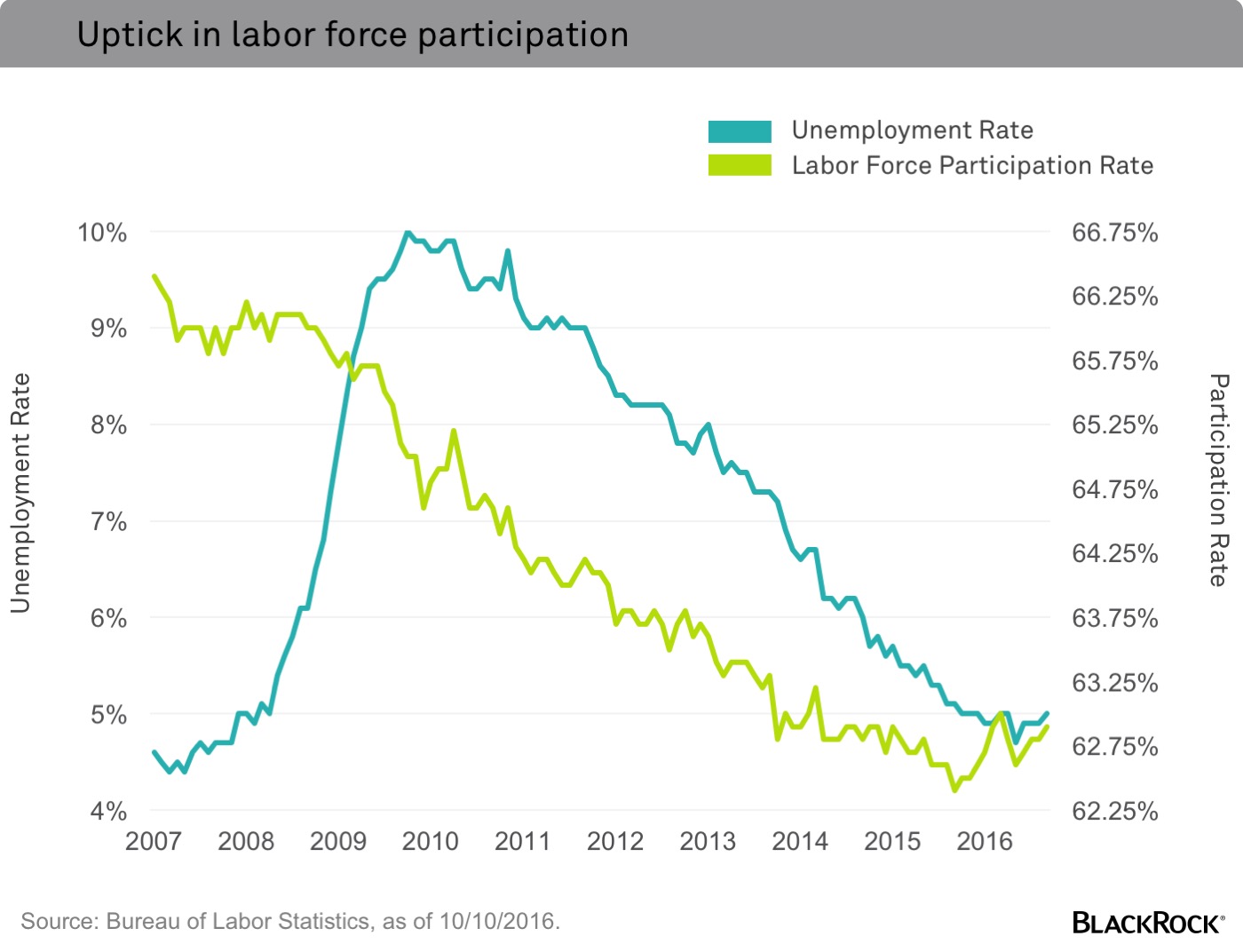

Many market watchers interpreted the September U.S. jobs report as a bit of a disappointment, as jobs growth came in slightly weaker than expected. But I think it was a decent report, fairly in line with where I expect the U.S. economy to be given that it’s moving on two tracks.

What do I mean by that? We’re currently witnessing a U.S. economy in which bothconsumption and employment in the services sectors have been amazingly robust, while expenditures and employment in good-producing segments remain softer. The September report showed this longstanding trend is continuing, with strong employment growth in service sectors, such as health care and education, and especially in professional business services (up a strong 67,000 last month). In contrast, the manufacturing sector lost another 13,000 jobs, continuing short-term and long-term trends. In fact, manufacturing employment peaked in June 1979, roughly four decades ago, with nearly 20 million jobs in the sector (or 1 in every 5 employees). At its trough in 2010, there were only 11.4 million manufacturing jobs in the U.S. (or less than 1 in 10 employees).

There are both demographic and technological underpinnings behind this two-track trend, as an aging population and innovations in technology boost employment in service industries that tend to be much more labor intensive.

The U.S. economy is also running along two separate tracks in another sense. We’ve seen strong employment growth in recent years, but merely decent levels of reported gross domestic product growth. Some say the incredible employment numbers reflect a poor-productivity economy. These arguments suggest that we have needed to hire many more people to produce a relatively smaller amount of goods, as if production and labor output were diminished in their ability to generate aggregate output. I believe this is a misguided interpretation of the economic landscape due to the fact that traditional productivity and output numbers don’t capture the downward influence of new technologies on prices.

The bottom line: The two-track trends evident in the September jobs report are just more signs that the U.S. economy is doing better than headline numbers may imply. So where does this leave us from a monetary policy perspective? The Federal Reserve can, and will likely, move policy rates at its December meeting, barring an unexpected shock to the economy or markets.

Rick Rieder, Managing Director, is BlackRock’s Chief Investment Officer of Global Fixed Income and is a regular contributor to The Blog.

This material is not intended to be relied upon as a forecast, research or investment advice, and is not a recommendation, offer or solicitation to buy or sell any securities or to adopt any investment strategy. The opinions expressed are as of October 2016 and may change as subsequent conditions vary. The information and opinions contained in this post are derived from proprietary and nonproprietary sources deemed by BlackRock to be reliable, are not necessarily all-inclusive and are not guaranteed as to accuracy. As such, no warranty of accuracy or reliability is given and no responsibility arising in any other way for errors and omissions (including responsibility to any person by reason of negligence) is accepted by BlackRock, its officers, employees or agents. This post may contain “forward-looking” information that is not purely historical in nature. Such information may include, among other things, projections and forecasts. There is no guarantee that any forecasts made will come to pass. Reliance upon information in this post is at the sole discretion of the reader.