LLC is a registered investment adviser and an affiliate of Nuveen Investments, Inc.

©2016 Nuveen Investments, Inc. All rights reserved