KEY TAKEAWAYS

- We believe the earnings recession may have ended in the third quarter.

- We expect potential upside to third quarter estimates due to supportive economic data, stable oil prices, and U.S. dollar stability.

- We will be watching closely to gauge the confidence of management teams in their ability to produce solid earnings gains in the fourth quarter and first half of 2017.

We believe the earnings recession may have ended in the third quarter of 2016. As the drags from sharp energy declines and a strong U.S. dollar continue to abate, backed by a pickup in economic growth, the S&P 500 could potentially produce a small increase in earnings on a year-over-year basis in the just-completed third quarter. This week we preview the third quarter earnings season and discuss the always important outlook for management guidance.

EARNINGS GROWTH RETURNS?

Third quarter earnings season gets underway this week with Alcoa’s results after the bell on Tuesday, October 11, followed by nine other S&P 500 companies over the rest of the week. Thomson-tracked consensus estimates are calling for a 0.7% year-over-year decline in S&P 500 earnings (FactSet and Bloomberg consensus figures are 0.5-1.5% lower). Based on the typical quarterly upside of about 3% that companies have historically delivered, a 2-3% earnings gain is a reasonable expectation, even including an expected 3.4% drag from the energy sector. The average upside above estimates over the past five quarters is actually a bit better at 4.5%.

Should the S&P 500 produce an earnings gain, based on Thomson Reuters data, it would prevent the streak of earnings declines from reaching five (or six based on FactSet and Bloomberg data) and end one of the longest earnings recessions — though far from the deepest — in the history of the index. Revenue growth is expected to return in the third quarter as well, breaking a streak of six straight quarterly year-over-year earnings declines (third quarter consensus is +2.6%). Both metrics may have put in a trough [Figure 1].

THE GOOD NEWS

We expect at least the typical upside to third quarter estimates and, outside of energy, solid earnings gains for several reasons:

· Supportive economic data. The Institute for Supply Management’s (ISM) Purchasing Managers’ Index, one of our favorite earnings indicators, rebounded more than expected in September 2016 to 51.5. Gross domestic product (GDP) in the third quarter is tracking to near 3% annualized growth, a strong pickup from the sub-2% growth pace in the first half of the year. The U.K.’s planned separation from the European Union (EU) has had a limited impact on the global economy, or even Europe, as of yet.

· Stable oil prices. Although the energy sector will likely see another significant earnings decline (though smaller than in the second quarter), oil prices held steady during the third quarter and gained some momentum with an 8% increase in September. That may help energy companies, including energy infrastructure companies in the industrials sector, meet or exceed expectations.

· U.S. dollar stability. The currency backdrop for U.S.-based companies operating overseas has generally been favorable over the past three months, although the British pound has weakened significantly versus the U.S. dollar. Still, the broad U.S. dollar index inched lower during the third quarter and fell 0.7% year over year, suggesting the currency may not be much of a profit drag during reporting season.

· Steady earnings expectations. The recent stability of analysts’ third quarter estimates suggests that the typical quarterly upside of 3–4% could potentially be achievable. Consensus analysts’ estimates for the quarter have fallen just 0.5% over the past month.

· Good start. The 25 companies that have reported Q3 earnings thus far have delivered solid results. Although this is a small number of companies, 80% have beaten earnings targets and 60% have met revenue forecasts, both about 10% above recent quarterly averages.

BROAD-BASED GAINS

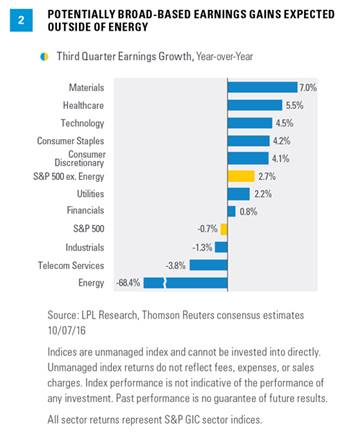

Potential earnings gains are expected to be broad based given the improving macro environment, with potentially nine of 10 sectors (excluding energy) in position to produce earnings growth if industrials and telecom are able to produce sufficient upside [Figure 2]. Among widely held sectors, healthcare could possibly deliver the strongest earnings growth during the quarter at 5.5%, followed by technology at 4.5%. We believe these sectors may be well positioned not only to produce solid growth, but also generate good upside given recent earnings performance. Recall technology was the standout performer in the second quarter while both sectors have seen above-average estimate revisions. The drug price controversy is unlikely to have a material impact on third quarter results for healthcare.

POTENTIAL RISKS TO THE DOWNSIDE

There are some risks to earnings meeting expectations, although we see them as manageable. First, U.S. presidential election uncertainty may have led to some cautious spending and slower capital investment during the quarter. Second, European bank concerns may have spilled over into U.S. financials. Third, although the process of leaving the EU has not begun, companies may have seen some impact from Brexit planning even if only through the financial markets. Fourth, although oil prices have stabilized, companies tied to energy capital investment continue to face a challenging environment. And finally, wage gains have picked up a bit and may limit profit margin improvements.

ALL ABOUT THE GUIDANCE

It’s always about guidance as stocks trade more on future expectations than past results. Remember that the next 12 months’ earnings estimates typically fall 2–3% during earnings season, which means that even a modest decline in estimates during earnings season can be viewed positively.

We expect generally favorable guidance for these reasons:

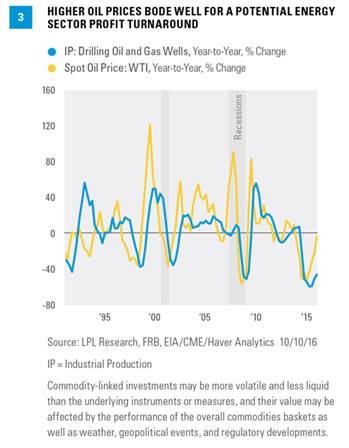

· Economic growth is starting to pick up. We expect the potential pickup in economic growth that occurred in the third quarter to continue through year end and into early 2017, based on our assessment of leading economic indicators. Global growth has been stable, although the U.K. is a risk as it exits the EU, and growth across Europe has been subpar. Bottom line, the macro outlook today is not materially worse than it was three months ago and might be a bit better. Oil prices are on the rise. At a price of $50 (about where West Texas Intermediate crude oil is now), oil prices would be up an average of 19% year over year during the fourth quarter of 2016 and much more in the first quarter of 2017. The relationship between oil prices and energy capital spending is strong [Figure 3].

· Favorable pre-announcement ratio. The ratio of companies pre-announcing negative results relative to those pre-announcing positive results, at 2.3, is better than the year-ago (3.1) ratio and the long-term average (2.7). Estimates held up relatively well during second quarter earnings season and may do so again.

· Future estimates have barely budged. Estimates for the fourth quarter of 2016 and for 2017 have held up well over the past one and three months, falling just 1.2% and 0.5%, respectively. We do not think the consensus estimates calling for a 14% year-over-year S&P 500 earnings gain in 2017 are realistic (something more like half that is more likely), but we do view the resilience of these estimates as a positive indication that guidance will be supportive.

These factors suggest that mid-single-digit earnings gains in the fourth quarter of 2016 may be achievable (consistent with consensus estimates), which could help support near-term stock market gains.*

CONCLUSION

The earnings recession may be coming to an end with third quarter results. There are reasons to suggest that earnings may potentially produce solid upside relative to expectations including mostly favorable economic data, oil price and currency stability, and steady estimates in recent weeks. But it’s always about guidance, so we will be watching closely to gauge the confidence of management teams in their ability to produce solid earnings gains in the fourth quarter of 2016 and first half of 2017.

*As noted in our Midyear Outlook 2016 publication, we believe the conditions are in place for a solid earnings rebound during the second half of 2016, due to the easing drags from the U.S. dollar and oil, coupled with minimal wage pressures. A slight increase in price-to-earnings ratios (PE) above 16.6 is possible as market participants gain greater clarity on the U.S. election and the U.K.’s relationship with Europe, and begin to price in earnings growth in 2017.

IMPORTANT DISCLOSURES

The opinions voiced in this material are for general information only and are not intended to provide specific advice or recommendations for any individual. To determine which investment(s) may be appropriate for you, consult your financial advisor prior to investing. All performance referenced is historical and is no guarantee of future results.

The economic forecasts set forth in the presentation may not develop as predicted and there can be no guarantee that strategies promoted will be successful.

Investing in stock includes numerous specific risks including: the fluctuation of dividend, loss of principal, and potential liquidity of the investment in a falling market.

Because of its narrow focus, specialty sector investing, such as healthcare, financials, or energy, will be subject to greater volatility than investing more broadly across many sectors and companies.

The fast price swings in commodities and currencies will result in significant volatility in an investor’s holdings.

All investing involves risk including loss of principal.

DEFINITIONS

Purchasing Managers Indexes are economic indicators derived from monthly surveys of private sector companies, and are intended to show the economic health of the manufacturing sector. A PMI of more than 50 indicates expansion in the manufacturing sector, a reading below 50 indicates contraction, and a reading of 50 indicates no change. The two principal producers of PMIs are Markit Group, which conducts PMIs for over 30 countries worldwide, and the Institute for Supply Management (ISM), which conducts PMIs for the US.

A Leading Indicator is an economic indicator that changes before the economy has changed. Examples of leading indicators include production workweek, building permits, unemployment insurance claims, money supply, inventory changes, and stock prices. The Fed watches many of these indicators as it decides what to do about interest rates.

INDEX DESCRIPTIONS

The Standard & Poor’s 500 Index is a capitalization-weighted index of 500 stocks designed to measure performance of the broad domestic economy through changes in the aggregate market value of 500 stocks representing all major industries.

The USD Index measures the performance of the U.S. dollar against a basket of foreign currencies: EUR, JPY, GBP, CAD, CHF and SEK. The U.S. Dollar Index goes up when the dollar gains “strength” compared to other currencies.

© LPL Financial